QE or Not QE, That is the Question

The Fed, in consort with the FDIC and US Treasury, has created two new rescue programs that are rapidly inflating its balance sheet -- the Bank Term Funding Program and a revised FDIC policy that covers all deposits at certain banks for any amount of money -- sky is the limit -- but only if the bank is what one senator called "one of your preferred banks," by which he meant the too-big-to-fail banks like JPM and BofA -- the same ones that always get the vast bulk of bailout money so they don't fall on us.

An even larger factor driving up the Fed's balance sheet right now is the sudden return to its normally shunned (due to stigma) discount window where banks can get short-term (typically emergency) funding at the Fed funds rate, which is 4.75% right now, but likely to change by the time this article is published.

The question flying around everywhere as people watch in shock and awe the abrupt skyward climb of the Fed's balance sheet is whether this is a covert reversal of the Fed's quantitative tightening (QT) program back to full-on quantitative easing (QE). Did the Fed just pivot without saying so -- if not on interest rates, then on QT back to QE?

That turns out to be a complicated question with a nuanced answer necessary. So, I'll provide the answer by turning to several parties with varying views and try to sort through them to lay out a view makes the most sense to me ... and maybe to you ... as I think may way through this. I'm sure Jerome Powell will be giving his own view by the time I hit the "publish" button on this, and it should be interesting to hear how he wrestles with this.

First, let's cover the basics.

What is the new Bank Term Funding Program?

Here is a good summary of how the new program works:

Among measures to counter fallout from the failure of Silicon Valley Bank, the Federal Reserve said it would create a new lending program for banks: the Bank Term Funding Program, or BTFP.

The facility will allow banks to take advances from the Fed for up to a year by pledging Treasurys, mortgage-backed bonds and other debt as collateral. By allowing banks to pledge their bonds, they can meet customer withdrawals without having to sell their bonds at a loss, which is what Silicon Valley Bank did last week, sparking a run on the bank.…the Fed won’t look to the market value of the collateral, which in many cases reflect big unrealized losses due to the jump in interest rates.WSJ via Bonner Private Research

Banks have to pay for this benefit, so it is not like the free money the Fed gave them under original QE, but let's read on. Here's another description of the plan to make sure we have a full view:

Bank Term Funding Program

The new Fed facility, the Bank Term Funding Program (BTFP), is to lend for periods of up to one year on a collateralized basis. The collateral is anything that is eligible for the Fed to purchase under open market operations. This is primarily US Treasury securities, agency debt and mortgage-backed securities.

An important element of BTFP is that collateral will be valued at par. The significance of this is that much of the current collateral held at banks has a market value of less than par, as it was purchased during the recent period when interest rates were much lower than they are now. By using par value, the Fed is allowing the banks more leniency in their borrowing. The Fed is deviating from their historical practice by not requiring at least 100% collateral backing their loans.

The market decline in their bond holdings is what got SVB in trouble in the first place. Because they owned long duration Treasuries and MBS which had declined in market value as interest rates rose, when depositors withdrew their funds, SVB needed to raise cash to meet the withdrawals and their only quick option was to sell their bonds at a loss, which wiped out their capital.

By allowing borrowing under BTFP with collateral valued at par, the banks will not be forced to sell their underwater securities and recognize losses to meet their liquidity needs.

As a refresher, the banks do not have to write down the value of their securities held in reserves until they sell them. So, the wipeout came when bank runs forced selling, depleting the capital of some banks by around 20%. The key word in the above description is that the banks are borrowing the cash with the bonds turned over as collateral on a loan with interest, not selling them; so, the banks avoid the requirement of writing down the value of their capital in present circumstances where the Fed has created the loss of value.

Is this a silent "pivot," and will it fuel a new bull market or inflation as the old QE did?

First, to be clear, I have always said the Fed will NOT pivot until something breaks; and then the breakage will be so serious that it won't matter to stocks that a pivot has happened anyway. We've certainly cleared that bar. Clearly something huge broke, or we would not even be talking about TWO massive new bank rescue plans -- BTFP and the huge expansion of FIDC insurance to cover all deposits of any size at select banks -- or the massive rush to the Fed's discount window, after years of quiet at that "window," to borrow huge sums of cash that comes at a cost.

So, yes, the Fed continued until something broke; and, yes, the breakage was serious enough that the new plan, being called "stealth QE" by some, is not turning the stock market back to a bull market ... so far. That means, whether we consider the new BTFP a pivot or not, has no bearing on what I said for months about the Fed not pivoting until it was too late because something big broke. We've cleared that bar.

Some might say, "Ah but this is going to turn the market into a new bull market, even if it hasn't quite done that yet." To address such a hypothetical claim that might arise, I'm going to turn to last year's biggest bear in the mainstream financial media, Morgan Stanley's Michael Wilson 1) because he lays out clearly why it will not create a new bull market like QE did, and 2) because this way you get to hear it from a different source than just me, and 3) because Wilson called the bear market very accurately throughout last year; but 4) he is equally facile and willing to call bull markets whenever they are coming.

His focus is more on the bailouts of large depositors, not on the BTFP bond-trading program, but those depositor bailouts are all paid out of the increase that has just happened in the Fed's balance sheet that many are identifying as a form of stealth QE because it sure looks like it is. So, what he has to say about the balance sheet, QE, and bull markets still applies to the BTFP contribution, too, which is actually the smallest contributing factor at present. Wilson starts by asking,

Why On Earth Did US Stocks Rally Last Week?

The uninsured deposit backstop put in place last weekend by the Fed/FDIC will help to alleviate further major bank runs, but it won’t stop the already tight lending standards across the banking industry from getting even tighter. It also won’t prevent the cost of deposits from rising, thereby pressuring net interest margins. In short, the risk of a credit crunch has increased materially....

If growth is likely to slow from the effective tightening rolling through the US banking system, as we expect, and the bond market seems to be supporting that conclusion, why on earth did US stocks rally last week? We think it had to do with the view we have heard from some clients that the Fed/FDIC bailout of depositors is a form of quantitative easing (QE) and provides the catalyst for stocks to go higher.

While the massive increase in Fed balance sheet reserves last week does reliquefy the banking system, it does little in terms of creating new money that can flow into the economy or the markets, at least beyond a brief period of, say, a few days or weeks. Secondarily, the fact that the Fed is lending, not buying, also matters. If a bank borrows from the Fed, it is expanding its own balance sheet, making leverage ratios more binding. When the Fed buys the security, the seller of that security has balance sheet space made available for renewed expansion. That is not the case in this situation.

One qualitative difference in terms of whether this balance-sheet expansion can inflate market assets as QE did, creating a wealth effect that might pump money into the economy, as QE did, is that this is happening by lending, making this more like a repo loan, except with a one-year term, as opposed to overnight. That, at least, means it is not permanent new money as with QE. With QE, the banks also made a profit off of securities they sold to the Fed, inclining them to do it just for the profits, which did add money into the economy. In this case they have to pay the Fed about 4.75% interest, depending on the facility used, disinclining them to do it unless they need to.

Wilson also explains that loaning a security to the Fed in order to get a loan of cash back from the Fed does not make room for the banks to offer additional loans on their reserves -- to expand the economy. That is because the Treasury they are turning over to the Fed was already on their reserve balance sheet. They are merely converting it to more liquid cash. So, it is net neutral on their balance sheet. It is just more liquid.

Moreover, while all the balance-sheet expansion on the Fed's balance sheet was related to the various forms of assistance provided in the present banking crisis, almost none of it was actually from the BTFP SO FAR:

According to the Fed’s weekly release of its balance sheet on Wednesday [the 15th that we are talking about], the Fed was lending depository institutions $308B, up $303B week over week. Of this, $153B was primary credit through the discount window, which is often viewed as temporary borrowing and unlikely to translate into new credit creation for the economy. [Note: that amount is up from $4.58 billion the previous week, so it's a huge leap, even higher than the previous all-time high leap of $111-billion back in 2008.] $143B was a loan to the bridge banks the FDIC created for Silicon Valley Bank and Signature. These reserves are obviously going nowhere. Only $12B was lending through its new Bank Term Funding Program (BTFP), which is viewed as more permanent but also unlikely to end up converting into new loans in the near term.

So, most of this was related, as I just said in introducing Wilson's comments to the FDIC insurance provided for accounts over $250,000, not due to the BTFP program. Most does not create new money because the Fed is not financing new bond issuances, even indirectly, and is taking as much money in face value off of bank balances at the Federal Reserve by withdrawing their bonds so no loans can be made on them as it is adding in cash that banks can loan on. So, it is roughly net neutral.

I suppose either could be thought of as a return to QE if it is hugely expanding the Fed's balance sheet, but it is, as Wilson points out, highly unlikely to cause serious inflation because in all of these situations, the money is essentially either just changing form with money already in the banks to a more liquid form (while the Fed holds the Treasury taken as collateral out of the monetary system) or is replacing deposits that already existed but were about to get wiped out; so, still not really a net gain in money supply over what was already there, and because banks are not in a mood to use this money to issue loans right now. They are in a mood of making sure they save themselves from bank runs with plenty of cash on hand.

In short, none of these reserves will likely transmit to the economy as bank deposits normally do. Instead, we believe the overall velocity of money in the banking system is likely to fall sharply and more than offset any increase in reserves, especially given the temporary/emergency nature of these funds. Moody’s recent downgrade of the entire sector will likely contribute further to this deceleration.

This is a detailed way of explaining why it is that the sudden "stealth pivot," as some are calling it, will not do any good for stocks, as I said would be the case when and if a pivot ever happened because things broke. The balance-sheet expansion is merely compensating for money that already existed but was about to get wiped out to prevent an actual further reduction in monetary supply than what is happening concurrently with the continued Fed's roll-offs under QT (and, yes, they are continuing), or it is turning bonds that were already in reserves to pure liquid fiat, digital currency without really changing the amounts they have in reserves. The banks will then be paying that cash out to all the parties who are creating a run on the banks' reserves; but that money is no more likely to be spent in the economy than it was when it was sitting in the accounts before all this broke out. It is just changing banks, which means it will go from one bank's reserve account with the Fed to another bank's reserve account.

It is more financial churn than it is a change in the velocity of money. If anything all this noise and concern is likely to make everyone less likely to go out and actually spend the money on Main Street (maybe a lot less), which can ratchet up the price of goods and services. Another thing I've been saying throughout the years of writing this blog is that money only creates inflation where money circulates. If all it is doing is moving from one bank's vault to another (or one bank's computer data at the Fed to another's), then it creates no inflation at all.

So, is it really even a pivot?

With all of that said, one writer in this field, whom I respect, Bill Bonner, has just asked that question in an article titled, "The 'Stealth Pivot': Is this the moment we've been waiting for?" First, he leads off by implying this is a stealth pivot back to QE (not to lowering interest, which was the main aspect of the "pivot" the bulls have been fantasizing about for nearly a year and which certainly hasn't happened:

The most important thing that happened was that the Fed revealed more of its ‘stealth pivot.’ It came out with a program to bail out the big depositors of failing banks....

The new alphabet group – BFTB, or something like that – is going to look after large account holders. In other words, the whole banking system is being nationalized.

Well, not exactly. The losses are being nationalized. The profits will remain with the bankers.

As I've said for years, the same rinse-and-repeat "solutions" get preferred every time. In 2008, George Bush nationalized (or "socialized," as I put it) the losses of banksters, but never the profits. Those stayed with the top 1%. These cowardly, quasi-capitalists only socialize things the moment their greed winds up costing them ... to make sure it costs someone else, instead.

Ultimately, when you spend more than you can afford, something’s gotta give. Either you go broke....

Most of us remember Speaker of the House John Boehner saying back in those days, "We're broke."

Or, if you are a sovereign country with debts denominated in your own currency, you ‘print’ more money to pay the bills. It’s either deflation (when prices fall), or inflation (when the dollar falls). Either you protect the currency (and the people who depend on it) and let the chips fall where they may. Or you print and spend…and let the dollar go to Hell.

Bonner is of the opinion that this program is QE, and that means the dollar's value will crash in a hyper-inflationary slide. We know by experience that is not a foregone conclusion or inevitable cause and effect. We saw years on end of QE in which the Fed couldn't even get inflation up to its target. So this "ain't necessarily so."

It is, however, the motivating narrative that those with gold to sell love to endlessly deploy or the feel-good narrative that those gold to hoard love to believe to validate their holdings. We've had years of the most massive monetary expansion on earth that created virtually no inflation. (It all depends on 1) where the money circulates and 2) scarcity (shortages) to provide a reason for people to use the additional money to bid up prices ... as no one bids up prices just because they have money when competition is willing to provide a better price elsewhere. There has to be an imbalance between supply and demand.

Last week, we saw the gates of Hell open a little wider.

Big depositors, faced with big losses, turned to the big Fed for relief.

They always do in order to socialize their losses when their nefarious work caves in on them.

The Fed could have said: ‘you called the tune; you dance to it.’

We saw during the Great Recession that it usually only does that with banks it doesn't care for.

But the feds live in a fake world…a planet of wishful thinking and self-serving illusions. For more than 12 years, they encouraged people not to save, but to spend.

Always part of the cycle, too -- solve each bubble implosion by blowing up a bigger bubble financed with a bigger mountain of debt -- or, as Bonner phrases it on the Fed's behalf:

You’ve got too much debt. We’ll give you more of it … so we can keep the scam going.’ That is how the Fed handled every crisis since 1987.

Rinse and repeat.

It backed the markets with more and more credit…leading to more and more debt…to the point where the debts cannot be serviced at normal interest rates.

For sure it did. So, we agree that the Fed fueled the present inflation and is now pulling the rug out from under its own "economic recovery." The economy, of course, did not so much recover as float along (literally I banking terms) on a magic carpet of Fed mystery money. But this time, as I stated repeatedly over the past two years, is different:

Now, for the first time in 40 years, the Fed is not merely adding debt, goosing up the economy and making the rich richer, it is fighting inflation....

No more magic carpet. That puts the Fed (and us with it) in an impossible trap where the Fed will ultimately be forced to choose between high inflation -- likely higher than we already had -- or even hyperinflation or a massive economic collapse. Choosing the former path, which is likely to come from more of its traditional money printing, if it goes back to that, could create hyperinflation and only blows up the bubble once again for another rinse and repeat. Except this time I do not believe the tired old balloon of a bubble will inflate so nicely.

If you've read Bonner, you know he predicts the Fed will go back to QE and pick the hyperinflation path. Bonner says the stealth pivot already began a month ago. That would be the first I've ever heard of that timing, and I see no evidence of what he claims:

A month ago, [the Fed] quietly changed the way it handles its QE bond portfolio. Instead of letting the bonds run off – as had been the program (to reduce the money supply) – the Fed began quietly rolling them over … effectively increasing the supply of debt in the Fed’s balance sheet.

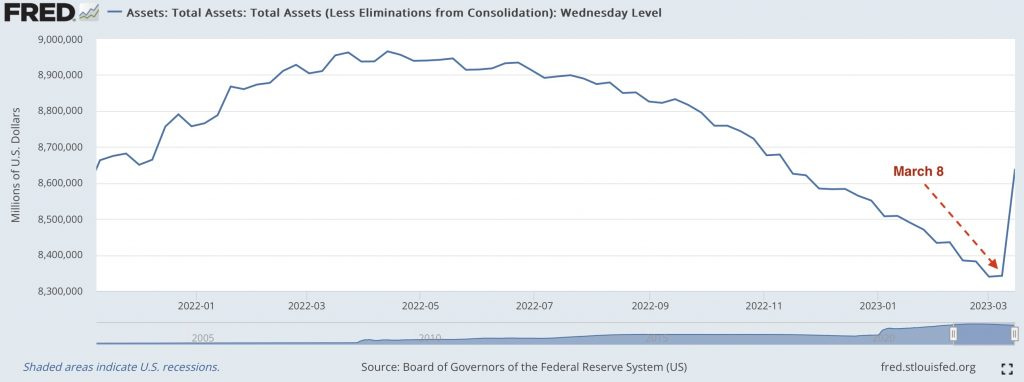

This has been burning up the Twitter wires all night. Quantitative Tightening reduced the Fed's balance sheet by $625 billion when it started on April 13th of last year. Since March 1st, it's up $299 billion. So 47% of QT was wiped out when the first hint of crisis came.

I don't think so. If you look at the following Fed graph, you will see it looks like the first ever-so-tiny tick up happened on March 8th, not on the 1st, and certainly not "a month ago":

I see a consistent glide path down until after March 8. Even the slight uptick on the 8th is consistent with every previous uptick, all of which were followed by a larger down-draw -- consistent in timing and scale. The first clear move up came in a single MASSIVE leap on March 15th (as the Fed posts the moves once a week). That was right after the Fed created BTFP on March 13th. So, it is pretty clear the huge increase was created by the funds that were suddenly demanded by banks trading in their bonds as collateral on loans right after they learned of the new program on the 13th.

That solitary move appears to have erased almost half of the QT the Fed had done, except for all the reasons above regarding how differently this increase of the balance sheet works by being so unlikely to create new money that would add to circulation in the general economy. This was not due to a quiet change in how they roll over bonds. A change to just ending QE and going back to rolling over (refinancing) the bonds they had been rolling off, would simply be an upward move relatively similar in scale to the downward moves that came from not refinancing them.. or would simply be flat.

No, this is full-on balance-sheet expansion in scale ... so it looks like QE, but I am inclined to agree with Wilson on this as to whether or not this will inflate asset markets or consumer prices or even add any money at all to the Main Street economy. If it does not even inflate asset markets (which we saw a lot of under QE), it seems even less likely to create extreme consumer inflation because it does not meet the criteria for increasing the velocity of money or the criteria that money only creates inflation where money actually circulates. It doesn't appear to Wilson it's even goin to create inflation in Wall-Street assets. It appears to be activity that is likely to only happen between banks and the Fed to guarantee deposits.

Is it QE in kind and substance?

Wolf Ricther has some informative thoughts to share on this.

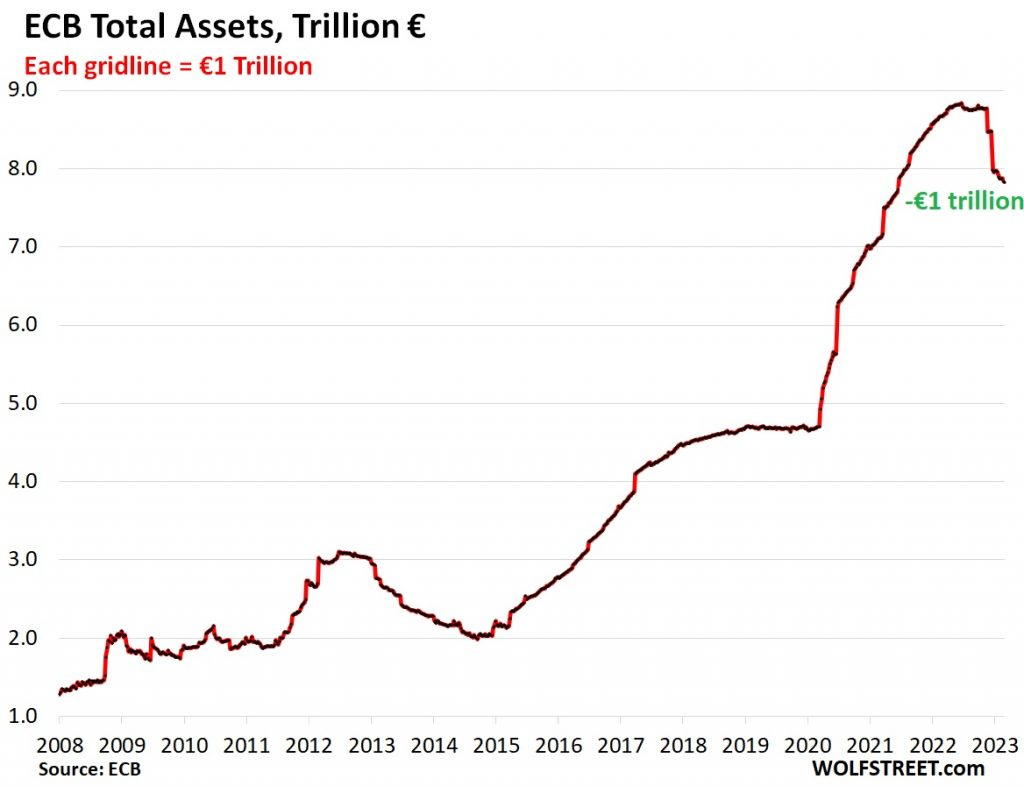

First he noted that the European Central Bank, in a similar situation, is "defying pivot mongers." In other words he does not consider anything that is happening in Europe's central bank to be actual QE, and he notes that QT is continuing apace there. In terms of "denying pivot mongers," he was referring to interest rates, and saying the ECB had not pivoted at all on interest but had gone full speed ahead, which he expects the Fed will also do today:

The ECB hiked its policy rates by 50 basis points today, defying predictions and fervent hopes out there that it would end its rate hikes. Yesterday, traders saw just a 20% chance of a 50-basis-point hike. They’d all been hoping that the ECB’s rate hikes would be shut down by the banking turmoil.

That didn't happen last Thursday with the ECB, and it probably will not happen today with the Fed either, unless more breakage piles up on the Fed between now and the end of its meeting at a time when that could easily happen. So, no pivot on interest rates so far at the ECB -- even after significant things broke -- and the same is likely to be true at the Fed, and a pivot on interest rates was the big thing the stock market kept gambling on as a fantasy since last summer that has never manifested.

With this 50-basis-point hike, the ECB stuck to the rate-hike indications it gave at its last meeting.

“Inflation is projected to remain too high for too long,†is how the ECB started out its press release today to point out where its emphasis was.

The ECB is staying fully engaged in the inflation fight, just as I have said the Fed will, stock market be damned as far as they are concerned. They are not ultimately in the stock-market business; they are in the money business, and guarding their money against inflation comes first and is a legal mandate. That has been a mantra with me in face of the seemingly unkillable ghost pivot fantasy.

There are, of course, many testosterone-flooded bulls who won't give up the ghost on this fantasy. That is ultimately going to be their great loss as they keep riding waterfalls down for refusing to believe in truth while denying economic reality all around them. Their problem, not mine and not (to their surprise) the Fed's.

“We are not waning on our commitment to fight inflation, and we are determined to return inflation back to 2% in the medium term – that should not be doubted. The determination is intact. The pace that we take will be entirely data-dependent,†ECB president Christine Lagarde said at the press conference.

It doesn't get stated any clearer than that. In fact, the ECB is taking the bulls by the horns:

“There is no trade-off between price stability and financial stability. And I think that if anything, with this decision [hiking by 50 basis points when markets were expecting no hike], we are demonstrating this,†she said.

As you may recall, I said in my recent post that the Fed would do well to stay with its projected 25-basis-point path, so as not to stir markets by doing less and convincing markets it must be panic or by causing more fear by raising rates 50 basis points. So, the ECB chose exactly that path, since they had already forecast 50 basis points, even though they went ahead of the market's expectations. If the Fed does the same, there will not only have been no pivot, but no pause.

We have also seen that these emergency actions, even much greater sounding ones, have already proven to be short-lived and monetarily neutral over the course of a couple of months:

The BOE stepped in with big rhetoric about massive buying of gilts, but in fact bought only small amounts. It calmed down the gilts market and gave pension funds time to clean up. In November, it started selling those bonds it had bought in September and October. And by January, it had sold all of them. With the panic settled down, the BOE’s rate hikes and QT continued.

Of course, we are getting into much more troubled waters where banks are actually going bust, and that hits right in the Fed's domain where the banks that own the Fed expect it to save them.

As we've seen in the United States,

Energy prices in the euro area have been declining, but inflation has shifted to services, with the Eurozone CPI without energy spiking 7.7%, core CPI without food and energy spiking 5.6%, and services CPI spiking 4.8%, all of them records.

That is similar to what is happening here, and we know central banks (CBs) have been closely coordinating their action at this juncture, so we can likely expect the Fed to respond in a similar way to similar inflation dynamics.

The ECB's balance sheet at that time looked like this:

{kind=link}

Its rate of decline is slowing, but the balance sheet is still going down. So, no pivot on interest or QT at the ECB. LIkely no pivot or pause on interest at the Fed, and the balance sheet expansion does not really function like QE, so may have no stimulus effect even in assets, much less on Main Street. That remains to be seen, but I think Wilson made a fair case.

While Wilson explained the difference in terms of how the money flows and its effect, Wolf explains in another article about the Fed's balance sheet that difference in more granular detail:

On today’s balance sheet, there are two new accounts, the Bank Term Funding Program (BTFP) and “Other credit extensions†that were announced last Sunday as part of the liquidity support for banks and the depositor bailout with the FDIC.

Wolf also notes that the 4.75% interest ...

is expensive money for banks, and it requires collateral, and so banks won’t borrow long at this rate if they can avoid it, and they tend to pay back those loans quickly....

They borrowed this way because they needed to have the funds like “right now†when depositors were yanking their money out late last week and this week, as SVB Financial collapsed and panic spread.

Because these are emergency funds that banks want to pay back quickly, they are not likely to have much impact on monetary policy and, hence, on inflation ... unless, of course, the banks cannot pay them back; but then we have a broader set of troubles that could as easily be disinflationary as inflationary, depending on whether it finally does get the Fed to reverse into full-on QE.

If this goes like the Repocalypse, all of this could keep increasing in amount and become full-on QE effectively, but I don't think it is as apparent (so far) that it will do that as it was in the Repocalypse, and that money was a lot cheaper than this money. (The BTFP side of this dual program has slightly lower interest than the money used to directly bail out depositors in the recent crash or drawn by banks from the Fed's discount window, but not by much. It's running about 4.6%; yet, it is the least used so far.)

Of course, we are only one week into this rescue money with only a single snapshot from last week's (mid-month) change in the Fed's balance sheet, and it is broadening from day to day; therefore, much can change by the time the next balance sheet update gets posted after the month is over. Much can change in the entire banking picture for that matter.

For now, however, there has been NO PIVOT, even after serious damage that shook up the entire banking world was accomplished. Hence, we have yet, to see the QT picture as Wolf explains:

QT-related roll-off continued. Treasuries roll off twice a month, when they mature mid-month and at the end of the month. Today’s balance sheet captured the mid-month roll-off of $7.1 billion in three-year notes, which was the only security on the Fed’s balance sheet that matured. A big roll-off is coming at the end of the month.

Of course, not everyone agrees:

“The new BTFP facility is QE by another name,†strategists at Citi write. “Assets will grow on the Fed balance sheet, which will increase reserves. Although, technically, they are not buying securities, reserves will grow.â€

Apparently everyone is having a little difficulting agreeing on how to consider the effects of this expansion of the balance sheet if one allows for the difference between buying Treasuries and other securities from banks outright for cash or borrowing them as collateral for cash the bank borrows from the Fed.

Even if bank balance sheets grow, I think this money is destined to circulate almost entirely in banking circles and not out on the street -- either Main Street or Wall Street -- because in perilous times like this, banks are using cash to save themselves from all-out death due to bank runs. They are not inclined to be making big splurgy investments in a falling stock market (or, at least, a very edgy market) with money they are borrowing at 4.6%-4.75% (and likely rising at today's Fed meeting).

Bank clients are also not going to get all spendy. In crisis moments like the present, they are glad to simply safeguard their cash and make payroll.

No pivot coming either

David Stockman also says the Fed will not pivot on its inflation battle:

Why would you throw-in the towel now? We are referring to the Fed’s belated battle against inflation, which evidences few signs of having been successful.

Yet that’s what the entitled herd on Wall Street is loudly demanding. As usual, they want the stock indexes to start going back up after an extended drought and are using the purported “financial crisis†among smaller banks as the pretext.

We can expect no less from the bullheaded bulls who never give up on their greed. So, long as the 1% gets back to making the big money in stocks, inflation is just a cost of doing business for those guys. They want the pain of crashing stocks to end. They are not enjoying the waterfalls this economy keeps giving to stocks as the Fed keeps sucking money out of the economy to try to curb the inflation the Fed's money fueled when it hit the heat of product and service shortages, made worse by Covid regional and national lockdowns, Covid factory shutdowns, Covid deaths and long-Covid (or vaccine) disablements and then war and sanctions. All that money lit prices on fire in the environment of all those shortages.

Those are forces the Fed can do nothing about. So, as Stockman says (and so does the Fed) the fight is far from over as the Fed tries to take down inflation by just withdrawing money, which means the market bulls are still delusional. More delusions equal more times of getting their heads slammed from ceiling to floor. Oh well. Their pain, not mine.

So, let's keep the blame for inflation and the perils of fighting it where it rightly lies:

Well, no, there isn’t any preventable crisis in the small banking sector. As we have demonstrated with respect to SVB and Signature Bank, and these are only the tip of the iceberg, the reckless cowboys who were running these institutions put their uninsured depositors at risk, and both should now be getting their just deserts.

To wit, executive stock options in the sector have plunged or become worthless, and that’s exactly the way capitalism is supposed to work. Likewise, on an honest free market their negligent large depositors should be losing their shirts, too.

I certainly wish this country would let actually capitalism exist. If it did, we wouldn't have built up so much dry tinder in the banking forest now to burn:

After all, who ever told the latter that they were guaranteed 100 cents on the dollar by Uncle Sam? So it was their job, not the responsibility of the state, to look out for the safety of their money.

If the American people actually wanted the big boys bailed out, the Congress has had decades since at least the savings and loan crisis back in the 1980s to legislate a safety net for all depositors. But it didn’t for the good reason that 100% deposit guarantees would be a sure-fire recipe for reckless speculation by bankers on the asset-side of their balance sheets; and also because there was no consensus to put taxpayers in harms’ way in behalf of the working cash of Fortune 500 companies, smaller businesses, hedge funds, affluent depositors and an assortment of Silicon Valley VCs, founders, start-ups and billionaires, among countless others of the undeserving.

Let me just note that disguising the cost of the infinitely raised deposit insurance as "insurance fees" the banks will pay, is a bit like the mafia telling a store owner he will have to pay insurance fees for protection ... from the mafia. Because that is what the banks will be buying and passing along in some way to depositors -- insurance (protection money) paid to the FDIC to protect them from the Fed and from incompetent FDIC regulators ... and apparently from their own greed and mismanagement.

In any event, inflation is still raging and wage workers are still taking it on the chin. During February real wages dropped for the 23rd consecutive month. So the Fed needs to stay on its anti-inflation playbook, come hell or high water. That means it needs to keep raising rates until their after-inflation level is meaningfully positive, which is not yet remotely the case....

Real interest rates are still deeply underwater.... The cries to stop the rate increases, therefore, are just damn nonsense.

In fact, in any sane world these are not even “increasesâ€. They are long overdue normalization of interest rates that have been absurdly pinned to the zero bound for upwards of a decade.

The Fed is not going to find it politically easy (or legal) to step in and pump up inflation again on everyone to save the one-percenters in the stock market. It certainly is not going to find it politically easy to jack inflation tax on the masses back up with rescue plans due to rich and greedy banksters who, once again, devastated the economy, particularly the banksters at the Fed who were actively setting up this catastrophe for years with their profligate monetary policy and deplorable bank monitoring.

The Fed remains trapped in killing banks

The punishment will end when the pain stops.

As Lance Roberts writes,

Since the turn of the century, the Fed has been able to repeatedly support financial markets by dropping interest rates and providing monetary accommodation. This was because inflation remained at low levels as deflationary pressures presided.

The Fed, as I've stated many times, contrary to the delusions of market bulls, cannot drop interest rates this time, and it cannot go to the kind of balance-sheet expansion that stimulates markets and drives up inflation either. So, if the present kind of expansion does turn out to drive inflation, the Fed is in a tough bind.

With inflation running at the highest levels since the 80s, the Fed risks creating another inflationary and interest rate spike if they focus on financial stability. However, if they focus on inflation and continue hiking rates, the risk of a further crack in financial stability increases.

I don’t know which path the Fed will choose, but the markets have little upside. The moral hazard the Fed created in the first place has now come home to roost.

I'll finish with something I quoted in my last article,

Never attribute to malice that which is adequately explained by stupidity, unless it keeps happening over and over.