Credit Crisis Cruising Toward Collapse

While this is not an article about the US national debt, one cannot comprehend the overall scale of US debt crisis without also including the world's largest elephant in the room. Here stands the largest debt the world has ever known, growing faster than any debt has ever grown. It dwarfs the entire combined value of all Fortune-500 companies.

Under Obama, the national debt increased by more than the value of all the gold ever mined in the history of the world (at today's gold price). Under Trump, it is expanding even faster to where, by the end of his term, it will have increased again by as much in inflation-adjusted dollars as the entire debt accumulated at the end of World War II -- a period during which the US government often spent 50% of the nation's entire GDP. That debt expansion, however, was to win a global war in order to stop an epic villain who wanted to rule the world. It happened during one of the world's darkest times. This time, however, it's just to cover routine operating expenses and establish futile regime changes around the world. It is happening during supposedly the greatest of economic times. And no one in government or the Fed or in finance or economics sees a problem with this?

To get a sense of how out-of-control this debt has become, consider the following: In four years, the interest on the national debt is expected to exceed the entire national defense budget, which exceeds the defense budgets of China, Russia, Saudi Arabia, India, France, the United Kingdom, Japan and Germany combined. With just the interest on this debt, the US could operate all of Canada -- its entire national budget -- plus most of its provincial budgets, and that is at today's abnormally low interest rates, which are now rising. You cannot even solve this problem by taxing away 100% of the accumulated lifetime wealth of all the billionaires in the nation. The entirety of their wealth would only run the government for four months!

This article, however, is about other debt disasters in the US economy that appear to be climaxing, but I want you to keep the scale of the national debt in mind as the matrix in which all these other debt crises you are about to contemplate are forming.

The Federal Reserve is accelerating all debt problems

The other background to keep in mind as you consider the debt monsters described below is that the Federal Reserve is changing the matrix. It is now intentionally exacerbating all of these problems by increasing interest rates. The Federal Reserve's balance-sheet unwind, or the Great Recovery Rewind, as I call it, will result in billions of dollars of existing loans becoming mispriced as the entire market shifts around them. Investors will begin to dump loans they hold at fire-sale prices, resulting in enormous losses. The multitude who need to refi will be doing so in a tougher environment.

This is a loan market riddled with a decline in quality in terms of earnings to support loan payments, loan packaging that hides loan problems, reduced covenants that formerly protected investors because investors have been willing to take on more risk in the chase for yield, and other declining underwriting standards ... just like we saw in the run-up to the financial crisis that gave us the Great Recession.

Standards for credit relaxed around the chase for yield during the past period of artificially lowered interest. As the Fed stops suppressing true price discovery in the marketplace, the standards for loan qualification will toughen up again because the chase for yield becomes less desperate. In that situation, investment grade material declines into junk; junk falls into default. Zombie corporations that were kept alive beyond their time during cheap credit go bankrupt.

Loan lizards lining up for slaughter

The lowest belly-dragging loans in the market are those called "leveraged loans." The US has amassed $1.1 trillion in leveraged loans held by institutions. If you wonder whether that amounts to much in a world where trillions now seem routine, this heap of reptilian loans is almost double the size that existed at the start of the last financial crisis only ten years ago.

This growing segment of the financial world involves loans, usually arranged by a syndicate of banks, to companies that are heavily indebted or have weak credit ratings. These loans are called 'leveraged' because the ratio of the borrower’s debt to assets or earnings significantly exceeds industry norms....

November, 2018: The International Monetary Fund issued a warning that leveraged loans were approaching a globally threatening level because the market has grown to such a massive size. Clearly the US has followed this same path, given the doubling of its own rubbish heap. Three economists at the IMF highlighted alarming trends, including speculative excesses. This is where the Fed's changes to the financial environment are likely to create wholesale damage:

With interest rates extremely low for years and with ample money flowing though the financial system, yield-hungry investors are tolerating ever-higher levels of risk and betting on financial instruments that, in less speculative times, they might sensibly shun.... Globally, new issuance of leveraged loans hit a record $788 billion in 2017, surpassing the pre-crisis high of $762 billion in 2007.... It is not only the sheer volume of debt that is causing concern. Underwriting standards and credit quality have deteriorated.

Highly leveraged loans were issued with fewer and fewer covenants that protect investors. Earnings that support the loans are becoming more creatively expressed as companies move increasingly toward non-GAAP accounting, allowing borrowers to pile on more debt. And loans are being packaged with other loans to hide their problems. (Ring any pre-crisis bells?)

The IMF's sobering conclusion:

Having learned a painful lesson a decade ago about unforeseen threats to the financial system, policymakers should not overlook another potential threat.

Did we? Did we learn nothing?

December, 2018: Loan funds suffered dramatic redemptions in December when the stock market was falling. Prices on existing loans (for those who buy loans as an investment) dropped (the fire-sale risk I described above) as money escaped from stocks. Blackstone's leveraged-loan ETF saw, by far, its worst outflows ever:

Overall, in the US, loan funds looked like this:

The $2.5 billion outflow in the last week of the graph set a record. Zero Hedge noted,

While many have voiced concerns about the risks inherent in a collapse in the loan market, among them the IMF, Fed, BIS, JPMorgan, Guggenheim, Jeff Gundlach, Howard Marks and countless others, concerns about leveraged lending were highlighted this week when Janet Yellen reiterated warnings that declining underwriting standards for corporate loans could lead to more bankruptcies and prolong the next economic downturn.... The most vivid example of the freeze in the loan market came late on Thursday, when Bloomberg reported that in a flashback to the events that culminated in the 2008 financial crisis, Wells Fargo and Barclays took the rare step of keeping a $415 million leveraged loan on their books after failing to sell it to investors.... The banks were stuck with hundreds of millions in unwanted paper.... The delayed transaction means the banks will have to bear the risk of the price of the loans falling further, as well as costs associated with holding loans on their books.

Highly leveraged loans are sometimes packaged like Mortgage Backed Securities into a single security called a Collateralized Loan Obligation (CLO). The difference between an MBS and a CLO being primarily that one is a package of mortgages while the other is a package of corporate loans, usually for corporations with low credit ratings.

As with those derivatives that took the global economy to its knees in 2008, CLOs begin as bank loans that are ranked below investment grade, which are sold to a CLO manager who bundles multiple loans (typically 100-250) into a single security and then sells stakes in that security called "tranches." (Remember how lovely that worked out in 2008.) The tranches are graded from higher risk to lower risk, paying higher to lower interest to the investor respectively. What could go wrong?

Well, liquidity is what goes wrong. If the underlying loans start defaulting so that investors want out, it may be hard for the CLO manager to sell off assets fast enough to pay people out.

And then a funny thing happened on the way to the market in December with respect to issuance of these CLO's:

Nobody was packaging new CLOs that month because so many CLO managers were rapidly unpacking them to sell off underlying assets in order to raise liquidity in order to keep up with investor withdrawals. That is the point when low-grade credit starts to seize up because banks can't sell new loans to packagers, so the channel clogs up all the way back to the banks, which stop issuing these kinds of loans.

The level of withdrawals from these kinds of assets late last fall bordered on panic levels. That says to me that the Fed backed away from its tightening suddenly for more reasons than just a crashing stock marke.

Here is what happened to leveraged loan prices during that same period when banks were not able to offload the loans they were issuing:

By the end of December, that chart I showed you above looked even worse:

Three straight weeks of record-setting withdrawals.

Bonds in bondage

The US has amassed $1.2 trillion in junk bonds held by institutions.

October, 2018: By October of last year, junk bonds, like leveraged bank loans, saw their worst performance since ... (yes, the comparisons keep pouring in) 2008. A big contributor to the near crash in junk bonds was the price falls in oil. High-yield debt started demanding an even higher yield. Corporate HY in energy climbed to yields that were 4.5% more than investment-grade bonds. Those selling bonds they had been holding, typically saw a 1.8% loss in value, wiping out 2/3 of high-yield gains for the year.

December, 2018: The US has amassed $1.2 trillion in junk bonds held by institutions. The junk bond market did something exceptionally rare in December. It froze over entirely. Not a single junk bond was issued. Given the large amount of low-interest junk debt that is maturing soon, this deep freeze in debt is a threatening situation. $110 billion in junk bonds and leveraged loans is set to mature this year and probably most need to refi (versus $36 billion last year). Next year $191 billion mature and $293 billion in 2021 and then $385 billion in 2022. So the problem of refinancing in this market just gets worse and worse if things start to tighten up again.

When a market freezes up like that, you have to offer substantially more interest on your new bond issues to attract buyers into the market and free credit up. Given that interest has already risen a solid bump up since the bonds that need to be refinanced were issued, a serious cascade of defaults is not some distant possibility that it is not likely to happen, but is a possibility growing more likely every year.

Besides the freeze, a serious quality issue emerged as the market started to play with real price discovery. Higher quality bonds began to slough off into the lower reaches. $176 billion in A-rated bonds got downgraded to BBB (the lowest investment-grade bonds) in the fourth quarter. (That number was reported two weeks before the quarter finally closed.) Fall below BBB, and bonds lose their investment grade, which forces many funds to catapult them outside the fortress walls. When BBBs start falling wholesale into the next basket down, you have a big problem because there are a lot fewer potential buyers so a lot more interest is required in order to compete for investor money.

January, 2018: Moody's noted rising refinance risk in high-yield bonds as corporations followed the path described above, moving the entire market toward a higher percentage of high-yield (junk) bonds as opposed to speculative-grade bonds and as interest on high-yield also rose (now averaging 7.26% as opposed to 5.84% a year ago), due in large part to the Fed's balance sheet roll-off.

February, 2018: Currently BBB credit, due in good part to these revisions downward from higher ratings, stands at an all-time high of 56% of the $6 trillion of investment-grade bonds in the US, and $6 trillion is 3x the amount of this kind of debt that existed at the start of the last recession.

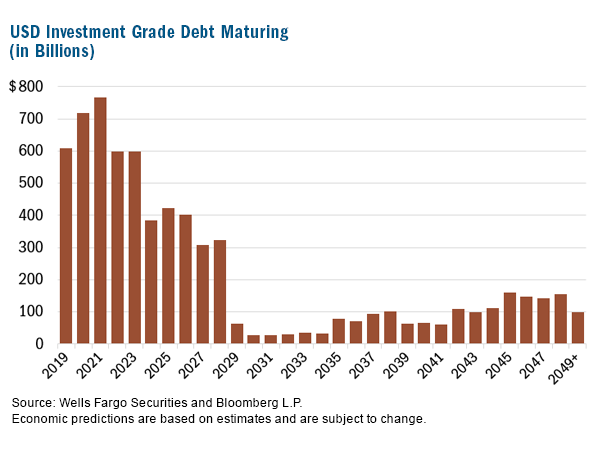

Here is a snapshot of the tsunami of corporate debt that is suddenly rolling over now at higher interest:

That $3.3 trillion in corporate debt that needs to be refinanced is the highest amount in US history and is greater than all the securities the Fed wanted to wipe from its balance sheet in its Great Recovery Rewind.

The mutating mortgage monster

One thing that is more stable this time around, versus during the Great Recession, is that the US does not have as many of those mortgage time bombs known as ARMs. By 2007 a decade-long ARMs race had created a leaning tower of loans in which few of the debtors could actually afford their loans. The whole nation pretended income would grow, making those Adjustable-Rate Mortgages affordable by the time the higher rate of interest kicked in (typically the fifth year of the loan).

Real income for the same job, however, did not grow at all; but some people in that much time did move up in their careers to better income. For the most part, detonation of this massive bomb was held at bay for a number of years by the continually rising value of real estate. That growing equity made it possible to refinance at an attractive fixed rate five years into the loan on the same income.

Those time-bomb loans are why I was certain, as soon as housing began to decline, that the US was going to experience a financial collapse great enough to tear the global economy to shreds. Simply put, those ARMs were sustainable only so long as housing prices rose, leaving a cheap refi due to strong equity as an exit strategy in the face of flat income. The decline of the housing market into a long-term slump set the match to the fuse.

Before you think we are safer in the present housing market decline because we have not issued as many of those daredevil loans, you may be interested to learn that millions of those loan implosions remain frozen in place from last time -- 10.6 million to be precise, totaling $2.4 trillion in outstanding balances. Many of those loans have never received a payment since they went delinquent.

Because I first saw the crisis coming when I was managing five-star resort properties in Hawaii, it is no surprise to me that the worst of this situation continues to be in Hawaii. While only 4% of these loans were more than five years delinquent in 2012 (five years after the crisis began to unfold), 68% of them are today. The second-worse state is New York at 55% today, then New Jersey and Washington, D.C., at 48%. A national average of 25% of these Great-Recession era loans are more than five years delinquent.

This situation exists because the number of homes that entered foreclosure was so great that continuing foreclosure would have crashed real-estate prices into such a pit that nearly all banks would have gone bankrupt. So, the Federal Reserve gave the banks permission to stop foreclosure and freeze the mortgage values on their book at their level at that time.

Debtors, however, quickly realized that the foreclosure freeze meant they could also stop making payments throughout the freeze without concern, and so they did and continue to do. Thus, most of those loans have not been paid down any since they were first frozen. (For details on how these mortgages were modified or frozen, click here.)

Thus, we live inside a game of pretend that keeps the banks alive because, if they actually wrote down the loans to market, many of those banks would go broke, and the bankruptcy of so many banks would have collateral effects that would likely cascade to all the other banks over time if there were no further Fed interventions. (In that sense, then, we're not doing much differently than Italy with all its carried bad debt.)

"So what?" you may say. We've been living in this suspended animation for a decade. We can continue to live in it. In fact, we have to because, if the banks all restarted foreclosure on all these underwater homes (even if they didn't add in all the years of accrued interest, fees and fines), they would completely crash the housing market by dumping millions of homes on the market.

Perhaps this is why many of the big loan agencies, including Fannie Mae, have stopped showing these homes on their graphs and reports. They are now just the mud we are perpetually stuck in as we live inside this game of economic denial wherein banks pretend they have a lot more value than they really do. The emperor has new clothes.

However, the game keeps falling apart and requiring new rounds of pretend:

Banks, mortgage servicers and the GSEs have been able to pull off this charade because hardly anyone knows how bad the re-default situation really is. Even mortgage pros don't really know that there is a problem. How could they? I am not aware of another analyst writing about this looming disaster. The re-default numbers you see in this article have been buried where few people can find them.

My problem with this situation is that, philosophically, I don't believe denial ever wins over reality in the long run. The banks can pretend they have hundreds of billions of dollars more in collateral than they do, but pretend collateral is not worth a cent. This is one of the many things I'm routinely referring to when I say "we have done nothing to resolve the fundamental economic flaws that created the Great Recession." It is why the Great Recession is still lurking as a huge pit beneath the\is mess of an economy the Fed calls "recovery." These kinds of faults in the foundation tend to crumble over time, so "pretend to the end" only makes the end collapse worse when it does come.

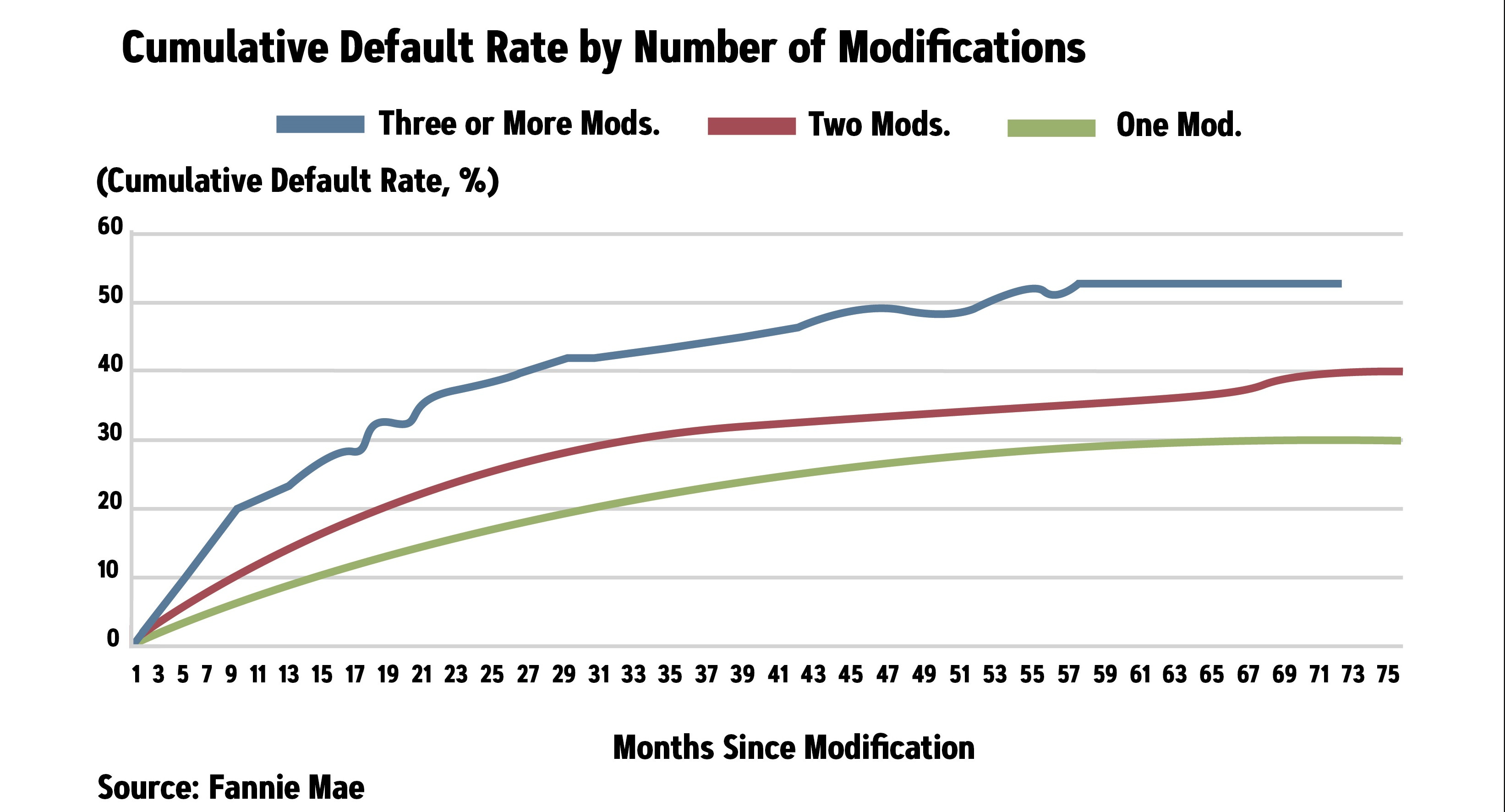

One of those problems is now surfacing. When these mortgages were modified in various ways, it was assumed eventually the borrower would be able to make good on the mortgage; but that never happened for most. As a result, the mortgages that were rewritten are beginning to redefault, bringing the old problem from the pit of recession up to the surface of the present. In 2017, JP Morgan showed that 47% of all its troubled financial-crisis debt that had been modified redefaulted. (In large part, that is because the banksters were too miserly in their modifications to be realistic in the first place.) For BofA, the number was 45%; for PNC, 57%. Wells Fargo was 35%.

Many of these restructured mortgages are now on their second or third modification, and statistics show that the more often a loan is remodified, the more likely it is to need to be remodified yet again:

How long can you sustain that game of leapfrog? (In an imaginary universe -- forever.) I think it is fairly obvious that many of these "homeowners" have no intention of ever repaying their loans. Their situation became hopeless, but the banks also became so badly entangled in the situation they created that the homeowners know their best bet is to live as deadbeats in their homes as long as they can and let the interest and fees and fines stack up forever, rather than become homeless; and banks don't want to foreclose because then they actually would have to write down the homes to value and report their losses. It's a mountain big enough to swallow entire banks if they ever re-open that Pandora's box.

If you still own Mortgage Backed Securities (MBS) -- the monster loan packages that brought down the world in 2008 -- or if you invest in the hedge funds that sucked up a lot of them, just know that a huge amount of this junk is still packaged up and buried within those black boxes. Investors likely know as little about the content of those packages as they knew back then.

Black Box Logic did a study of the worst of the worst of these loans, which it sold to Moody's in 2015. That study mysteriously hasn't seen the light of day since. The Securities Industry and Financial Markets Association, however, estimates that the worst of the worst of these loans total about $700 billion.

But here is a little sunshine for you: My guess is that buried within those loans are the worst-of-the worst loans -- the ones where mortgage issuers lied about doing their due diligence and took applicants' statements of income at face value or where they didn't even run credit checks ... because that is where you hide the fraudulent stuff -- in the rubble pile no one wants to sort through.

So, where is the sunlight in that? Well, I for one am angry that the Obama Administration, under the guidance of Attorney General Eric Holder, never did a darn thing to bring banksters to justice after the Department of Justice failed in its first case and gave up (because proving these cases is "too hard"). I have nothing but contempt for Eric Holder and Obama for either cowering before the difficulties of winning or (worse yet) just caving in to cronies.

The sunshine is this: I've been thinking the statute of limitations means it is now too late to go after the banksters who brought us the Great Recession who, then, floated on their own golden parachutes to safe landings. Maybe just maybe within this heap of true junk loans lies a mountain of evidence never disclosed, and the clock on the statute of limitations only starts ticking from the date when evidence of the crime becomes known.

Of course, the Trump Administration hasn't shown itself one bit more interested in going after the banksters than were Bush or Obama. So, my hope is probably misplaced.

Getting schooled on the student loan crisis

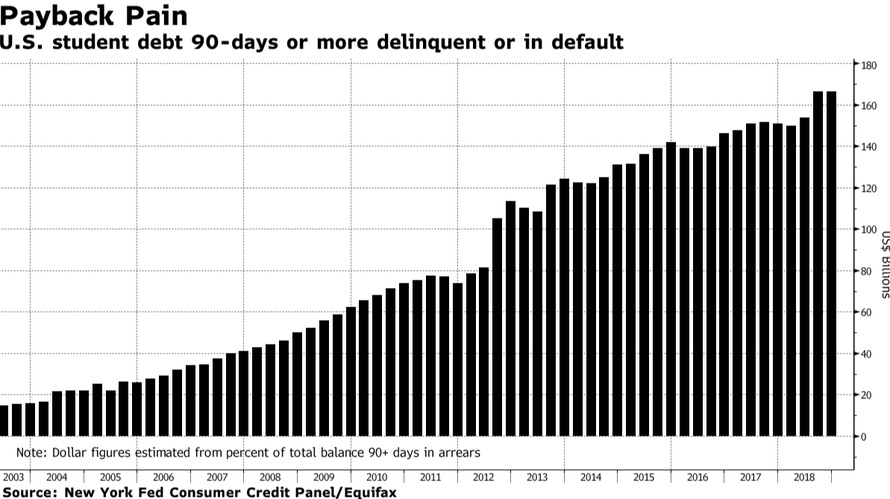

After a surge of delinquencies in 2018, $166 billion in student debt is now delinquent (ninety days overdue or in default). Of total household debt, excluding mortgages, student-loan debt is now the largest percentage, followed by auto loans, followed by credit-card debt, followed by the aggregate of all other debt.

The US job market has not brought forth the level of wage growth and entry career jobs needed for students to be able to pay off their debt, as the cost of tuition has rapidly outstripped raises in wages. Even the Federal Reserve recently questioned whether a college education is worth what it costs anymore because the cost-benefit ratio to the risk of not being able to pay off loans is so high.

These loans won't hurt banks because they are government guaranteed, so the problem rests solely on taxpayers -- at a level that is 400% of the amount of delinquent student debt at the start of the Great Recession and that is twice what the Federal government put out to bail out the auto industry during the Great Recession. No big deal. We'll add it to that great rubbish heap called "the national debt." Until then, it shackles the feet of the emerging generation.

Going forward

Back in December, Alisdair McCloud of GoldMoney offered the following scenario as being likely to play out in the first half of this year: (I don't know much about him, but the scenario read as reasonably likely to me now that we are seeing some of it already play. I've added my comments in brackets.)

We can now suggest the following developments are likely for the US economy. Warnings about an economic slowdown are persuading [we can now solidly say "have persuaded"] the Fed to soften monetary policy, a process recently set in motion and foreshadowed by US Treasury yields backing off. However, price inflation, which is being temporarily suppressed by falling oil prices, will probably begin to increase from Q2 in 2019. [We are only in Q1, and are already seeing oil prices rise fairly quickly again.] This is due to a combination of the legacy of earlier monetary expansion, and the consequences of President Trump’s tariffs on consumer prices.

After a brief pause, induced mainly by the threat of an unstoppable collapse in equity prices, the Fed will be forced to continue to raise interest rates to counter price inflation pressures, which will take the rise in the heavily suppressed CPI towards and then through 4%, probably by mid-year. The recent seizure in commercial bond markets and the withdrawal of bank lending for working capital purposes sets in motion a classic unwinding....

As result of the credit freeze and the falling stock market, the Fed slacked off dramatically (in Fed terms) from its tightening schedule. In a recent comment to one of my own articles, I noted that all the relief the markets now feel is due solely to the Fed backing away from its tightening schedule, and the Fed was only able to do that because inflation receded and gave them a window in which that was easy.

While that calmed things down, the Fed can only back away from its tightening so long as inflation cooperates. Inflation was down mostly due to falling energy prices, which are now back to rapidly rising, so inflation is likely to rise soon. If tariffs continue much longer, they will also drive inflation up, something I warned about last summer. Producers have done their best to resist passing along tariff costs, but they can only resist so long.

Thus, the Fed's ability to spare the market from the effects of its balance-sheet unwind and interest-target increases ends as soon as inflation returns. The Fed was fortunate to have hit a soft pocket in inflation right when it needed to back off, sparing the US stock market from a much larger crash. If the Fed's low-inflation window closes up, it won't be just stocks that go down when the Fed starts tightening again. The bond and loan markets will also return to seizing up just as they were doing in November and December.

Inflation also softened in December because retail sales fell hard, but that may have been an anomaly brought about by the government shutdown. Hundreds of thousands of federal employees who were kept from their paychecks all month and well past the holidays undoubtedly leaned out Holiday shopping. Now, with pay brought up to date and possible tax refunds, spending may rise, and inflation may return to where it was

These fractured markets began to break up during the Fed's tightening. Their collapse became enough of a concern to the Fed that it lost face and backed down from its stated plans. The resulting reprieve from this multi-market collapse of the Everything Bubble hangs on a single thread: inflation must remain low so that the Fed is not forced back to tightening, which would inevitably restart the same crash that was underway last quarter.

This economic situation has been called "stagflation," which refers to a time in which the economy is stagnant even as the Fed is forced to tighten to stop inflation. One of the several reasons I predicted a recession starting this summer (which won't be officially known until next January) is that I think inflation is likely to rise enough to force the Fed back to tightening, which would also end the hope of more quantitative easing as a way of avoiding recession.

All of these debt problems will become a credit crisis if the Fed is forced back to raising interest rates