Deranged Stocks Dodge Reality as Inflation Rises along with Interest Rates on the National Debt

With a cash register drawer full of Trump money, you will, at least, have toilet paper.

According to CNBC, the stock market is not ignoring the Iran War or the sustained soaring of oil prices. Stocks are rising due to magnificent economic reasons! The article, itself, will someday become a classic study of insanely deranged justifications for the market’s irrational exuberance.

First CNBC’s acknowledgement of the reality-denying insanity:

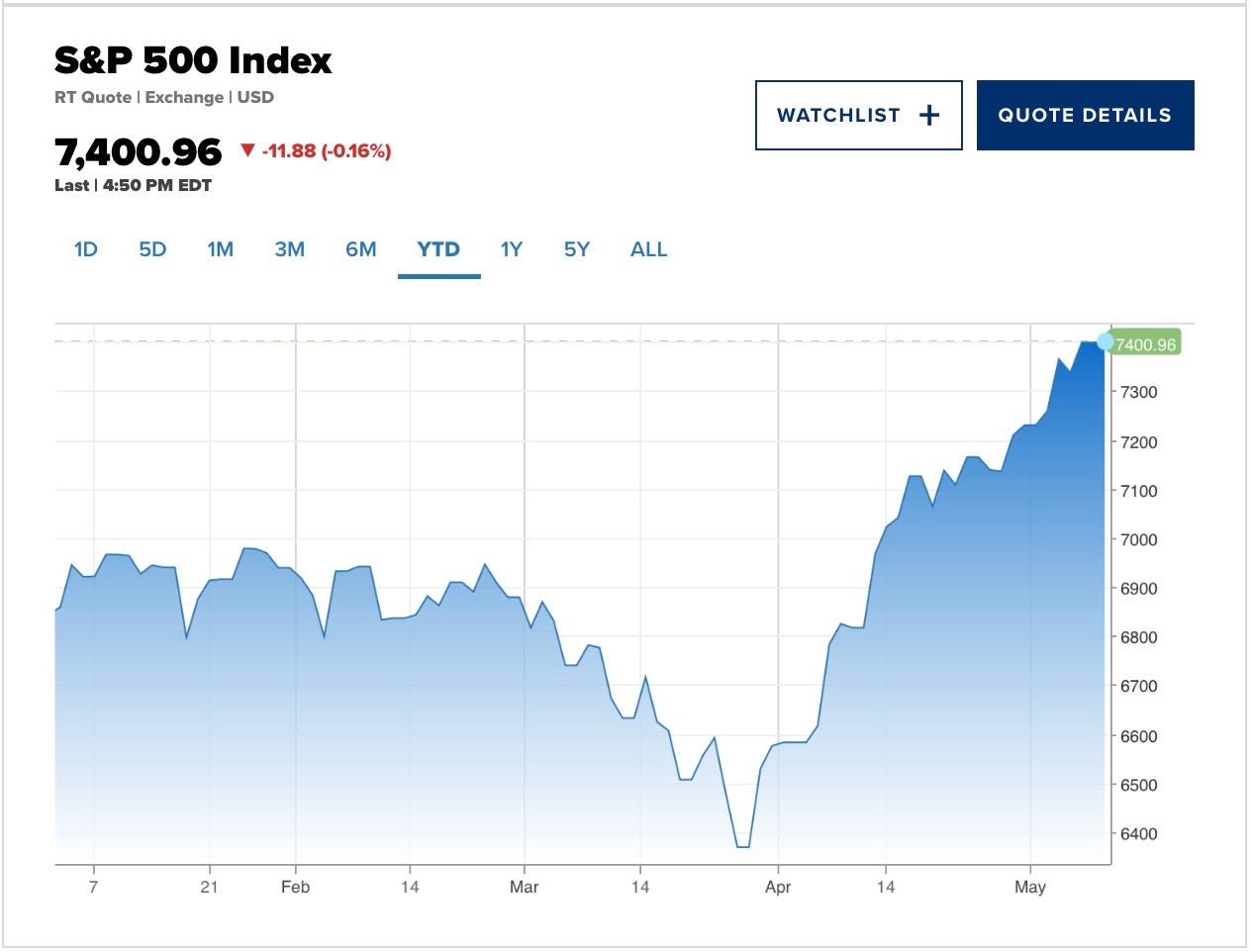

After a small early drawdown near the outset of the war, the S&P 500 has rebounded to all-time highs, closing above 7,400 on Monday for the first time ever even as oil prices remain at elevated levels….

Then the nonsense:

There are very real fundamental reasons for the comeback, including an economy much less reliant on oil to power it, strong company margins with energy costs as just a small input and tech companies whose businesses are insulated from the impact powering S&P 500 earnings forward.

Would that be tech companies like AI that demand enormous amounts of energy far beyond any spikes in demand humans have ever seen right at a time when energy costs are going through the roof for the reasonably distant foreseeable future? Are those the companies that are insulated from these forces? The article, itself, points out how AI is the driving tech force.

The index has made short work of recovering from its March low, having rebounded roughly 17% from around 6,300 in just a little over a month.

That it has done, indeed:

In rising, it has doubled the distance by which it fell when the war began. But that is insanity. AI and tech are far from immune to Natural Gas shortages and energy price hikes because they demand tremendous amounts of energy beyond anything we’ve ever seen by any industry and because the helium used to produce AI’s computer chips comes from NatGas. So, the article, itself, is lunatic thinking. These guys are smoking weed soaked in expensive crude oil, and their own smog cloud is making them delirious.

When the U.S. first struck Tehran on Feb. 28, the S&P 500 slid only about 8% peak to trough. In other words, it didn’t even fall … into a correction — defined as a fall greater than 10% and less than 20% — that theoretically would follow an energy shock rippling through the global economy.

Lunacy. A plunge SHOULD follow an energy shock ripping through the entire global economy if “very real fundamental reasons” were actually being applied to companies that demand extraordinary amounts of energy and helium, especially when we can all see that this energy shock is the biggest in history already with no clear end in sight.

Sheer lunacy.

At its height, since the conflict started, oil has climbed above $120 a barrel, and was last above $100. Gas prices have surged above $4.50 a gallon at the pump, and is above $5 in many states.

Brent is already pushing back toward $110 after Trump laid out how totally unacceptable Iran’s peace proposal was (because they were so anxious to make a deal, as I warned they were not!) and as Iran leadership said US surrender would have to be the answer to ending the current war.

The stock market continues to buy the Trump blabbergassing it has clearly been consuming with relish all the time in order to find endless justification for rising as its greed desires, but now even Trump is finding it hard to blab up a claim that the war will end soon. Instead, he was last seen going off about how stupid the Iranian people must be to not be coming to the table with something that looks even remotely like his demands.

A Trivariate Research review of 1,465 earnings transcripts since the start of March found that only 10% of the entire market cap of the U.S. equity market expect[s] a negative or even mixed impact from the U.S.-Iran war. The firm said that that 10% approximation is, if anything, an overestimation.

That is denial of some pretty starkly obvious realities. You can see the mania just in how CNBC crows about how narrow the profits are:

Indeed, the largest companies in the S&P 500 are now the most extraordinary they’ve ever been from an earnings standpoint. Apollo’s chief economist Torsten Slok pointed out that the 10 largest companies in the S&P 500 now account for roughly 34% of the index’s total profits, doubling from 17% in 1996. JPMorgan’s trading desk pointed out last week that earnings for the Magnificent Seven companies are outpacing the other 493 S&P 500 stocks by more than 40%, to levels not seen since 2014.

They know that a single sector of companies being responsible for the majority of profits being made in the entire market is a serious weakness, not a strength, but they are ignoring that fact by finding rationales to feed their greed:

To be sure, that massive concentration unnerves investors mindful of the risk in relying on just a handful of names. But the acceleration in earnings during the first quarter reporting season from tech giants, with quickly-expanding use cases for AI, and ballooning capital expenditures, has investors confident that market concentration is a feature, not a bug, and that the fundamental story in AI is intact.

And that is EXACTLY like the dot-com bust, which is how I have said this market is going to end.

A market expert who sees differently

Charlie McElligott, Nomura Capital’s quant guru, gives a much clearer view regarding the market’s insane positioning. He just pointed out how precarious the stock market’s rise really is, saying the materialization of any downside risk at this point could trigger an avalanche of 15-20% in just one day!

McElligott pointed out the obvious, which the article above missed entirely. He said the market is soaring on a “self-referential” feedback loop, which means it is susceptible to any external economic pressure that brings a significant change into the narrow view angle within the market’s blinders. As a market graph/data specialist, however, McElligott is not just pointing out some obvious logic, he is noting how internal market rhythms and moves in the data are showing hugely overstretched levels that indicate a big snap could come rapidly.

The market is looking only at itself and what is has been doing and betting on that to continue. That has become a self-fulfilling feedback loop. If any outside contradiction finally breaks through, stubborn investors who have only been looking within the loop to see what they want to see, may be horrified when they can’t find a narrative demented enough to explain it all away. Then the cascade will be calamitous. The factors McElligott listed that could accomplish that breakthrough are already so abundant and powerful that it’s incredible they haven’t already broken through:

Those include:

Inflation, which we know is rising again due to tariffs passing through and is also rising due to longterm high oil prices. That inflation just got a boost in today’s CPI inflation report, but watch what happens when a sudden massive surge of inflation makes it into the numbers. For now, a rise like today can still be shrugged off with a little more applied narrative about why it is transitory, even though it was larger than economists had expected and should be ringing an alarm about what is coming.

Interest rate increases, which became more likely after today’s inflation report. Today’s report revealed that the Fed’s target interest rates are now lower than actual inflation, making them stimulative of more inflation. Today’s lousy Treasury 10Yr bond auction with low participation even at higher yields also signaled that the bond vigilantes will be pricing through the inflation that Fed rates are falling behind on. This is going to make it hard for the incoming Trump chair to make good on the delirious hopes of further rate cuts when interest rises every time the Fed lowers its targets, making the Fed look stupid if it takes that path. Bonds would react grievously to announced rate cuts a this point. Even mores so a couple of months down the road when inflation is rising even more quickly.

Geopolitical events. Hmm, where are we going to find any geopolitical events powerful enough to upset the apple cart?

I’m going to save my analysis of today’s rising inflation report for my weekend Deeper Dive, but I will note that the government’s inflation report shows that items having little to do with direct oil impact on prices are rising more quickly now, too, though gasoline and petroleum-related prices were the main drivers. Those non-petroleum prices are likely the effects of the last year’s tariff regime coming through, even though the Supreme Court quashed most of those tariffs (while Trump reimposed some at lower levels under a different set of laws). It’s still a little too early to see the cost of oil pricing through to other items, as I’ll explain in my Deeper Dive.

The increase in today’s CPI inflation report for April is nothing compared to what is coming as Trump’s war is already dragging on far beyond any timeline he originally gave for how quickly the war would be over, disrespectful entirely toward his claim, which is now more than a month old, that he had already won victory.

(Articles to support today’s editorial and quotes appear in boldface among the following headlines for paying subscribers.)