Falling Back into Summer

Seasonal changes, even in economics, can swing back and forth

After I made much of the apparent labor-market downturn two days ago and the corresponding rise in unemployment, the market wants to prove me wrong on my claim that labor was beginning to turn, just as I thought it was going to do earlier in the summer, but then it flipped right back in favor of my position. This is the second swing this summer, and while most are seeing it as a sign that the labor market is still very tight, I’ll note in my slight defense that swings back-and-forth during transition are often a part of any kind of turning.

Where I live, for example, the first notable downturn in temperature, accompanied with some wind, occurred a couple of weeks ago, and I said to my wife that it looked like the turn of the season from summer to fall was here. After a couple of days, the summer swung back, and we had several days of hot sunshine.

“So how is that turn of the season?” she probed me as we sat trying to beat the heat in our shorts in a little shade. (She takes a certain satisfaction in pointing out when I’m wrong.)

“Just fine,” I said, making sure to sound unphased. “Looks like Summer is giving us an encore. But things swing back and forth like this sometimes at the big seasonal change.”

Two days later it was overcast, lightly raining and twenty degrees cooler; but today a warm weekend entered back into the forecast. So, back and forth before the weather settles into its autumn groove.

That example is not to say the labor market will not prove me wrong by remaining tight for months to come, or that I’d be terribly surprised if it did; but it is true that there are typically no straight lines to anywhere in economics, and that changes — whether in weather or economics — sometimes have a hard time making up their minds at first.

The big news today, which sent the NASDAQ to plucking its own tail feathers in a fourth day of down-spin on the “good news is bad news” plan, was that jobless claims fell back to their lowest since February, while productivity soared. Our stock market full of Fed addicts has for years now hated nothing more than even the slightest appearance of a good economy.

This was the fourth straight weekly decline in jobless claims, so that looks pretty trendy and doesn’t look good for my opinion that the labor market was just beginning to show signs of making a turn downward (i.e., unemployment upward). It does look like the economy will be holding the Fed’s feet to the fire awhile longer, putting those free Fed meds for the addicts further out of reach, which put the market in a pout today (the Fed having long run a sort-of San-Francisco plan for supplying its addicts every time they face withdrawal).

Economists thought new claims for unemployment would rise, so they were caught more off-guard than I was, as I wasn’t quite prepared to say the turn was that solid yet, but a flip back to a six-month low in new claims wasn’t in my sights either. Continuing unemployment benefits, which have a little more duration, also went lower.

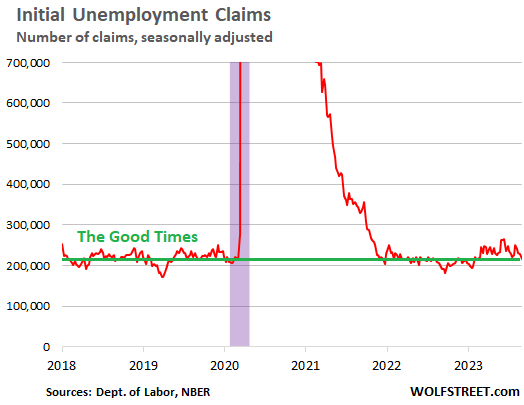

Nevertheless, the unemployment rate is at 3.8% where it rose to from 3.5%, but another week like this will be enough to overturn that, too. Even with the flip, you can still see evidence of a turn over a longer stretch of time, but it is mighty thin:

We’ve gone from the good side of Wolf Richter’s “Good Times” line, which is the underside when it comes to unemployment, to riding along the flip side of the line. We’re still in rare territory for unemployment so low it has only been experienced during a couple of short periods in the past half century.

That said, I’ll note again, how recessions start shortly after the upturn in the unemployment as well as in initial claims; and this upturn in unemployment claims, even with today’s jog down, has as much of an upswing from its low point as any of them get before the recession begins:

Continued claims in this anomalous labor market, however, are not playing along:

“So, how’s that change of the seasons coming, Honey?” She asks again.

“Don’t know, but I think I need another cold beer … and a frosty mug.”

On the other hand, that dollar rally I’ve been speaking of as being secure for now is coming along great, especially if the Fed is pressed to keep tightening, which is likely since the Fed relies on unemployment as one of its main gauges for when to stop. It’s set to be the longest rally in years, while that “major, biggest-ever in history” prop of the yuan that China made yesterday … already failed again, leaving the yuan still at its weakest since 2007 after the longest string of props in Chinese history.

As for that inflation equation, it’s coming in hotter. Canadian inflation is solidly back to rising, and gasoline prices are rising in the US. It was the drop in oil prices that gave inflation a rest since oil goes into everything in one way or another, and Joe’s favorite murderous friends in Saudi Arabia, thanks to Joe’s sturdy fist bump with the Prince of Petrol, are going to keep the heat up through the end of the year on prices. Others are now writing that CPI is expected to rise because of it. That would match my twin forecast on that matter from the start of the year — oil rises, inflation likely does with it, though not entirely due to oil.

So this is the year-over-year percent change of the average price of gasoline on a weekly basis. And it’s another setback for the Consumer Price Index to come. “Disinflation” good bye.

Yes, bye for now.