Fed Tightening Impacts Markets: How Fast and How Furious?

The Fed has a solid track record of killing its children and eating them, which is to say destroying all of recoveries it worked so hard to originally nurture. This it does by how it shifts into tightening mode with a jolt, almost always taking down the stock market with it. This time is no different, except likely to be worse for the reasons I'll lay out below, and we already see it happening.

Recap

My thesis to all of you last year was that the big money moves to watch out for in 2021 would be inflation continuing to rise (from nothing where it was when I started writing that back in 2020) until it finally forced the Fed to taper sooner than expected and then to taper faster than it first announced. It would play out that way because the Fed would discover as soon as it began to taper that it was already behind the curve due to its fantastic belief that inflation was transitory.

I also said that tapering, itself, would be tightening because of how the bond market would take over interest rates and push them up as the Fed stepped back from covert yield-curve control. This would happen this time when it didn't during past tapers, which is why investors and analysts aren't expecting it to happen now, because this time bonds have some serious inflation to price in. As the Fed's taper releases the Fed's white-knuckled grip on the bond market, bond yields will to start to shift back to real price discovery, and that rise in yields due to severe inflation will impact the stock market.

Ta da! Here we are. The question to cover now is just how fast is the Fed going to increase the rate at which it tightens? Below we'll see that the Fed is already talking about leaping from tapering immediately into all-out tightening ... and I do mean all-out. That is something neither the Fed nor any analysts were talking about as a scenario for 2022 a couple of months ago.

Fed on the run

Only two months after the Fed made its first tapering announcement, January has already given us proof of the scenario I've been laying out. Just look at how quickly the Fed is having to accelerate its tightening to catch up with inflation. As the Fed accelerates, investment analysts are already saying the bond market's big moves and stock market's big gyrations from the start of the new year are almost entirely due to investors being surprised (they shouldn't be) to discover the Fed is going to have to move a lot faster and harder on inflation than they ever thought the Fed would do:

Investors have been preparing for the Federal Reserve to start hiking interest rates. They also know the central bank is cutting the amount of bonds it buys each month. On top of that, they figured, eventually, the tapering would lead to a reduction in the nearly $9 trillion in assets the Fed is holding.

What they didn’t expect were all three things happening at the same time.

But minutes from the Fed’s December meeting, released Wednesday, indicated that may well be the case....

The jolt of a Fed triple threat of tightening sent the market into a tailspin....

“The reason the market had a knee-jerk reaction yesterday was it sounds like the Fed is going to come fast and furious and take liquidity out of the market,†said Lindsey Bell, chief market strategist at Ally Financial. “If they do it in a steady and gradual manner, the market can perform well in that environment. If they come fast and furious, then it’s going to be a different story.â€

If investors had paid attention to this blog, they would have been expecting all of this. There would be no surprise in seeing the Fed has to scramble to catch up with inflation. Inflation has grown so hot, as promised, that it pressed the Fed to start talking about tapering, interest tightening, and even quantitative tightening where it reduces its balance sheet before the Fed has even seen what its tapering can accomplish. It has done all of this in a single December meeting that came right after its first announcement of tapering.

While the Fed initially indicated it anticipated that the inflation threat would subside after a short period of time, its view has changed. Chairman Powell now anticipates inflation remaining elevated “well into the middle†of 2022. In December 2021, he announced a plan to cut in half the monthly $120 billion in bond purchases by the Fed, with the entire strategy likely to be curtailed by March 2022.

While the Fed’s choices related to buying bonds tends to affect interest rates on the long end of the yield curve, setting the target fed funds rate directly impacts the short end. Through much of 2021, Chairman Powell stated frequently that the Fed would not likely adjust short-term rates from the current “near zero†level until 2023. That plan now seems to have shifted, and following the December FOMC meeting, Fed officials indicated there could be at least three rate hikes in 2022.

Calling inflation a severe threat, chairman says central bank is preparing to raise rates and shrink asset holdings.... “If we have to raise interest rates more over time, we will,†he said.... "Inflation is running very far above our target."

So, they've piled on everything -- the taper, then planned interest-rate increases, and even shrinking their balance sheet at the same time and the even more interest rates increases over time if necessary ... all because "inflation is running very far above our target."

Yet, people who don't read these patron posts still are not fully understanding what is happening. (Be glad you're not one of them.) Here is proof. Pay attention to why the following person believes what he wrongly believes about inflation (and he's an expert):

“Inflation data is becoming a bigger issue for the Fed,†says Eric Freedman, chief investment officer at U.S. Bank. “Yet we believe that the trend from here could be that inflation goes down, rather than keeps going up, from current levels.†Freedman notes that long-term interest rates, such as the yield on 10-year U.S. Treasury notes, are holding at levels below 2%. Historically, interest rates tend to track with inflation trends, but that didn’t happen in 2021. “The market is saying that it doesn’t believe this inflation move is sustainable,†says Freedman.

What they don't understand -- even though it is so basic, as I keep saying, and is right in front of them -- is that bonds CANNOT price in inflation ... yet. The Fed is still the whale in the bond market, though not as much as it used to be. Therefore its bond hoarding is still weighing against natural repricing in the market. Nevertheless, we've already seen the bond market rise in interest far more quickly than is normal as the Fed has started to relax its grip.

What we also are seeing is a dynamic I talked about before it happened: As money flows out of stocks and into bonds when yields rise, that presses yields back down in a seesaw effect as the markets seek to find a new equilibrium. That is why I've said the fall of the stock market is likely to be a process this time, as it was in 2000 and the years that followed because it is bonds that are leading the way. Stocks are not likely to Gove over a big waterfall plunge like they did in March of 2020 when we were suddenly besieged by COVID and our own stupidity in destroying our economy. Bonds will keep trying to rise, and each time they do, more money will flow out of stocks and into bonds and keep the bond rise somewhat under control. That is a mitigating effect, but the bond market has a LOT of repricing to attempt because inflation is not relenting, and that means a lot of sucking money out of stocks.

This battle between stocks and bonds will intensify as the Fed moves further out of the bond market, leaving the Fed with less and less control over bond pricing/yields. In the meantime, major analysts like Freedman are still basing their inflation predictions on what bonds are doing as if bonds control inflation, rather than respond to it. The inflation is already there; we don't need bonds to tell us it is coming. It is already way beyond anything bonds are pricing. And the reasons for inflation -- huge amounts of accumulated Fed money in the economy and huge product shortages are not abating yet, and will take time to change. These analysts are thinking if a Fed-controlled bond market even CAN price in inflation! So, they're asleep at the switch, not thinking about why price discovery left the bond market in the first place and how it will return as the Fed exits.

Therefore, watch their surprise all over again and future revisions in their forecasts as the Fed finishes its taper and bonds fully return to open-market pricing, but especially watch as the Fed is forced by that inflation that people don't want to believe in to tighten faster than they believe it will.

Regardless, US bank sees the Fed's moves as having the same kind of effect I do. They just think inflation will back off and the Fed won't have to move as fast as it is now saying. Those effects are:

In light of the tapering strategy and the prospect that rate increases could occur sooner than originally anticipated, investors should prepare for possible impacts.

Fixed income market. Much of the focus will be on changes in interest rates. The Fed ending its role as a buyer in the bond market will result in less demand for bonds, which could put upward pressure on interest rates....

Residential real estate. If the Fed also tapers its purchases of mortgage-backed bonds and eventually brings that process to an end, mortgage rates could go higher....

Equity markets. Persistent high inflation rates may result in higher interest rates, which could affect calculations of projected future cash flows that analysts use to determine the present value of a stock.

Let's look at how rapidly things have already changed to see if these bankers are right in thinking the Fed won't have to move as quickly as it now says it will on their presumed basis that inflation will cool just because bonds are not pricing as much inflation in as the Fed finally says is likely coming. (They haven't been right once so far.)

Federal pedal to the metal

Only it's the brake pedal. Yet, it's more than the brake pedal because the Fed is already talking about shoving into reverse while economic stimulus still has forward momentum and hitting the gas in reverse to spin the tires backward.

First, look at where we are in the tapering process right now.

For the past two years (roughly) the Fed has been purchasing $80 billion in treasuries every month. That is as much stimulus as all of the bond purchases -- treasuries and mortgage-backed securities -- under QE3 just in the treasury side of its purchases.

At its last meeting in mid-December, the Fed's Federal Open Market Committee (FOMC), which sets monetary policy through such operations as bond purchases, decided to pick up the pace of its taper to where it would be down to adding only $60 billion a month in total bonds to its balance sheet in January.

That is already halfway down from the $120 billion it was buying and holding in treasuries and MBS combined, but that is still 3/4 as much stimulus as QE3 -- the Fed's largest quantitative-easing stimulus program until this last round through the COVIDcrisis. That means we we are still at a highly accommodative level of easing, not tightening. So, OF COURSE, bonds are not fully pricing in inflation yet! How can they? Tapering has just begun. The Fed is still the whale in the pool. However, all of that is now changing rapidly, and we can get a sense of that rush by seeing how much the Fed has already had to pick up the pace from each announcement it has made and how much market analysts have already moved their own predictions:

The Fed originally said in its October meeting it would taper at the rate of $15 billion less in bonds each month, starting in November (and continue at that rate until it was done with QE); i.e., until it was done expanding its balance sheet by creating money to buy and hold bonds. In its December meeting, the Fed already doubled down on that to cutting back total bond purchases by $30 billion, and it said it will increase that monthly reduction, starting in 2022. So, it is scrambling, running behind the curve and trying to catch up.

The Federal Open Market Committee’s moves, approved unanimously, represent a substantial adjustment to policy that has been the loosest in its 108-year history. The post-meeting statement noted the impact from inflation....

For the Powell Fed, tightening policy now marks a dramatic pivot off a policy enacted just over a year ago. Known as “flexible average inflation targeting,†which meant it would be content with inflation a little above or below its long-held 2% target....

However, as the “transitory†narrative came into question and inflation began to look stronger and more durable, the Fed has had to rethink its intentions and shift gears.

But that is now the least of it.

The Fed has now said it will ALSO likely start raising interest rates this winter or in the early spring, something that had not been anticipated until the end of 2022.

On Wednesday, San Francisco Federal Reserve Bank President Mary Daly became the latest U.S. central banker to set her sights on a rate hike in the next couple of months.

I.e., by March. And Daly is one of the Fed's doves!

"It's really time for the U.S. central bank to start removing some of the accommodation we've been giving to the economy," she said in an interview on the PBS NewsHour. "I definitely see rate increases coming, as early as March even...."

Coming from Daly - who as recently as November was calling for policy patience in the face of rising prices - the remarks are a clear signal that Fed policymakers are getting ready to put an end to the pandemic era of near-zero interest rates....

Atlanta Fed President Raphael Bostic said he expects the Fed to raise rates three times this year, beginning in March, and to shrink the Fed's massive balance sheet rapidly....

St. Louis Fed President James Bullard told the Wall Street Journal later in the day that he now sees four rate hikes, starting in March, as a likely scenario. Just last week he had said he expected three rate hikes.

And Cleveland Fed President Loretta Mester on Wednesday told the Wall Street Journal she supports starting rate hikes in March and reducing the Fed's balance sheet "as fast as we can conditional on it not being disruptive to the financial markets."

We've gone from Goldman Sachs predicting two rate hikes for late 2022 last year to three to Fed dove Daly saying she would support two or three, starting as soon as the taper is complete, then to other Fed presidents predicting three and then four to Fed presidents saying they also need to start quantitative tightening immediately after the taper is complete by reducing their balance sheet ... and doing even that as quickly as they can.

Moreover...

It's not just the regional Fed bank presidents, whose views are sometimes at odds with the core group of Fed policysetters in Washington.

"The economy no longer needs or wants the very highly accommodative policy that we’ve had in place to deal with the pandemic and the aftermath," Fed Chair Powell said at his renomination hearing at the U.S. Senate on Tuesday, flagging coming rate hikes, as well as a reduction in the Fed's $8 trillion balance sheet.

So, the big guy, himself, is all on board with moving straight into balance-sheet reduction. Therefore...

"If you don’t see the March rate hike at this point, you are just dull-witted and nothing the Fed can say now will help you," tweeted SGH Macro Advisors chief U.S. economist Tim Duy....

Indeed.

All of this is even more change more quickly in the Fed's stance than I expected, and I am the one who has been predicting since before the Fed started tapering that it would find it had to run as fast as it could in picking up the pace to meet inflation because of how it was lagging due to its "transitory" narrative. It doesn't pay to pretend as the Fed did. Even Powell has now told congress that "transitory" wasn't a particularly helpful term.

I've never seen the Fed run like this!

Inflation's scorching breath burns up bankers everywhere

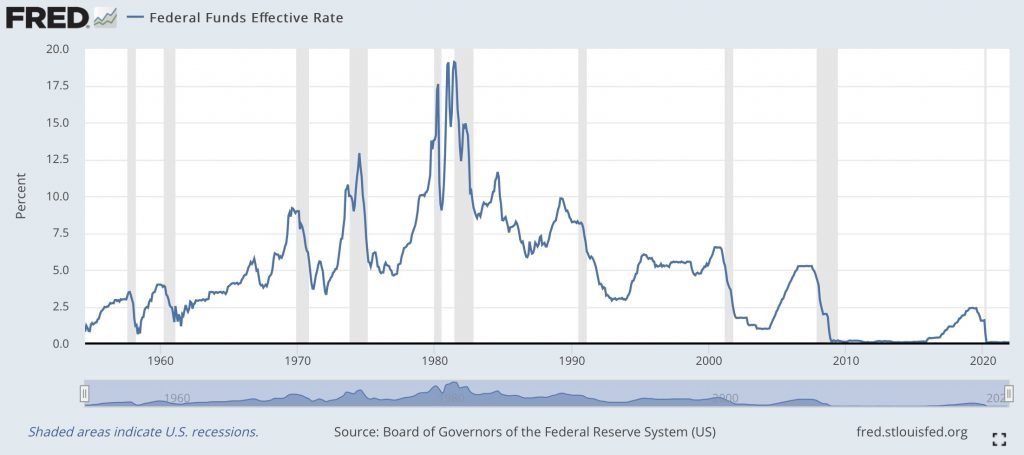

Last week, we saw that CPI is now at 7%, clearly hitting the levels we haven't seen since late seventies and eighties, yet the Fed is STILL in stimulus mode! We've never seen the Fed in stimulus mode with inflation this high. So, this shift from accommodative policy to inflationary tightening by March is likely to be the most jarring shift we've ever experienced. When the Fed started tightening down on the inflationary screws back in the early eighties, it was not in a high-stimulus mode when it realized it needed to make that shift. The Fed funds rate had been at 5% or higher for years before it began its big rate hikes under Chair Paul Volcker's determination to curb inflation, not down at zero where it remains now, yet look how high they had to raise their minimum interest rate:

The Fed also didn't have a massive balance sheet it needed to unwind at the same time back then. And we already saw how the combo of balance sheet unwinding and interest hikes went down in 2018 when the economy, flawed as it was, was in far better condition than now and when stocks, overvalued as they were, were far from being as absurd as they have become since then. Look at how the stock market became much more volatile in 2018 when the Fed was unwinding its balance sheet all the way until it went back to full-on QE in 2020: (Ignore the arrows from when I used this graph previously, except to the extent that the top arrow shows how the market fell apart in increasingly lower bottoms.)

So, how is it even remotely possible -- during the middle of an ongoing global pandemic with huge supply shortages everywhere and skyrocketing inflation -- that this sudden reversal into outright tightening and rate increases is not going to go worse than it did at the end of 2018?

This suicidal reversal would be unthinkable stupidity if not for the fact that the Fed has no choice but to raise interest rates as soon as its taper is over because interest rates will be rising, regardless of what the Fed says its target is, once the Fed is finished with its balance-sheet-expanding bond purchases. The Fed will look out of control if it doesn't make the rise sound intentional. This is the trap I've said all along the Fed was painting itself into. It is now making a suicide pact with the nation to assure everyone it has this under control.

Ask yourself, how much sense does it make that the Fed is still actually increasing its balance sheet right now (just at a slower rate of expansion) when it already knows it will have to start shrinking it less than two months from now? Why wouldn't you end all balance sheet expansion right now so you can ease more gradually into rate increases, except that you know you are going to see rates go nuts as soon as you are out of bond buying. You know you also cannot really wait because inflation is surging.

And to think Daly said the Fed needs to start tightening now because if it waits longer, then it will have to tighten quickly, and that, she noted, is how the Fed typically throws us into a recession. We're not already facing "quickly?"

We're going to go from a still fully accommodative mode -- equal almost to QE3 -- to the start of the Paul Volcker days in less than two months because the Fed knows it already needs to be there because it resisting fighting inflation for too long, but it just can't shift that abruptly without crashing everything. We've never attempted anything like this before. Not even close. So, buckle up, Buttercup, because shifting into reverse and going gas-backwards when we're still going sixty-miles per hour forward ain't gonna be pretty.

Then stop to think about the fact that, in previous tightening rounds when that didn't go so well, some other central banks in the world were still easing, which meant a lot of their money kept flowing into US markets. This time around, all central banks will be tightening at the same time because the inflation incinerator is global.

So, park your money in the safest spaces you can think of until you see where all of this going. My money has been to cash, inflation-protected bonds (not any other kind), commodity ETFs and real-estate ETFs, but those are not entirely safe either. They are just the safest places our 401Ks have as options. I anticipate shifting out of real-estate when mortgage rates start to feel the pain, which won't be long.

Beware that crypto currencies are highly speculative, and we've never really seen how they endure this kind of financial upheaval. Some consider them safe as an alternative. Maybe they're right, but I'm not so sure. The Fed's plan is to strengthen to dollar against inflation by raising bond interest, but it can't do that without crashing stocks. That may raise its value relative to other currencies, including crypto, too. QE weakens the dollar. QT intends to strengthen it in order to battle inflation. How that settles out for cryptos, I really don't know.

And, then, of course there are precious metals, but keep in mind tightening usually means strengthening of the dollar; but this tightening will mean destruction of stocks and of bond funds that are heavy in low-interest bonds and financial damage for any bond investors who are stuck holding their low-yield bonds in a tide of rising inflation or selling them at a loss because rising yields equal falling prices. It's going to get messy, so look for stable places to stand.

The stock market's revolt since tapering was first announced

Bear in mind 40% of the NASDAQ 100 has already crashed 50%, while 2/3 of the NASDAQ is down more than 20%. Wall Street is already flowing with blood for many. So, what constitutes a "crash" is relative to what portion of the market you are talking about. Half of the market has already crashed deep into the bear's forest. We just can't see the forest because of the trees. If you ask me, with the Fed's projected rapid shift from its year's high flying, all markets are looking at Armageddon.

But, in the very least, it ain't gonna be pretty.

You can see where the stock market has gone in the past when stocks have ventured this far past the edge of the bear's forest (meaning when indices have kept climbing even when most stocks were in their own bear market):

We've never broken this level of individual stocks in bear markets without an almost immediate stock-market crash for the entire index of, at least, 20%. The graph above is logarithmic, essentially showing drops as percentages of the market's total value at the time. Bear in mind the 2020 crash happened as the Fed was going into hyperdrive stimulus mode during a pandemic lockdown. This time we have pandemic lockdowns to a lesser degree, but shortages from past lockdowns to a much higher degree as lockdowns still continue, and the Fed is slamming into full reverse.

Here are the words of a permabull I generally consider so rosy-eyed in his optimism that I get nauseated reading him because he's a high-sugar diet, but look at what he has to say:

The Fed's proposed increases will raise the Fed funds rate to 1%. That won't come close to quelling 7% inflation.

The last time we had 7% inflation the Fed funds rate was 11.5%.

Investors are going to have to see results on this issue very soon. The knee-jerk reactions we have seen to a "headline" will look like a walk in Disney World compared to what unchecked and entrenched inflation will rain down on the economy and investor portfolios.

Facts and Truth are unpopular subjects because they are unquestionably correct....

Seeking Alpha (emphasis his)

So, get ready for massive Fed rate hikes to curb inflation or massive negative stock market responses to unchecked inflation. In other words, either way, buckle up, Buttercup! (This is why you read here -- at least partly -- be be forewarned so you can consider moving ahead of the dull masses, but the thinking needs to be your own based on your own situation. Ideally, you already made your own preparation based on what you've read here in prior months because we are now at the point where land masses have already started to shift.)

This permabull goes on to note that transformation as follows, some of which has happened in just two weeks of this new year:

Investors have witnessed a stealth BEAR market occurring under the surface of the major indices….

IPOs … down ~30% since they saw a peak in February of last year. SPACS, the "meme" stocks, and Alternative Energy have been punished. Other speculative areas like HIGH growth PE stocks and Cryptocurrency have been clobbered since the start of the year. In short, this market is rapidly unwinding many of the most speculative excesses of the past two years to start 2022, and the trend hasn't slowed yet....

I've shared a few stats over the past month that show that we may have already lived through a stealth correction or bear market, and it's hard to argue against it when we see more statistics like this.

And that's from a permabull!

Look at the following graph and ask yourself, in the present microenvironment, which line is most likely to step in line with the other:

Notice that several major banks reported this week, and their stocks didn't exactly rise.

Says the permabull,

We just witnessed a bloodbath in the HIGH PE stocks, but the larger mega-cap names in Technology also took a hit. With sentiment changing, it is time to put this group in perspective and investors may have to tread carefully here.... At some point "everything" reverts to the mean and enters consolidation phases. "Value-Tech" is not immune. They have been market leaders for a very long time.

I'm not suggesting a blood bath in technology, but I am seeing signs that it won't be so easy to navigate this area of the market as it has in the past.

The best a permabull can say is that it might not be a bloodbath, but it will certainly be rough.

The Fed takes center stage, but they will need a lot of luck and plenty of assistance to thread the needle in fighting inflation while trying to keep the economy afloat. Hope is not a strategy. Anyone hoping that we see a change to policies that help the situation may want to rethink that strategy.

Even the permabulls are seeing the possibility of a lot of red now, to where the best they can say is it might not be a bloodbath BUT that will take a lot of luck. Better hope for really solid earnings as businesses start reporting in for last quarter.

However, on that note, another advisor at Seeking Alpha writes,

The big headline on Friday was the poor December retail sales data which declined by -1.9% month-over-month, compared to the consensus for a flat readout. The result was blamed on a combination of persistent inflation which has pressured consumer budgets, along with ongoing Covid disruptions. This follows what was already a soft November retail sales report last month on top of a disappointing miss in December payrolls along with poor consumer sentiment.

And, of course, with the dollar rapidly losing value to price inflation, earnings would have to be up just to mean sales volume was flat because prices are up, and sales are measured in dollars, as are earnings -- dollars that are rapidly declining in purchase power (different than their relative value in the Dollar Index to other currencies because all of those are also declining in purchase power). The whole world is experiencing high inflation.

So, consider the following:

In other words, there is a lot of room to fall as bonds pressure stocks to reprice for inflation and as the Fed sucks away the money supply that has fed into the stock market and does so right as the economy is faltering.

Recession warning dead ahead

And what does this say for GDP in 2022?

The timing here is critical. It was only into the final two weeks of December that Omicron cases began to surge through the holidays which made headlines through thousands of flight cancellations and also other businesses forced to temporarily close with workers out sick. As it relates to the December retail sales data, keep in mind that it was largely business as usual for most of the month while the bigger hit came into the final week.

The Fed has placed its bet for 2022 GDP around 2.9% growth, but clearly the trend has already been down, and the final couple of weeks of December in retail show that GDP could be falling off a cliff. However, it is to "real GDP" that we will have to look to know what the economy is doing because inflation-adjusted GDP will go negative in the first quarter. Headline GDP may only be spared a hurl into recession by the fact that it is measure in inflation-damaged dollars. Yet, in December, even in those weakened dollars, retail was still down 1.9% from November, and November had already gone soft. (Remember one of my predictions was that we'd be going into recession at the end of 2021.)

Into January, the Covid data has continued to deteriorate including a record number of hospitalizations with schools either canceling classes or moving back to remote learning. Companies have also pushed back return-to-the-office plans. It's fair to assume that retail sales are poor at the start of the year which represents a direct hit to current Q1 estimates for corporate sales and revenue growth.

As I've warned we'd see a number of times, the Fed is now being forced to tighten, just as the economy is spiraling down due to more COVID wreckage from shutdown businesses. And, if Joe Biden's Build-Back-Better budget doesn't get approved, $18 billion a month in government stimulus checks since last July for the Child Tax Credit (CTC) payments just came to a screeching end this month. That's an average of $444 per month per family. So, take that out of retail sales, restaurants, etc. and other household spending, and tell me that the end of fourth quarter isn't sliding into recession as I predicted it would. It certainly will be in "real GDP."

All of this not exactly a good environment for the Fed's fastest switch from mega easing to rapid tightening. So, rots o' ruck and buckle up. There is turbulence ahead, and the Fed's downdraft has barely begun.

![By Lucian.amarii (Jup) [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0) or GFDL (http://www.gnu.org/copyleft/fdl.html)], via Wikimedia Commons](https://substackcdn.com/image/fetch/$s_!Ld09!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff90bc0e7-071b-4954-9dcb-3772f7fa3764_449x604.jpeg "By Lucian.amarii (Jup) [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0) or GFDL (http://www.gnu.org/copyleft/fdl.html)], via Wikimedia Commons")