Fed-up and Failing: How FedMed Killed the Patient

When The Great Recession Blog was conceived back in early 2011, I wrote the following statement to my friend Stan who was thinking about developing a website of his own, which became the core theme for this site:

I think focusing on the economy from the perspective of economic sustainability might be better. I don’t know if there are sites that take the critical stance on the economy rescue efforts that you and I have taken in our exchanges. The present approaches to economic rescue are so UNsustainable.

I thought it would now be interesting to walk through how the Fed's economic rescue plan played out over all the years since that proclamation.

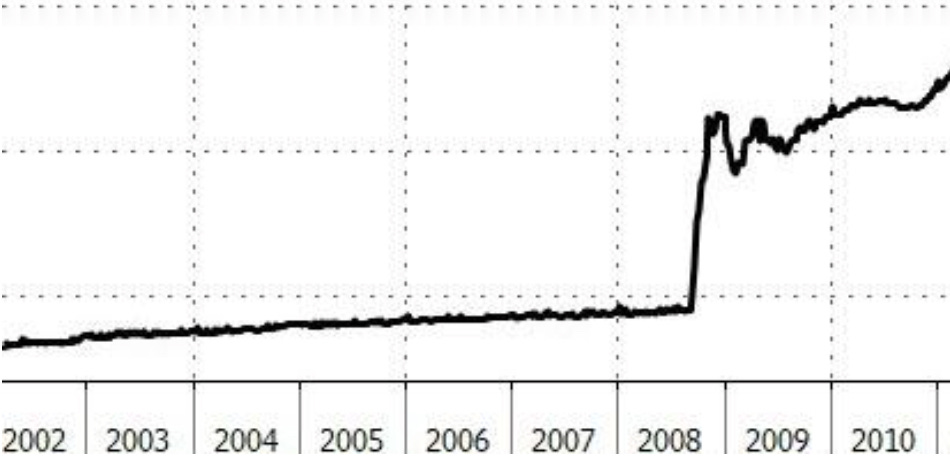

At the time I wrote that and started my site, the Fed's effort, in terms of all its economic stimulus was right here:

As you can see, the Fed had been trundling along for a very long time at a rate of balance-sheet expansion that would keep up with the growth rate of the population and the corresponding growth rate in GDP. If the Fed didn't add money as the populace and gross domestic production grew, then products and services would drop increasingly in price (deflationary) because production was rising with population growth, while money per person would become more scarce; so people would have keep a tight reign on what they spent. Businesses would have to lower prices because there was only so much money going around; so, with so much more out there in goods and services, they would be competing for a smaller piece of the money pie.

That's all a way of saying that line of growth made sense, although its rate of rise targeted 2% inflation, rather than a neutral level of money to sustain the economy.

Then along came Fed Chair Ben Bernanke's economic rescue experiment back when the Great Recession began in 2008, and it blew all former monetary expansion out of the water. As you can see, the Federal reserve tried tapering that a little at the start of 2009; but the taper went poorly, so they boosted things back up right away to about where they had been. Later in the year, they tried to taper again, and the taper went poorly again; so, they began a trek of slow continued expansion from that point on, and that is when I decided to start writing about how Ben Burn-the-Banky's plan was clearly not sustainable, even though all the experts in the financial media seemed to be going right along with him as if this would work. It was not sustainable in the sense that balance-sheet expansion (creating massive amounts of new money through debt issuances) was an effort that would have to be continued forever because any attempt to return to normal monetary policy, as Ben kept telling us we would do, sent the new-money-dependent stock market and economy back toward the pit of the recession. Good ol' Uncle Ben, such a pleasant looking chap, leading us along like children of the Pied Piper to our eventual economic demise.

The core of Uncle Ben's plan, aside from making sure that big banks would become hugely profitable because they were going bust due to having gone for broke, was to rebuild the housing bubble that the former Fed chair, Alan Greenspan, had been the architect of on the basis that its had served the banks and the country well, and it is what was broke. So, clearly the best plan was to rebuild what was broke.

I had never really liked that plan when the first bubble was percolating right along, so I wrote the following to my friend, Stan:

The entire government is failing to learn. If it had learned, it would not be trying to revive the real-estate-driven economy that just crashed. For many decades I have publicly decried the idea that we must always develop more land in order to keep the economy going. I decried it on the basis that it was not sustainable, even though that word was not in circulation so I was not using that word at the time. I simply said that it was obvious we cannot keep a good economy going (sustain it) on the basis of endless development because land is finite....

"Sustainable Economics was part of my thinking before it was vogue"

Not only would space and water run out for endless expansion of the economy by expanding our population through rampant immigration in order to expand our housing developments, but we would simply go right back to hitting the same kind of debt limits that took down the first bubble if the only game in town was to stupidly reinflate the same bubble with the same kind of easy money, loose monetary policy that caused the first bubble to form:

I also argued that clearly the economy could not continue to be based on (be sustained by) the need for housing to rise in value — that sooner or later people would reach the limit of debt they could take out — would hit a natural debt ceiling — and would not be able to go any further.

These things [the nuggets of sustainable economics as a philosophy] I wrote in letters to the editor of various newspapers as far back as my college days. It is something I've believed and preached throughout my adult life.

The Bernanke plan rapidly turned out not to be enough to end the Great Recession, so the economy started to slump toward recession again. In response, Uncle Ben upped the juice. And now we looked like this:

I noted the following problem with the Bernanke Plan back in 2011 when Uncle Ben was turning up the heat on the Fed's pressure cooker to try to get his economic rice to expand:

The government has no ideas for new economies, so they are trying everything to keep the real-estate market propped up to gain more mileage out of that.

Toward the end of 2011, as we were climbing the last part of that new-money slope, I wrote the following:

When “quantitative easing†was first announced, I predicted in newspaper articles at the time it would prop up the economy for awhile and make it appear that we were recovering. I also predicted it would only make the recovery more painful down the road. We are now down the road. We cannot see the end, but we are past the point of no return as for any hope of a soft recovery.

We were past the point of no return because, by now, the Fed had managed to get the economy so strung out on FedMed that it was totally addicted to the new medication. Every time the Fed plateaued the new money, the economy and, often the stock market, started to stall out. It needed routine heavy hits to keep the high going -- a metaphor I often used back then. You can see the plateau in monetary growth after that second rise and see that, once again, every time the Fed allowed the least little taper, it had to immediately prop things right back up because it saw signs of economic faltering.

During that time of faltering, I wrote this:

I stated two years ago (see “Downtime†articles) how long I thought the artificial props would hold before the government would run out of steam and become unable to continue such measures. I stated why quantitative easing (Q.E.) was not sustainable and why it would not create any actual recovery but just an illusion of recovery that would look like a double-dip recession once the Q.E. ran its course. The so-called “recovery†was nothing but a rise in the belly of a Great Recession caused by artificial supports. It would last only as long as the supports lasted.

By "not sustainable" I meant the plan would never get the economy to where its growth would become self-sustaining -- as in not require the constant intervention of "recovery" medicine. Instead of bringing a self-sustaining recovery, any economic recovery brought by this plan would always require greater doses of FedMed to continue, and that was not something the Fed could sustain doing forever because the law of diminishing returns would mean greater amounts were required to get the same results, so the crash would only become bigger the further the Fed went down this road.

I also wrote this back in that October, 2011, article:

I predicted that the government would try a second round of quantitative easing as soon as the first one they approved ended and downward reality began to reappear of a hard road in front of us. I have even stated the government would be strongly tempted to try a third round when the second ended and the ugly reality, again, began to reappear. Anything to avoid this austere reality. Stark realities mean angry voters. Politicians seek by nature to avoid angry voters....

That is the bleak landscape we now face (and are still trying to deny). The artificial recovery made it appear for awhile as if we were just going through another bursting economic bubble and were on our way out. In real fact, ALL of those efforts did nothing to correct the underlying problems of the economy. That is why this is the same recession, not a second recession. It is due to continuation of the same cause. It looks like two recessions or a double-dip only because it was falsely propped up in the middle by the unsustainable effort to create funny money.

The worst part of Ben Bernanke’s solution is that he actually perpetuated the problem and even made it worse.... They also sought to solve the problem of banks that were too big to fail by merging them with other failing banks, creating even larger banks that are all-the-more too big to fail.... Ben Bernanke sought to prop up the failed housing market by expanding debt once again. Yet it was this highly indebted housing economy that led us into this mess. The actions of the U.S. government have been nothing more than a desperate attempt to keep the old economy alive. No one wants to face the arduous task of creating a new economy from the ground up. Nor do they have the vision to know how to do that....

Thus, they can only see to do that which is in their view “tried and true†— meaning only that which has been done before. If the problem is that what was done before worked for awhile but has now reached its logical end, they have no solutions. They failed to see that what was working was not sustainable for the longterm, so they keep trying to sustain it....

What Ben Bernanke did (and is still doing) was nothing more than CPR — breathing hot air into a moribund economy. His solution was not sustainable economically for one simple reason that should have been evident to everyone: the U.S. government (as with many other national governments) was already so deep in debt that it could not continue to transfer all of this bad private debt into the government’s debt for very long. Nor could it risk creating more money by taking out more debt. Most of all, economic growth that was financed by debt everywhere could not be sustained once everyone’s debt capacity was maxed out.

Nevertheless, the Fed and Feds solution to a debt problem was to go exponential on the debt. So, faltering on down the road to toward unsustainability we did go. Thus, after a year and half of still faltering along, the Fed finally did this, adding as much monetary expansion as it had during the first recovery effort and more than it had during the second effort:

That was QE3, which started near the end of 2012. Now we were talking some serious Fed meds.

The trouble of 2012

To back up a bit, 2012, you may remember, was the infamous year when the Mayan's had supposedly predicted the world would end. That, at least, was the general assumption of the worried based on the fact that the Mayan calendar ended in December of that year. (But what were the poor Mayans to do -- create a calendar that stretched for all eternity? Every calendar ends on some year because you run out of paper or rock to print it on.)

Apparently, the Mayans or their interpreters got that wrong. While my predictions for 2012 were also doom and gloom, too, they weren't quite as bad as the end of the world. News at the beginning of the year had been all about the green shoots of spring that were being seen in the economy as proof the Fed's recovery had worked. I wasn't buying any of it.

Economic recovery is the talk of the town. Following a string of job improvements and many other glistening bits of news this week, the economy appears stronger now than at any time during the Great Recession.... The stock market is still roaring along on a growing wave of consumer confidence.... Yet, this whole scene could shatter any given week because it is a house built of sugar glass in a world full of stones....

I think further economic collapse is inevitable for a few very large reasons. The ground that underlies all of the economic indicators mentioned above is faulty, though the indicators are good at present. The foundation of the economy remains a complete shambles. It floats on great chasms of hot air. Nothing has been done to restore the nation’s (or the world’s) economic fundamentals. Therefore, whatever you see on the surface is actually fairly meaningless — a lovely emerging house of glass built on an earthquake fault....

We are now stacking up trillions in debt each year like we used to stack up hundreds of billions with no known way out because we want to put the cost of correction on the backs of a future generation to avoid the pain ourselves. There is no exit plan here.

In fact, I believed, in spite of all those green shoots everyone was talking about, that things would fall apart so badly in the remainder of the year due to the Fed's attempt at another gradual taper, that I said the Fed would have to go back to more QE before the year ended. The Federal Reserve, you see, believed the economy was now doing so well that it actually could taper. I knew, to the contrary, the economy was now so dependent on endless FedMed that the Fed could never taper, so attempting to taper would result in quick disaster. That's why I wrote,

The only end in site for this mess assumes that the economy does recover and that the U.S. continues to pay the cheapest interest rates on the planet for its debt. In other words, the only positive end for this massive debt spiral we are now in depends on a best-case scenario where the U.S. economy revives to such vibrancy that it has a surplus and can start to reverse these massive new debts. Anything less than that, and the U.S. economy gets flushed down the vortex. No one has suggested any clear path to get out of this yawning debt spiral because stopping the debt spending will certainly collapse an economy that is still being entirely founded on debt spending....

I believe in the face of so much trouble Ben Bernanke will strain and manage to pass another round of quantitative easing this summer, but it won’t pass easily this time, as he will find more resistance in the FOMC. It will pass like a wooden block through the bowels of credit only because the alternative looks so much grimmer and because of intense election-year pressure for a short-term laxative. That means it is also likely to be Ben’s last deposit of that kind. Furthermore, this Q.E. will have far less effect than the already ineffectual previous periods when money was given a massive diarrhetic to try to loosen up the nation’s credit. No one will be impressed for long with all the extra cash that comes out of it. In fact, QE3’s failure to accomplish much of anything will increase consumer malaise. While the first rounds of Q.E. brought months of stock-market inflation, this last round may be lucky to bring days of relief.

That is basically how it played out, as you can see by looking at the graph of Fed monetary expansion above.

In another April article I had also written,

The early economic spring of 2012 is going to grind into the dog days of summer for the U.S.... Expect a long, dry and dusty summer economically.... While I cannot predict the behavior of individual people like Ben Bernanke and his cohorts, I strongly suspect there will be another round of quantitative easing in the summer of 2012 to ease the long hot ride with some liquidity.... This is the year when all hope for reviving the old economy begins to crack and fall away....

So, while everyone in the financial world was writing about the green shoots of spring that April, I was writing that the Fed's belief that it could end QE would actually end the Fed's recovery (on the basis that any apparent recovery by the Fed' plan could never become self-sustaining but would require endless expansion of debt to keep feeding it). That is why in the final quarter of 2012, as we steamed toward the Mayan Apocalypse, Gentle Ben and his Federal friends did as I predicted and engaged that massive new round of QE (QE3) to resave the economy they had just finished saving.

Now you might think, if you read through the entirety of those articles, that I sounded more apocalyptic than things turned out. Well, hold on a minute! The only reason we did not fall into total economic collapse after QE2 was that the Fed jumped in with that massive new drug hit to stop the collapse. Think about it: If it took the biggest, most continuous hit ever of Fed drugs to stop the economic collapse, which became known as QE3, how big was the collapse going to be? Apparently, the Fed believed it was going to be massive, because it stepped in with a recovery effort even larger than it had applied in the Great Recession. (Of course, my position was that we were really still fighting the Great Recession because we had done nothing to change the flaws in our economy that led up to it!)

Also think about this: if the Fed's recovery plan was ever going to become sustainable, why did QE now have to become continuous at 80 billion every month?

Janet isn't yellin' "recovery" any more

The Bernanke Fed argued, as did the later Yellen Fed, that it didn't have to be QE forever. It still believed and told us it could eventually taper its QE without killing its recovery. There was a game plan, Bernanke had always maintained, to retrace the balance sheet back down -- to do some quantitative tightening. The Fed had to maintain that point of view because it had always argued that QE was not "monetizing the national debt," which is illegal based on the Fed's charter, on the basis that the Fed was only buying government treasuries as a means of regulating interest rates to stimulate the economy. The treasury purchases, as required by federal law, were not about financing the debt but just a vehicle for accomplishing monetary policy, so once the economy stabilized, the Fed would return its balance sheet to normal.

"We'll taper," promised Uncle Ben.

"We will wrap this up," said Gramma Yellen, tag teaming with Uncle Ben. "We'll actually unwind our balance sheet, and you'll see that doing so will be as boring as watching paint dry."

And, so, they did, and that looked like this:

Like a great, big frown.

A frown, I say, because the economy and the stock market didn't like that much. They went into various stages of apoplectic shock to where the stock market wound up wearing a very similar frown during much of that period, which looked like this:

Not at all a good time for stocks! The bull was broke. He lay on his death bed for two years. You could have exited the market for two years, and got back in at the end of that period right where you jumped out, and missed nothing but the really wild roller coaster in the middle. In fact, much of the NASDAQ became a full-on bear market. Here's what I predicted would happen to stocks during that time.

While the market looks good on the surface, nearly half of Nasdaq Composite stocks are down 20% from a year ago, meaning they are all deeply mired in a bear market. The Nasdaq is made up largely of high-tech stocks, which is where market vulnerability showed up in the last crash of a speculative stock market.... Since the Federal Reserve announced a little over a year ago that it will begin reigning in its quantitative easing program, signs of market vulnerability have risen. The number of high-tech stocks that are in their own bear market has gone up from 30% of the Nasdaq to 47%.

"Bearish Underbelly of Tech Stocks Reveals Increasing Market Vulnerability"

I didn't go as far as predicting a stock market crash in 2014 because, during 2014, the Fed was merely tapering its expansion -- i.e., buying fewer and fewer treasuries -- so it was still expanding but at a rapidly diminishing rate. This, I believed would put the market in peril, but the market could limp through until we got to actual unwinding of the Fed balance sheet (quantitative tightening). Thus, I wrote in September of 2014,

I’m not going to go so far as to say there will be a 2014 stock market crash this fall, but there are some concerning forces building up

The stock market's great crashes, I noted, like to happen in the fall, especially as October surprises.

As you can see in the last graph, the market experienced some immediate and deep trouble right after I wrote that September article in 2014. It had been going up when I published the article, but two weeks later, it experienced its first big 10% correction in a long time, diving into October. In the two years to follow, it would repeat that kind of plunge two more times, going even deeper on the third plunge at the start of 2016. The market clearly was not happy with the new Fed tapering regime.

I was certain enough that the market (and especially the economy) would enter bad times in the fall of 2014 that I bet my blog on it. I actually made that bet that trouble would begin in the fall of 2014 clear back in the spring of that year. I still write the blog because, as you can see, that fall turned into two very bad years for stocks that kept trying to return to the lows of that October.

Accurately, I did not bet on an all-out crash, however, but a period of definite worsening:

I’ll bet this blog when it comes to my Economic Predictions 2014.... If only the forces that can now be seen and felt are the ones at work, then the economy will grow worse but not crash. If something unexpectedly bad — such as war with Iran — bursts into the picture, then the economy could easily crash....

We had three years [2011-2013] in a row that started out positive and upbeat in the spring. The dancers and singers of the new economy all raised their hands and sang of “economic recovery.†I did not. I said those years would get worse, and they did. After a warm spring, the economy cooled off most of the rest of the year. This year, we are off to a dead start with jobs stalling out, but that does not mean the year will be the opposite of past years by starting bad and then turning better. No. If the last few years started out fairly good and then got somewhat bad, this year can only do worse because of the major forces blowing in against it while there is nothing fundamentally fixed in our economy. It is more debt-ridden than ever and floating on a huge stock bubble created by quantitative easing, so more perilous than ever because the Q.E. is now slated to end. That means the artificial life support is coming off in 2014 just as global economic pressures are piling back up.

"Economic Forecast 2014: Strong Headwinds Face Global Economy"

As you can see based on the market graph above, economic and market malaise is exactly what we got in the fall -- two lousy years of it.

Yet, the Fed continued to believe it could actually tighten -- that it could actually reduce its balance sheet -- which it did not start actually doing until 2015 and, even then, very gradually, almost imperceptibly ... until 2018. That, I said, is when the trouble would really begin!

Powell hooked by the jowl

Poor Jerome Powell. He's the guy that got to put in that downward curve of the lip at the end of that frown. That's why he looks like this:

Before he came into office as Fed chair, the market had begun its biggest, steepest rally ever -- the Trump Rally. This had nothing to do with the Fed, but it probably convinced the Fed it actually could take that step forward in its plan to prove to the world once and for all that it really could tighten as Bernanke had always promised it would do, and as Yellen had promised would happen on autopilot because it would be so dull.

The Trump Rally should have given the Fed room to roam. After all, that rally was based on the Trump promise of the most massive corporate tax breaks in history. It began the day he was elected. There was no way such breaks would come if Hillary were elected to continue the work of Obama, but Trump had promised big stuff and was here to deliver. So, the market zoomed the day after election night and hardly looked back ... well, until 2018 when the first year's effects of the tax breaks rolled off the year-over-year comparisons just as serious Fed tightening began. The Trump Trade wars also started seriously eating at many bottom lines, and GDP began to decline almost immediately after the tax cuts so they never paid for themselves as promised. And, so, the federal debt began to grow again because Republicans proved no more capable of conservative spending than Democrats had been once they held all the reins of power

I said the stock market would not likely fall in 2017 when the Fed Great Rewind actually began because the first quarter of the rewind (final quarter of 2017) would begin so small -- at a mere 10-billion a month that it couldn't do much more damage than the incremental decline that had already begun. In fact, I though the market would breath a sigh of relief that the rewind had finally begun and nothing happened, so it would likely go up; and, so it did, marking its steepest rise in the Trump Rally.

Then came 2018 when Powell began his term as Fed chairman.

The market's first downturn, I said back in 2017, would come in January of 2018 when the Fed doubled down on its rate of rewind. Tightening jumped from 10-billion a month to 20-billion, and immediately fear struck the market as I said it would because the market would start to see this was real and would feel the squeeze. The spring step up to 30-billion a month, I said, would not feel like much change, but the summer step to 40-billion, doubling what happened in January would make itself felt with new market troubles. However, the fall would be when all hell would break lose as the Great Rewind hit full speed at the end of September, sucking 50-billion a month out of the financial system -- 5/8 the speed of QE. That would be enough downdraft to get serious.

The stock market seriously hated that program throughout 2018, and that looked like this:

The stock market experienced its largest Dow plunge beginning in January of any year since the Great Depression. During the spring, it experienced a few minor hiccups, but nothing of note. Then, in the summer it fell a little harder, but what was of great note in the summer was that the FAANG stocks, long the market's indomitable leaders, broke badly and crashed anywhere from 30-45% in their own bear markets.

Finally, came the fall. Powell announced the Fed was hitting full rewind and would put that on autopilot for a period of maybe a couple of years to finally unwind its balance sheet. As soon as Powell made the announcement, the market started to plunge, and by the end of December, it had put in its first serious down year since the Fed's Great Recovery program had begun. (2015 was marginally a down year for the Dow and S&P, but not the NASDAQ) due to the start of tapering its bond purchases but not actually unwinding its balance sheet.) So much for the Fed ever actually reducing its balance sheet.

The plan was a disaster, and the market only stopped falling because Powell chose to lose face by announcing prematurely (by about two years) that the Fed was backing down from the Bernanke and Yellen promises much sooner than Powell had originally stated, starting with the Fed's interest-rate increases. The market stopped falling shortly after Powell made his face plant.

Here was Powell's December 19, 2018, announcement, which tried, of course, to put as good a face on things as he could muster:

Since the September meeting of the FOMC, however, some crosscurrents have emerged. I’ll explain how my colleagues and I are incorporating those crosscurrents into our judgments about the outlook and the appropriate course of policy.... we have seen developments that may signal some softening relative to what we were expecting a few months ago. Growth in other economies around the world has moderated somewhat over the course of 2018, albeit to still-solid levels. At the same time, financial market volatility has increased over the past couple of months, and overall financial conditions have tightened—that is, they have become less supportive of growth.... The projections also show a modestly lower path for the federal funds rate, which should support the economy and keep us near our goals.... Many FOMC participants had expected that economic conditions would likely call for about three more rate increases in 2019. We have brought that down a bit.... What kind of year will 2019 be? We know that the economy may not be as kind to our forecasts next year as it was this year. History attests that unforeseen events as the year unfolds may buffet the economy and call for more than a slight change from the policy projections released today.... The additional tightening of financial conditions we have seen over the past couple of months along with signs of somewhat weaker growth abroad have also led us to mark down growth and inflation projections a bit.... Over the next year, if events play out broadly as expected, the federal funds rate will be in a range in which judgments of people both inside and outside the Fed will sometimes differ regarding whether the stance of policy is modestly accommodative, neutral, or modestly restrictive....

"Transcript of Chairman Powell’s Press Conference December 19, 2018"

And who was it that was doing all that tightening ... intentionally? Powell, in his initial statement, did his best, of course, to put a good face on all the Fed had done and on how the economy was doing, but the US stock market focused on his words that hinted at a premature slowdown in Fed tightening with possible additional slowing of the tightening regime. It wasn't quite all the oxygen the market needed, as tightening was continuing, but Powell's words did contain a hint that autopilot was going off:

Moving forward, my colleagues and I will be watching the economy closely for indications that the stance of policy is appropriate to sustain the expansion.... Neither the pace nor the ultimate destination of any further rate increases is predetermined. We will adjust monetary policy as best we can to keep the expansion on track....

Still, the market did not get all the news it wanted. In fact, in the questions afterward, Powell was asked,

I’m wondering if the Fed has had any discussion of altering the course of balance sheet normalization and if you could give us any insight on what might lead the FOMC to alter that balance sheet normalization in 2019.

Powell answered as follows:

If you go back some years, I think we—people who were working at the Fed in 2013 and ’14 took away the lesson that the markets could be very sensitive to news about the size of the balance sheet, the pace of asset purchases, the pace of runoff, and things like that. So we thought carefully about this, on how to normalize policy, and came to the view that we would effectively have the balance sheet runoff on automatic pilot and use monetary policy, rate policy, to adjust to incoming data.

And I think that has been a good decision. I think that the runoff of the balance sheet has been smooth [really?] and has served its purpose. And I don’t see us changing that. And I do think that we will continue to use monetary policy, which is to say rate policy, as the active tool of monetary policy.... I think we’ve reached the bottom end of the range of Committee estimates of what might be neutral. I think, from this point forward, we’re going to be letting the data speak to us and form the outlook and inform our understanding of what would be appropriate policy. So there’s a fairly high degree of uncertainty about both the path and the ultimate destination of any further increases.... So we also took down our rate forecast.

The Fed failed

So much for autopilot and boring as watching paint dry. The Fed's focus, however, was on interest-rate policy, but backing off from that is a move away from quantitative tightening, too. Only three months into full-speed tightening, and the Fed decided it had already tightened to the new normal:

Policy at this point does not need to be accommodative. It can move to neutral. It seems appropriate that it be neutral. We’re now at the bottom end of the range of estimates of neutral. So that’s the basis upon which we made the decision. I also think we took on board, you know, the risks to that, and, you know, we’re certainly cognizant of them.

The announcement that the Fed may have already hit the neutral level for interest rates meant all tightening could end. Bear in mind, Powell was doing all he could to avoid losing face as much as he could and to not mention the stock market directly or the end of tightening, lest the Fed be seen as a slave to the market. Powell was certainly not going to claim outright that tightening was ending because it had failed. So, he spoke more broadly of "financial markets tightening," as if they had been doing that on their own, but everyone knew the financial market taking the biggest hit was the US stock market, and everyone knew who was causing all the tightening.

The stock market continued to fall for three more trading days after Powell's big speech, taking its biggest point-drop in history on Christmas Eve because Treasury Secretary Steven Munchkin terrified the market with a glib (and possibly drunken?) announcement from his vacation swimming pool that he had just called all the major US banks to make sure they had enough money left in them to withstand any runs on the banks.

CNN summarized the year for stocks as follows:

2018 will be remembered for its extreme volatility. The VIX volatility index spiked, and CNN Business’ Fear & Greed Index has been stuck in “Extreme Fear†throughout much of the year. The Dow has swung 1,000 points in a single session only eight times in its history, and five of those took place in 2018.... The FTSE All-World index, which tracks thousands of stocks across a range of markets, plummeted 12% this year. It’s the index’s worst performance since the global financial crisis.

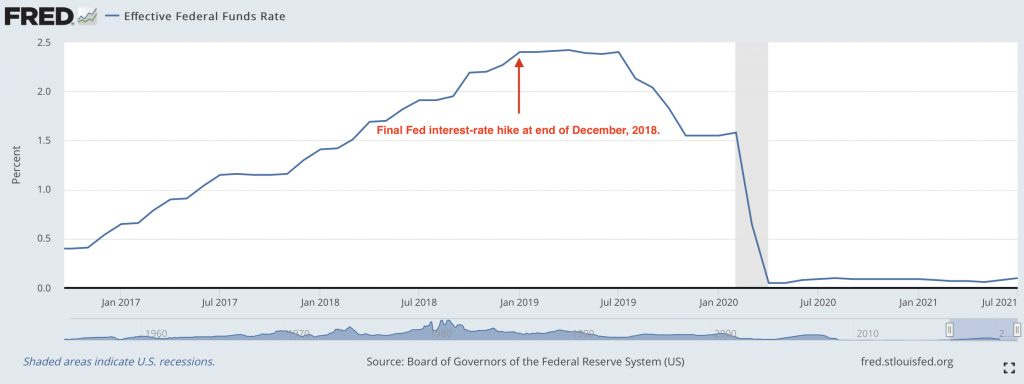

CNBC called it the "worst year in a decade." They also noted "the Fed finished its last rate-hiking cycle in December 2018" because, regardless of what Powell said about a few more to come, that is where rate hikes actually ended:

As you can see, from the end of December, rates fell, and they haven't dared go back up since.

The Dow, S&P and the lofty NASDAQ all experienced their worst crash since the start of the Great Recession as a result of this curtailed program of attempted normalization. So much for the Fed's ability to tighten without ending its Great Recession Recovery.

Why did the Dow leap back up a over a thousand points on December 26 -- its most massive point gain ever? No one really knows. Nothing special seemed to have happened on that particular day. Perhaps it was a recovery shock from realization on the first trading day after the Munchkin's astounding announcement that banks hadn't crashed. Perhaps it was that the market rightly sussed out over the few days after Powell's announcement that this was more of a face plant than Powell made it sound and that rate hikes were, in fact, over (as they, in fact, turned out to be). I think a solid point can be made that there was enough in his words to see the end of interest rate increases had come in sight and that the end of balance-sheet reduction couldn't be far off either with the Fed making such a turn, and that brought some calm.

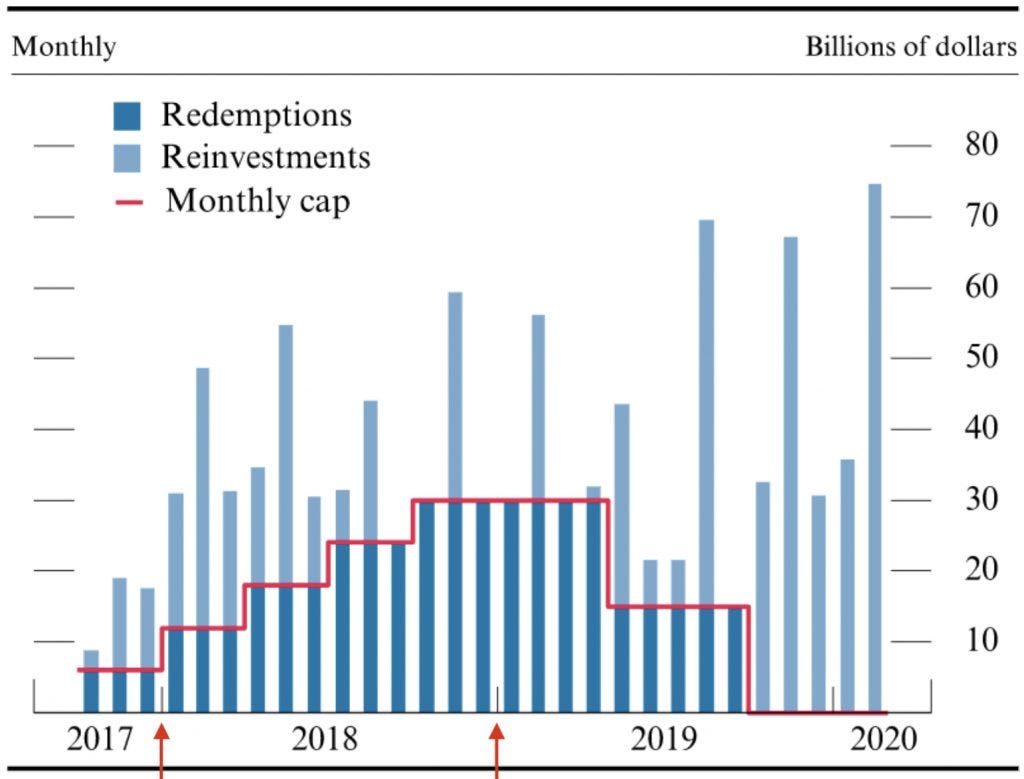

The Fed was caving in, and it would soon cave all the way. In March, Powell and his federation of banksters finally retreated on the balance-sheet runoff, too, cutting the rate of reduction way down and announcing its early termination. Taking the first step down from its rate of balance-sheet reduction in May, the FOMC also wound up terminating the program entirely two months earlier than they had promised in that March announcement, deciding at the end of July to bring it to an immediate end, rather than at the end of September of 2019, the date they had revised to in March.

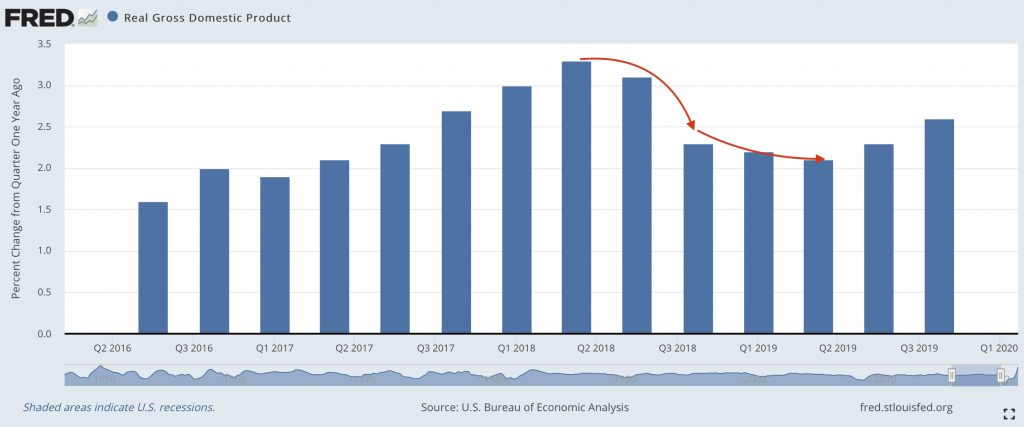

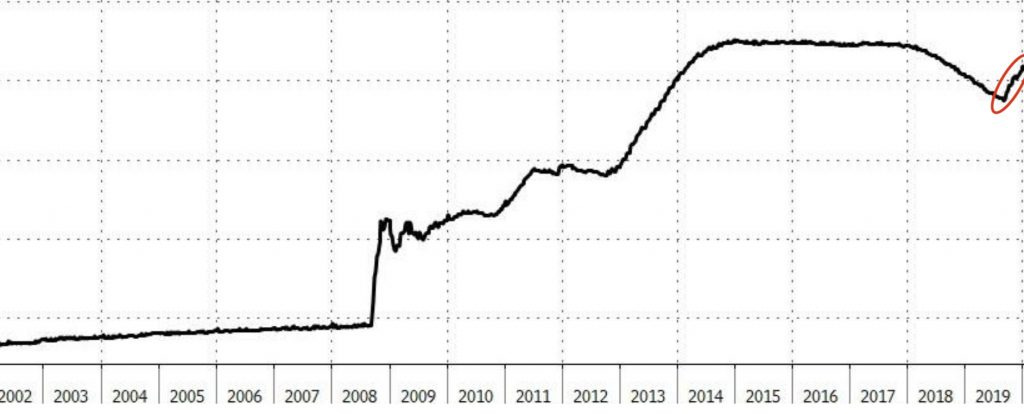

In the following graph of the Fed's tightening program (issued by the Fed before July's revision of the timeline), you can see how the Fed ramped up its tightening throughout 2018 (the period delineated by the red arrows) and then, right after its March meeting, came down to nothing in two massive steps very quickly in 2019, far short of the prolonged period of tightening that the Fed had originally promised would prove so boring (and even earlier than shown in this graph):

The sudden change shows they clearly saw trouble. Both steps down in 2019 happened earlier than anything Powell had hinted at in his December face plant because other troubles were building in the economy. While 2018 was a dismal year for stocks, it was not such a good one for the economy either. As you can see in the following graph, economic growth also did somewhat of a face plant during the Fed's Great Rewind:

While the economy stopped falling as the Fed rapidly backed away from its tightening regime, other problems emerged because even the much foreshortened tightening schedule continued on longer than banks could bear. My big prediction for 2019 was that Fed tightening would end in a massive repo crisis in the latter half of 2019 because bank reserves were being drawn down too far due to the Fed's reluctance to give up tightening soon enough. That would only end, I said, by the Fed going back to QE to actually reverse its tightening, and we all remember how that went as it is not that far back to remember. As CNBC recapped just last week,

Getting rates back to normal didn’t end well for the Fed the last time it attempted to do so from 2015-18, as it had to stop in mid-cycle amid a slumping economy. Hence, markets could be excused for being at least a little nervous this time around. The Fed not only has to turn around its most-aggressive easing policies ever, it must do so with precision and hopes that it doesn’t break anything in the process.

Good luck with that. At the end of the Fed's big frown, the Fed had to rush back into QE during the final quarter of 2019, though, of course, Powell maintained that it wasn't really QE because, again it was just temporary and did not involve long-term bonds. (Any excuse will do to avoid saying they have permanently monetized the US debt and its economy.) That looked like this:

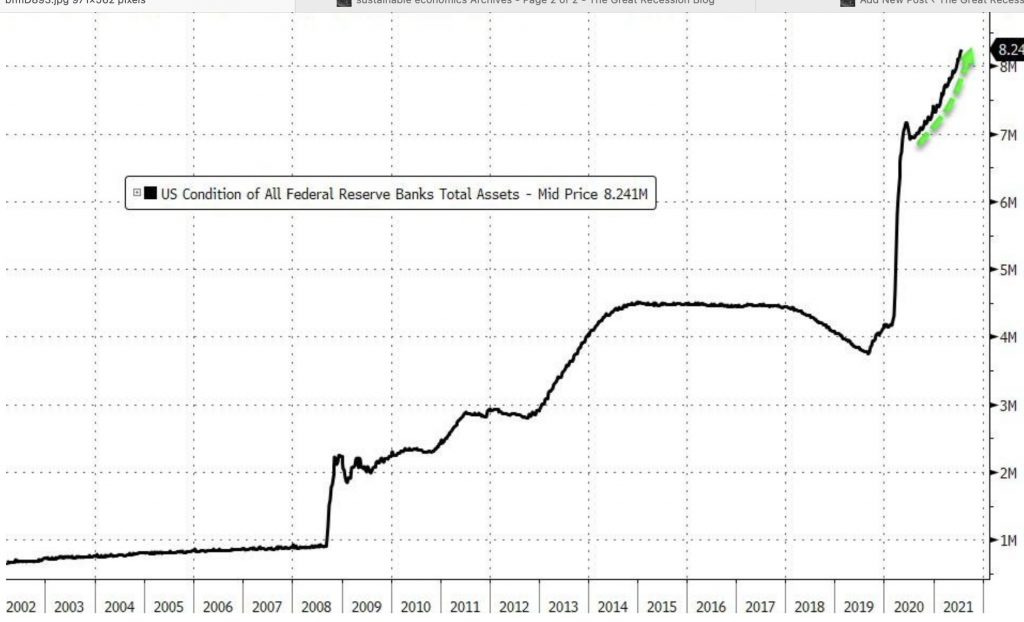

Then came COVID and our chosen economic shutdowns, which gave the Fed cover to return to QE that was QE, no holds barred, including purchases of bonds across the full maturity spectrum:

The Repo Crisis only ended when we moved to more QE than the world had ever seen -- almost as much QE, in fact, as all the previous rounds of QE that had gone on before. (That's that law of diminishing returns I talked about at the beginning of all of this.) Well, "almost" until that became this:

And suddenly, that burst of QE that began it all when the Fed's recovery plan for the Great Recession began way back in 2008 looked like a tiny, tiny little bit. The new QE, QE4ever, has already managed to outdo all the previous rounds of QE put together. So, as I said back at the start of tired and endless recovery plan, once we began down the path of QE as a way out of recession, instead of rectifying the real problems that were the cause of the Great Recession, it became QE forever, Baby! We decided to solve a debt problem by piling on more debt in that all Fed money issuance happens through debt issuances.

And that's why I call this the Great Recession Blog. We're still on the Great Recession Recovery Plan with no end in sight because we solved nothing! We just bought time -- "kicked the can down the road" --at the cost of ever spiraling debt, financed by exponentially growing Fed money printing. And we all know what happens now if the money printing actually stops. This time, however, the Fed has inflation breathing like a dragon down its back to face it to stop moneh printing, and this time the Fed faces that tightening pressure when the economy is already slumping:

Fed officials themselves expect noticeably slower growth in the years ahead at a time when both monetary and fiscal policy will be tighter. That raises more questions about whether Powell and his cohorts can get the exit right. “Are they exiting at the right place? Are they exiting at the right time, at the right magnitude? Given the slowing of the economy, we have questions around both,†Misra said.... "I think people are very worried about the idea that maybe this isn’t going to work out the way we planned."

It never has. Why would it start to now?