The Global Economic Tide is Quickly Receding

The global economy is now stranded as the central-bank tide runs out. By the end of this year, the collective monetary inflow from all the central banks of the world, which rose to a high-water mark of $2-trillion per year, will have ebbed to zero. After that, it runs net negative for years to come.

One can sense the effects of this tidal change in how we have moved from enthusiastic talk of "synchronized global growth" at the start of the year to clear realization everywhere that such growth ended as quickly as it began. January turned out to be peak high tide on all the shores of the world.

To get a sense of the collective central-bank action for this year, Fasanara Capital published the following chart last year of the quantitative tightening planned for 2018:

As we are almost halfway through 2018, we are nearly past the days when the monetary inflation of one central bank could compensate for the tightening of another, supplying new money to invest in markets anywhere. While a net positive trickle of new money will continue to come in from some nations, that, too, shall end by the end of this year (unless economic catastrophe shifts the plans of central banksters into rapid reverse).

A sea change in the flow of money can me unmistakably felt.

Taking stock of stocks

It can also be felt in the rapidly deteriorating beliefs of stock investors. According to Bank of America, the number of stock investors who believe the economy will be doing well twelve months from now has reached a low that was last seen in February of 2016, which is the last time the stock market took a shock drop. The number of investors who now believe the economy will be fine a year from now? One percent! That is an abrupt decline in investor sentiment from the start of 2018 when 40% of investors believed in the continuing strength of the economy.

Fast forward a few months, and investors now are facing headlines about tariffs and sanctions, escalating Middle East tensions, equity market volatility, concerns over interest rates rising too quickly (after being subdued for years), and a few economic report disappointments. These developments seemingly have dampened the optimistic global growth outlook. (MarketWatch)

Back then, growth projections for first-quarter US GDP were around 4% annualized. Real growth came in at 2.3%, almost a third weaker than the average for the three previous quarters. My statements a year ago that it would be abundantly obvious by this summer that the global economy was failing -- and stocks with it -- are borne out:

For almost a decade, it’s been extremely difficult to lose money in the U.S. stock market. Over the next decade, it could be hard to do anything but, according to analysts at Morgan Stanley. The outlook for market returns has precipitously worsened in recent months, with analysts and investors growing increasingly confident that the lengthy bull market that began in the wake of the financial crisis could be, if not coming to a close, petering out. (MarketWatch)

Morgan Stanley noted in a report titled "The End of Easy" that the market's days of predictably soaring upward over the past several years are finally over ... and for the reason I said this would happen:

Decelerating growth, rising inflation and tightening policy leave us with below-consensus 12-month return forecasts for most risk assets. After nine years of markets outperforming the real economy, we think the opposite now applies as [central bank] policy tightens.

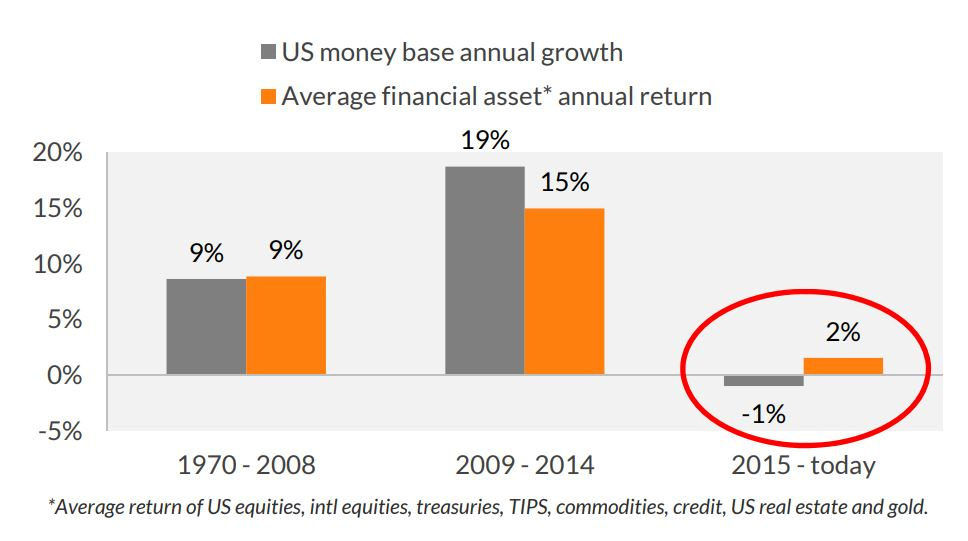

If you are one of the few who still think the rise in all asset values combined was not related to the rise in money supply, here's a helpful clue:

As the money tide has turned from pre-Great-Recession to Great-Recession recovery days and now to the post-recovery days of monetary tightening, so has gone the value of assets. With US quantitative tightening having only seriously begun this year, we see the stock market has moved from rising euphorically to trading in a tight range for months that is mostly downward. As tightening increases in all nations, everything will move into recession. Central banks appear to be oblivious to this basic math: what goes up must come down when the force that drove it up reverses. It is, apparently, too simple for a central banker to grasp as their heads swim in complexities of their own creation.

The S&P and Dow have remained in correction territory for months since they plunged right on schedule at the end of January. Bulls who thought last week's 2.4% rise in the S&P was the returning tide were disappointed this week when it returned, instead, to falling., taking its biggest drop since the beginning of April. It's become hard for investors to say whether each dip is an opportunity to buy or each rise is a bull trap.

The biggest concern noted by 30% of investors in the BofA survey is that central banks will overstep. (Of course they will. When have they not?)

Barry Bannister, head of institutional equity strategy at Stifel, said a snafu by the Fed—such as it becoming too hawkish—could spark an “unusually rapid†bear market, as well as a “lost decade for stocks.â€

For the fourth month in a row, investors have moved allocations in their portfolios from stocks to bonds. Unless you're good at trading the ups and downs, the major stock indices have made no money in 2018 (outside of dividends). Even though emerging markets -- stocks and local currency bonds -- are tanking, money is not fleeing sufficiently from emerging markets into the US market to pump US stocks up. The Dow remains down 2,000 p0ints from its last peak.

Most likely, money is moving into US bonds because of rising interest rates. That's good for those looking to buy and hold bonds, not so good for those with old bonds they want or need to sell. The iShares J.P. Morgan EM Local Government-Bond ETF, for example, had net outflows totaling $560 million this month. Financial flows out of bond funds at that speed eventually force those funds to sell bonds into a falling market, increasing downward momentum.

While euro stocks have been on a four-month rise, trying vigorously to recover lost ground, they still remain below their January peak.

Carmageddon keeps building

Following up on my last Carmageddon article, used-car sales took their biggest drop last week since 2009, supporting my statements about the path to come. Meanwhile, the number of delinquent sub-prime auto loans surpassed Great Recession highs by rising to the highest level in more than twenty years.

And this is before we have entered an official recession. This decline redeveloped, in fact, during that goldilocks time of "global harmonious recovery" the media and their pet economists were prattling about at the start of the year. (Foolish talk that you'd never hear here.) That's astounding when you think about it -- to beat the record for delinquencies from the worst of years during the best of years! Don't know how you do that! But let's call it "global harmonious price discovery" for lack of a better term. People are discovering the hard way that cars cost more than they can afford (even when employment is purportedly also at a peak level)

Bondage breaks loose

As predicted, here, the 10-year UST bond has broken solidly past the 3% barrier, pegging 3.11% this week, its highest level since the end of the Great Recession. The 30-year bond made its greatest one-day rise this week since February, hitting 3.25%.

Unlike many writers, I don't think the yield curve has to flatten before we go into recession this time because this time is different. This time, the Fed is unwinding trillions of dollars of long-term bonds. That is bound to spread the yield curve, making it a less effective barometer this time around of where people believe the economy is headed and more indicative of bond supply being forced into the market. (And that difference will fool lots of people who expect old patterns to always happen the same way. It is not that the indicative value is gone; it is that extraordinary forces are pushing the spread apart.)

The retail apocalypse keeps advancing

Chapter-11 bankruptcies have spiked 63%, reaching their highest level since April 2011 near the official end of the Great Recession. (Again with comparisons that always seem to line up now with the Great Recession. These bankruptcy numbers include all sectors, not just retail.)

Here's how things get worse. Remember how banks had to curtail foreclosures during the housing collapse because the very act of foreclosing was bringing down the value of other homes in neighborhoods so quickly that the banks' collateral was evaporating due to the downward spiral their own foreclosures were creating? Well, the same thing is happening now in retail bankruptcies, and it's happening once again with those dastardly mortgage-backed securities that practically ended the civilized world as we knew it back in the Great Recession.

Example: When Toys "R" Us issued commercial mortgage-backed securities before its bankruptcy, it estimated the securities were 98.3% collateralized and that, by the time the funding was all repaid, the securities would still still have a loan-to-value ratio of 91.4% under the company's worst-case scenario.

In October 2016, about 11 months before it filed for bankruptcy and 17 months before it decided to liquidate its operations in the US, Toys “R†Us sold $512 million in commercial mortgage-backed securities, backed by 123 Toys “R†Us and Babies “R†Us stores

Now the worst-case scenario has gotten a lot worse. Deutsche Bank analysts Ed Reardon and Simon Mui wrote in a note Wednesday, cited by Bloomberg, that as many as 26 of the 123 properties backing this deal may have little or no value if they’re vacated by Toys “R†Us. (Wolf Street)

Deutsche now estimates the value of the collateral backing those Toys "R" Us securities has collapsed by 34%. You see, with other brick-and-mortar retailers also failing, its hard to find tenants to fill the unoccupied Toys "R"Us stores. And, so, the death spiral begins again, starting in commercial real estate this time.

Once-growing commercial real-estate prices have already fallen backward by two years. Yet, the number of loans secured by this real estate is 11% higher than it was at the last real-estate peak ... just pre-implosion. (Again with things matching up only to that last time of economic crisis.) Banks that have specialized in issuing commercial real-estate loans are moving into a perilous position as their collateral value evaporates. Commercial real-estate (CRE) prices collapsed 40% during the last crisis.

When prices start to turn down, the market can collapse rapidly because of the downward spiral created in collateral values and because of how leveraged things are and how banks bundle these properties into their own mortgage-backed securities. We are now just rounding the peak in CRE.

Shown another way:

Average prices would be falling much faster if we looked only at retail space, but the above stats include industrial commercial real estate as well, which is still rising and, thus, helping hold overall statistics a little for the time being against an otherwise rapidly receding tide. All other sectors -- lodging, multi-family apartments, office and especially retail, are either flat or falling.

As CRE is starting to cascade down, US homes are peaking out, becoming more expensive than they've ever been just as mortgage rates are on the rise. That is triggering (for this summer only) a last-minute rush to buy a home before prices and interest take them forever out of reach, but that will all collapse in the fall when the usual summer buying period ends and interest finally has risen enough to make sure no buying spree returns for years to come. We are now in the last hurrah for the housing market and will be for most of the summer. (This, too, matches the elongated timing I gave last year for the housing-market collapse. More on that in an upcoming article.)

Once again, the closest comparison for the present situation is found in the Great Recession.

How about them tax cuts?

With most of the corporate tax benefits that became law this year already going toward dividends and a huge ramp-up in corporate stock buybacks, just remember that buybacks and dividends don't create jobs. They only create rising stock prices, and so far they are failing completely at even that. As I said over a year ago, if Trump & Co. really wanted to create rising wages and more jobs, they would have put a prohibition in the new corporate tax laws to keep those who opt to benefit from the the lowered rates from engaging in stock buybacks. Those who want to continue in buybacks could opt out the lowered rates and do their buybacks, instead.

If that sounds like government manipulating business, just consider that it used to be that all stock buybacks were illegal all the time -- a basic principle we should return to so that CEOs and big corporate board members don't simply use their positions to milk a company dry for their own personal gain, but instead invest in real future growth. If Trump and Republicans really wanted the tax changes to benefit the economy and really cared a whit about the middle class, they would have written that limitation back into the law to make certain the tax benefits drove the economy and didn't just get endlessly recycled in the stock market to help the rich and widen the gap between the one percent and all the rest. But that wouldn't have served their rich cronies ... or themselves, would it?

So, here we are, being sucked by the tide back into the last economic collapse. Now we'll find out what the real bottom looks like. I'm sure it looks mostly like sludge, a few sunken tires, some broken bottles and a barnacle-covered child's trike. Whatever it is, we soon get to see the true bottom of the Great Recession.

[amazon_image id="9870563457" link="true" target="_blank" size="medium" ]The Modern Survival Manual: Surviving the Economic Collapse[/amazon_image][amazon_image id="B06Y2K9MN6" link="true" target="_blank" size="medium" ]The Economic Collapse Chronicles Three-Book Box Set: A Post-Apocalyptic Novel of America's Coming Financial Downfall[/amazon_image][amazon_image id="B00M5IW4FE" link="true" target="_blank" size="medium" ]Surviving in Trying Times: A story of economic collapse.[/amazon_image][amazon_image id="0987924125" link="true" target="_blank" size="medium" ]The Money GPS: Global Economic Collapse[/amazon_image][amazon_image id="1492373990" link="true" target="_blank" size="medium" ]American Exit Strategy (The Economic Collapse Chronicles) (Volume 1)[/amazon_image]