Hopium Floats, and That's How the Market got High on Friday

So much for the trade war being "good and easy to win." Let's be honest. Trump has been grinding away on it for almost a year now, and China has barely flinched in its negotiations. On Friday the tariff war became personal because it will now tap your own budget and every business budget in town.

If you think Trump's boosting of the amperage means China will settle quickly, you may be one of the people I talked about in my last article, "The Zombie Epocalypse: A River of Denial Floods Markets Everywhere." Since you are a reader here, however, that is unlikely. In which case, this article is not to restore you sanity but to help you maintain it in an environment where you are surrounded by opiated fools.

To my own surprise, it turned out my last article understated how lulled in denial market madness has become, for Friday yielded a revelation that the Zombie Epocalypse has infected the entire earth when stocks everywhere rose euphorically upon receiving news that the tariff war is fully engaged!

While the US market started off in week-long depression, it ultimately lifted to where the Dow posted its first gain in an otherwise miserable week (+114), though the S&P and Nasdaq barely lifted their heads from their stupor to look around. Bull and bear alike, however, had expected the market to plunge if Trump and Xi failed to find a meeting of the minds, but it didn't.

Mind you, Friday's delirium may prove to be transitory. Reality could set in on Monday. At first, people are scared and the market tumbles, as it did at the open; then they see that it isn't tumbling as badly as they feared, so their drug-addled brains return readily to their former euphoria; and, so, the weekend party begins. However, the hangover and indigestion from the party bombards them all day Monday as they start to think more soberly.

Until we see how Monday goes, we have a market that went from Mayhem to madness on Friday. It fell in May in anticipation of larger tariffs and then rose when they arrived on the hope that they really didn't. I'll tell you why that is madness, starting with a layout of the new impacts of the fully engaged tariff war, followed by the reasons that were most commonly given to explain or justify the market's optimism on Friday, and end with a clear presentation of why those reasons are all a boatload of baloney.

The real impacts of Trump's tariff war

Let me start by saying, I'm not against fighting China with tariffs, though there was a smarter way to go about this. Cheater China needs to be fought, but let's not be stupid about the real costs to the US, and let's remember that soberly that American protectionism helped make the Great Depression what it was.

Contrary to the baloney Trump is blowing out his horn about China paying all of this into America's coffers, the move to phase two in the tariff wars, which escalates tariffs from 10% to 25% on $200 billion worth of goods imported from China is a tax that falls on American importers, businesses and ultimately consumers.

To some extent, Trump has been right about China paying so far. That's only because, to some extent, American businesses managed to put the 10% phase-one tax back on Chinese businesses by getting some to lower their prices to offset some of the tax. However, American businesses still had to absorbed as much as they could in order to avoid passing any of the tariffs on to consumers. They didn't want to pass them along because that would result in declining sales, which could turn into declining market share, which in some cases means a permanent loss of loyalty toward a customer's preferred brands. So, businesses on both sides of the Pacific have sucked up the 10% tax, hoping it would be short-term so they could endure their new very thin margins.

That now changes. Businesses claim to have absorbed as much of the tariffs as they can; so, more than doubling the 10% tariffs, places businesses where they won't be able to absorb the increase. As a result, the 15-point increase is almost certain to pass entirely along as a tax to you, the consumer. (And there flies out the window whatever tiny stimulus the US may have derived from the miniscule tax cut that was dribbled out to the middle class.)

Let's talk for a moment about the real-life drain that places on the US economy, which is certain to extend to the global economy to some extent. That applies especially, of course, to the already pekid Peking economy, which has been vital to the world in helping lift it some through the Great Recession. It won't be lifting it any longer.

The third phase of new 25% tariffs on an additional $325 billion worth of imported Chinese goods -- still just being talked about -- will mean essentially all Chinese goods will be taxed at 25%. Trump threatens that will kick in one month from now if China has not reached a deal with the US.

The consumer's alternative to all these new tariffs will be to shift toward non-Chinese brands that used to be more expensive but now compete favorably. That would be good in part for the US if it meant shifting toward American brands, but it doesn't because many American brands are loaded with Chinese parts or resources, so they will also go up in price. And, let's face it, a huge amount of the items that flood your Walmart shelves with a cornucopia of delectably cheap diversions, entertainments, must-haves and needful things come from China. Moreover, any non-Chinese brand you switch to will still be more expensive than what you were paying, or you wouldn't have gone with the Chinese brand in the first place. It's not like buying "Made in China" was ever a quality choice.

The American consumer is already deeper in debt than he or she was when the Great Recession began, and credit defaults have doubled over the last couple of years as the Fed raised interest rates on all of that debt and tightened money supply. Houses are more expensive in many areas than they were at the start of the Great Recession, though that is starting to reverse in some areas as sales have been declining for nearly a year now. Prices on consumer goods are, of course about 30% higher overall than they were when the Great Recession began, while wages over that same time have risen about half that much.

Here are some estimates being given of the real costs of these tariffs:

The second phase of tariffs that has just gone into effect on goods that originally had a 10% tariff applied to them could cost America an estimated 900,000 jobs and cost the average family an estimated $767 a year. By the end of 2019, these tariffs will have cost the US economy an estimated $29 billion and cost the global economy $105. Not too hard to absorb, but not something that should make the stock markets of the world all rise either. (Some estimate a loss of $62 billion by the end of the year by guesstimating Chinese retaliation.)

After that, it gets serious. If the (third phase) 25% tariffs kick in a month from now on the additional $325 billion in Chinese goods, the estimated job losses clock in at whopping 2.1 million additional jobless people. That strips away all the jobs added in the last two years; but it is actually worse than just setting the job clock back to the Obama years because population has grown by that same amount during those two years, so the available labor force has grown by about 1.5 million during that time. Meaning going back to the number of jobs we had at the end of the Obama years means a lot more people wanting jobs than we had wanting jobs at the end of the Obama years. At the same time estimated costs per household will go up by around $2,200 a year -- not devastating, unless you are one of the newly unemployed, but a drain that will certainly trickle down in America's consumer economy.

(Note: the study giving these figures was put out by the Trade Partnership Worldwide, a group that has every incentive to make things sound as bad as possible. These worst-case numbers include an estimation of the impacts of China's own retaliatory tariffs. Another group, the London-based Centre for Economic Policy Research, wrote in March that the cost of phase-one tariffs to the American economy last year was $6.9 billion (reaching $1.4 billion per month by year's end) in addition to the costs paid by American consumers and importers -- i.e., the unseen costs in addition to the seen costs.)

Some estimate the US economic loss with Chinese retaliation factored in under this third phase would be as high as $100 billion a year. Oxford Economics, on the other hand, puts the job losses under either scenario substantially lower at about 200,000 jobs (phase two) and 360,000 jobs (phase three).

Even if you go by the most relaxed numbers, think of the difference to the stock market if we go from seeing an increase each month of around 220,000 jobs simply to a small loss of 15,000-30,000 jobs a month! That's a big dent in investor psyche. (After all, we are not talking about a decline in the rate of growth, we're talking about a move month-after-month into negative numbers like we saw in the early years of the Great Recession.)

In a scenario where Washington puts tariffs of 25% on all imports from China, with Beijing retaliating in kind, U.S. GDP would take a hit of around 0.5% ... leaving the economy around $45 billion smaller by 2020 than in a world without tariffs. That would push real GDP growth — growth minus inflation — dangerously close to 1% by the end of 2020.... China’s GDP growth would be reduced by around 1.3% in 2020, slowing to an unprecedented 5% annual pace, while world GDP would suffer a significant 0.5% loss (see chart below).

That's just the immediate impact, though. What is the knock-on effect as the waves that slam against foreign shores reflect back onto our own when those countries flagging economies result in them buying fewer American products? What's the knock-on effect of so much unemployment when it also reduces what people have to spend so that higher taxes (tariffs) aren't the only thing slowing the economy? What's the knock-on effect to government revenue in a time of burgeoning deficits? And, from there, the effect on government interest (and thereby everyone's interest on everything) as the government increases borrowing?

The hope, of course, is that it all goes away before it begins.

Why the market did a Hail Mary, Hallelujah!

The market threw a last-minute scoring pass into the end zone on Friday because investors suddenly realized talks would continue through Friday. That supposedly secured hope through the end of the day that all of this might go away in a harmonious agreement. Ooops. It didn't. Perhaps, investor's hoped, it is all just negotiation bluster that will pass in the evening sun. Oops. It wasn't, but the market closed before negotiations did. So, we'll see if Monday restores some sobriety regarding those high hopes.

David Stockman calls this hopium. The market rises on any whisper hope, regardless of whether it has any firm basis. It rises because people are determined the game will go, the roulette wheel will continue to spin, the pretty lights will keep flashing, and the clamor of the crowd will grow into a roar because everyone wants it to. Reality becomes the sideshow to the sideshow.

“Investors seemingly continue to try to cling to hope that policymakers on both sides opt to deescalate,†Deutsche Bank’s research strategist Jim Reid said in a note Friday.

Oops. They didn't. No one knows when such baseless hope will stop working because no one is responding to anything real anyway. The downside is that, the farther you go up that astral road, the bigger and more surprising the fall when reality finally intrudes beyond people's ability to mask it; i.e., when it rises beyond their ability to deceive themselves. (Perhaps there is a limit to that.)

Here are the hopes that were widely claimed as being the reasons the market rose:

Stocks rose because President Trump said he had received a "beautiful letter" from Chinese President Xi Jinping.

Stocks also rose when Treasury Secretary Stephan Mnuchin said that trade talks were constructive.

Stocks rose when Trump tweeted that tariffs could be removed and that talks will continue

The market rose when Goldman Sachs noted that the escalated tariffs only begin on items that ship from China after Friday's deadline and arrive in the US two weeks now. That buys two weeks before tariffs will actually start being applied, during which time Goldman posited a deal might be struck.

Finally, some analysts said the market had already priced in the tariff hike.

Goldman Sachs told clients in a note that there is still some wiggle room in the negotiations.... “We note that details in the notice implementing the tariff hike indicate that exports that have already left Chinese ports before May 10 will not be subject to the increase,†said Goldman economist Jan Hatzius. “This creates an unofficial window, potentially lasting a couple of weeks, in which negotiations can continue and generates a ‘soft’ deadline to reach a deal … This also leaves an opportunity for the two sides to reach an agreement in the next couple of weeks...."

Any hope, I guess, will do in a storm if the market is going to rise just because it is supposed to.

If hopium floats your boat, it's a boatload of baloney

First, let us pause to reflect back to when all of this began about a year ago. Stock investors believed in large that tariffs were just negotiation bluffs that would quickly end in a mid-summer agreement without ever going into effect because neither side would allow that kind of economic damage.

Mid-summer hope faded to late-summer hope as businesses stocked up in anticipation of the tariffs. Then tariffs went into effect, and hope moved on to autumn and then to winter ... and then renewed in the spring. Now hope is moving to summer again. Only this time the new annual round begins with tariffs that are high enough to be damaging.

So, I call baloney on the continuous argument that these are just negotiation bluffs that will quickly resolve because neither side really wants to go down this path. While it is true they don't want to go down this path, down it we are! So, baloney!

Second, China immediately vowed to retaliate on Friday, and the market remained almost unconscious of that fact. (Probably again all kidding themselves with "this is just negotiation blunder.") That means equally intense tariffs will be imposed on American goods going into China. If you are among the denial crowd that thinks China is about to flinch or is bluffing, stop and actually evaluate what this means.

You don't state you are going to establish retaliatory tariffs and then flinch before they go into effect unless you have a peculiar desire to look stupid and weak in front of your own people. Does Xi really strike you as a leader who is willing to look stupid and weak to the Chinese people and to his colleagues and political competitors? What evidence have you seen to back that hope up?

Just note how the prevailing wisdom reversed in just one week:

Prior to U.S. Trade Representative Robert Lighthizer’s Monday comments, Cowen had assumed the "‘Great Man’ theory would hold, Trump and Xi would have the best conversation, talks would continue, and Trump would put tariffs on hold for ~30 days,†Krueger wrote....

Right there, you can see how foolish the market was. All of last week, the market realized that wasn't likely. In fact, it didn't even come remotely close to happening, but that is the dope the market used to get its new highs in April.

“To paraphrase Lenin: there are decades where nothing happens and there are weeks when decades happen…and then there is a single week in the Trump Presidency. What a time to be alive.â€

And that was written last Tuesday before things got really interesting.

If you are grounded and not one of the flying zombies, you will realize right off that Xi cannot afford to bluff about retaliatory tariffs and then look weak. Everyone has had plenty of months to realize that looking weak is not in his character. Nothing China has said has been a bluff so far. So, retaliatory tariffs are as good as a fact now, but the market chose to keep living in pretend land and didn't even respond to that.

Since the market was too dopey on Friday to figure it out, I'll spell it out: retaliatory tariffs take a few days or weeks to lay out, depending on how thoroughly the background work has been done. You can be sure most of it has been done, but the Chinese government would like to take a few days I'm sure to see if the mere threat will get Trump to back down before imposing them. Trump isn't going to back down mere days after implementing tariffs, which he plainly believes will be effective against Xi. So, Trump and Xi are now locked in a Trumpian handshake where Trump has pulled Xi in close, and the first to let go knows he's the weaker man. If Xi backs down first, he'll look like he flashed his fangs, then immediately flinched and failed.

So, the GS-noted fact that "We have two weeks before all this goes into full effect," doesn't matter. The market chose to ignore the most likely outcome and place its money on the least-likely outcome.

Investors may be betting, as some analysts said, that China's retaliation will force Trump to back down because he cannot go full-battle in an election season; but to keep betting stocks up on that basis, you have to be willing to believe Trump is willing to risk looking weak to his base in an election season. That argument hinges on the belief that Trump can sell snake oil to his base, and they'll buy it.

While we all know Trump has the ability to spin a deal to sound much more glorious than it was, so far he has not done that in his negotiations with China. Yet, people who are trying to talk the market up have been saying he will for months now. If he was willing to do this, why didn't he this week? He still has to have something to sell, and he clearly didn't think that whatever he had in hand would suffice ... if he's even willing to try to sell something he doesn't like. The market was counting on him all of last month to pitch whatever he came up with, and clearly the market was dead wrong. It didn't happen. The parties have all returned home.

Even Democrats are more or less with Trump in agreeing that China cheats on its trade deals in ways that have to be dealt with. So, Trump doesn't have a lot of political opposition to battle on this. It is more the weaklings on Wall Street who lust after short-term profits at any longer-term expense who are lobbying Trump to give it up and spin it up.

So, if you believe China is going to get Trump to immediately back down on the tariffs he has already now imposed by retaliating, you have been believing this kind of nonsense about bluffery for almost a year! Therefore, again, I call baloney! Sure it could happen, but it is far from being the most likely bet if you're going to price stocks based on where the economy is most likely to go based on what we've seen of these two sides in the past year.

For those who are among the many caught up in this market madness, let me spell it out again: (Mostly I spell it out to aid the few who are not caught up in it feel a little more self-assured that they are not somehow missing out or failing to connect the dots correctly.) It takes about a month for these tariffs to work their way through the system and start showing up in the prices on store shelves or Amazon pages. Then it will take another month for China and the US to start seriously feeling their impact in statistical reports.

So, it's two months minimum before either leader feels real hand-squeezing pain from this. Now, how hard and long do you have to squeeze before one of two people who are both totally unwilling to look weak, Trump having just publicly staked his very campaign on this, is willing to cry uncle?

Trump also clearly stated there is "no need to rush" negotiations. You can believe that is bluster, too, if you already believed everything for the past year has been bluster. However, I say that statement adds all the more credence to my realism that says this is going to take time to play out. Trump knows it, and is trying to ready the public for that. So, baloney!

If you still think Xi will back down quickly, consider China's response this weekend in which publicly clarified what it will take to get China to back down from its tariff retaliation:

In a wide-ranging interview with Chinese media after talks in Washington ended Friday, Vice Premier Liu He [China's chief trade diplomat] said that in order to reach an agreement the U.S. must remove all extra tariffs, set targets for Chinese purchases of goods in line with real demand and ensure that the text of the deal is “balanced†to ensure the “dignity†of both nations.Liu’s three conditions underscore the work still to be done if an accord is to be reached between the world’s two largest economies.

That doesn't sound to me like something Team Trump is ready to do to reach an agreement. The focus on maintaining dignity as a primary requirement for reaching a bargain underscores what I said above about Xi not being willing to do anything that will make him look weak in any way.

According to Ely Ratner, a China expert who served in the administration of President Barack Obama and is now director of studies at the Center for a New American Security think-tank, “The question is can the Chinese come back and offer enough such that Trump can sell it...? It is going to be hard for them to do that in the face of Trump escalating. I think it gets harder as this thing goes on, and it gets harder politically for Trump.’’

Positions on both sides are clearly hardening in public statements, so things have became harder on Friday for everyone to back down from not easier. That means betting on softening during what GS called a "soft deadline" for the next two weeks seems like a bad bet. I think the market is smoking weed, popping mushrooms and snorting crack at the same time to have taken Friday as a sign of a little reprieve. It'll be even more of a surprise if it doesn't start to wrap its head around this stuff on Monday.

Third, stocks rose when Treasury Secretary Stephan Mnuchin said that trade talks were constructive. Baloney. They may have been constructive, but we've heard that with every talk for nearly a year now. So ... so what! Do you really think Mnuchin or his Chinese counterpart, Vice Premier Liu He, ever will come out and say "Talks went nowhere?" The fact that they said that is no reason for markets do do anything. It was a given they would say that. They say something of that kind every time, and they never would do otherwise unless they want to deliberately crash their own markets.

According to Bloomberg in the article above, people familiar with the discussions have said that the mood around negotiations has become increasingly gloomy in recent days. So, while the chief diplomats put a good face on things from both sides publicly (as they must), reality may be much different. (While the old vague "people familiar with" as a source doesn't go far with me, why would you bet up stock values when relatively bullish publications like Bloomberg note that the mood around the talks is somewhat dour? Seems the wrong direction to me.)

Only pure hopium sends stocks higher just because these guys walk out of talks with nothing real to show but say things went "constructively." That's like seeing a new car ad that claims "excellent vinyl" or "engine runs." If that's the best they can boast, stay clear. If you want to talk about a group of people willing to buy snake oil, it's naive for investors to get excited by that kind of dealer salesmanship. You haven't driven a single car around the block if you put any stock in statements like "talks were constructive" in an environment where saying anything less than that would cause both nation's markets to crash; but the market heard what it wanted to hear in order for irrational exuberance to attempt another climb.

Then Trump tweeted that tariffs could be removed and that talks will continue. Again, of course, they will! Do you really think he'd ever tweet that "Tariffs are hear to stay because talks are over for good?" Come on! The market is flying on any whiff of hot and weedy air it can find!

Here's how inane some reporting gets. AP reported,

The market’s gains this year had been slow but steady up until this week.... It’s been mostly up amid a mostly muted year with no major market-moving news.

"Slow but steady?" The helium heads have gone so far out of their minds that they actually find Trump Rally 2.0 to be "slow but steady" when they should find it to be one of the steepest inclines of irrational exuberance ever plotted. What is their understanding of reality if this year is called a "slow but steady" climb? They are writing in a delusion where normal is an even faster rise than what we saw in the first four months of this year.

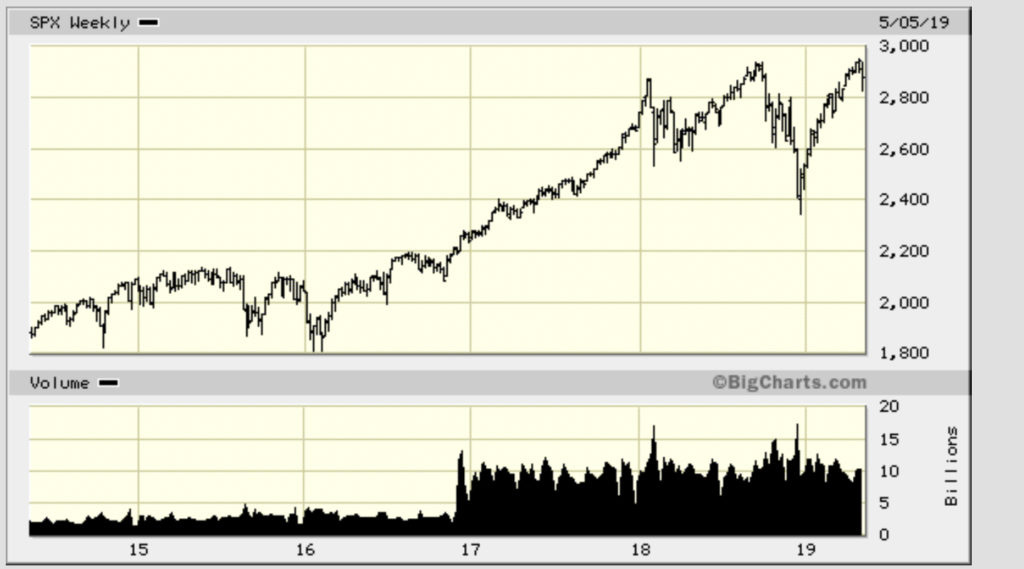

As for "muted," I hope the writers only mean the news that markets pay attention to has been muted, but that is exactly what makes the rise, which was anything but muted, an even more obvious float on hot air! Look at the last five years of the S&P 500, and tell me the start of this year (final column) had a rate of rise that was "slow" or "muted" compared to any other year:

If market news was muted, the rise was all the more hyper-inflated. Only the most exuberant tail end of 2017 compares. That kind of coverage is its own example of how irrational exuberance has now become to where the trajectory of 2019 would be called "slow but steady."

This is the same opiated nonsense that passed for financial reportage during the build-up to the dot-com bust. Some people back then wondered how no one could see all the froth. I wonder now.

As for stocks rising when Trump said he got a "beautiful letter," really? That somehow outweighs Trump saying "New tariffs have begun today?"

As for the stated notion that stocks rose because stocks had already priced in the tariff increase, when was that? Did they price it in during all those months when they were shooting for the moon and hit a new high? The only week of significant falling was this past one; but does a 2-4% drop for the week price in the new reality of all the costs I laid out above? Hardly. Just more hopium to try to keep things floating into the sky.

Where do we go from here?

While I love the fact that Trump is battling the globalists, he is fighting them all at the same time. Remember, he knocked out the TPP, dissed the World Trade Organization, and has set tariffs on Europe. He's kicked every hornets nest he could find. So, he'll need God on his side to win this war as alliances between China and all the rest will strengthen, which is another reason to think this is not likely to end soon. The market is betting against reality.

While a few prophets have risen to claim, as I would phrase their predictions, that Trump is God's Nebuchadnezzar (the ungodly emperor of Babylon that the Bible says God used to destroy Israel and put the Middle East under a single empire), I have no reason to put faith in any of them.

A better path could have been taken. If Trump were more shrewd he would have, instead of creating a tariff war in multiple theaters around the world all at once, tried to create a coalition of American trading partners against China (using America's strength to get their participation) and focused on taking down the biggest guy in the cell block first with as much help as possible. He could probably get some support from other nations to crimp China harder because China is doing the same thing with all of its trading partners.

As it stands, however, China has numerous trading partners it can continue to work with in free trade to help it survive America's tariff attack, while America may be facing counter tariffs from Europe as well as from China. Trump will not likely find any support from other nations because the odds-on likelihood is that he has already started a tariff war with them, too. Their smart play, if you are thinking from their point of view, would be to align with China and take down Trump in order to end their own Trumpian tariff battle.

Do I know I am right about this not going away anytime soon? Not at all. The Trumpettes who believe Trump is God's horn may prove right, but I'm not trying to discern the lay of divine intervention, which is beyond my divining. I'm just looking at the economic lay of the land.

My point in all of this is not to say, "This is where things are going," but that "you are continuing to bet against all odds if you are investing on basis that the tariff wars will be settled soon" (or if you believe Trump is on God's side). You are betting on the 10% likelihood (or a miracle from God), rather than the 90% likelihood. 90% of bets on Friday appear to have been placed the 10% likelihood.

That kind of setup is when fortunes are made and lost. The big money is made in a contrarian manner by betting against the lemming pack when the lemming pack is betting based on pure adrenaline and emotions against all reason. (I'm not making any recommendation to anyone here, however, because that is a high-stakes gamble in that we all know the lunatic 90% have a lot of power to keep pushing things beyond reason longer than a reasonable persons thinks they possibly can because the human capacity for insanity is nearly infinite. (Of course, just maybe, that makes them NOT lunatics because what some of them are really betting on is mass delusion knowing no bounds. There is a lot of basis right now for that belief, too.)

Am I saying the market should crash because of tariffs? No. I'm saying the market may well crash all over again because of foolhardy greed like we saw in the dot-com bust. (And, of course, those who want to rationalize this will look for all the ways that now is different from then, but that misses the point that what is not different is the high dosage of denial reddening up the market's veins.) When you see the market operating this much based on sheer hope in the face of clearly flagging earnings while ignoring every downside piece of news that comes along, even horrible economic news like we got Friday, that is the kind of fever that ends in even bigger crashes than the polar-bear plunge the market took in the final quarter of 2018.

Maybe Friday will prove to be a last hurrah for this euphoria, and the opiated market will get whiff of Narcan on Monday. After all, the last week overall was the worst since December's conflagration. So, maybe some reality is creeping in. It should be the last hurrah; however, hopium-addled, fevered brains may continue to prevail.

Here is a little evidence that even Bloomberg noted to indicate reality may be making a new appearance in the markets, in spite of what Friday indicated:

When the first Trump tweets hit on Sunday, Paul Nolte knew the peaceful days were behind him in the stock market.

“Have you ever seen the movie ‘Airplane’? It was just a bad week to stop sniffing glue,†said the 56-year-old portfolio manager for Kingsview Asset Management in Chicago. “When that got announced, it was like, well, this is going to be a volatile week.â€

For investors who were already unsure whether to ride this rally or run from it, the last five days have been a wake-up call. Not a tipping point, necessarily -- most said they were too shocked by the torrent of headlines to do much -- but it hasn’t made the decisions any easier. How will tariffs influence corporate earnings? The economy? Is Trump pursuing sound policy, or just campaigning?

“Anybody that thinks that they can divine what’s going to happen here, that’s just guessing,†said Liz Ann Sonders, chief investment strategist at Charles Schwab.

And CNBC noted,

“Fasten your seatbelt and don’t hold your breath,†Bank of America strategists wrote in a note this week. “The latest escalation of the trade war was completely unexpected...."

So, Monday could be that day of going back to work with a hangover headache from Friday's revelries, which is how I anticipate Friday's buyers will return as reality keeps pounding its way in like spikes into investors' temples. We all know, nothing sets the market up to crash like investor blindness, particularly the kind that forms under denial created by blind greed that denies unwanted realities because of its quest for boundless returns in the rush of irrational exuberance.

Still, I won't bet on it by going short (because I'm not that risk-taking). Fever can run hot longer than one imagines before insanity causes everyone's heads to explode. As long as stock buybacks continue to be the one-trillion-dollar-per-year hot-air balloon lifting market indices, then the market can possibly rise even if real apocalyptic events like an asteroid impact were to happen. It can rise until the monumental corporate cash piles from repatriation and tax savings are spent (which will simply have to be spent a lot faster in the event of an asteroid impact) .... or just until the corporate principals have used company cash to buy themselves out over enough time to make that legal, to where they can, then, let the smoldering shells of their corporations crash with companies having nothing to show for all the cash spent, except safe, wealthy executives and board members, who will use the cash they withdrew to buy their corporate stocks back at fire-sale prices after the crash while mom and pop, who rushed into the flames (as always), move to trading at Goodwill for some decent rags to dress their burns.

In which case, the collective attitude of the market manipulators is "America be damned, but Hail Mary, Halelujah!" Exactly the kind of greed that breaks markets completely apart.