As another Inflation Foreshock Rattles Markets Around the World, Fed not Fazed

Stock markets got a jolt of the wrong kind on Wednesday when release of Fed minutes showed a little more talk of the Federal Reserve tapering its stimuli took place than what Fed Chair Jerome Powell let on earlier in the month after the FOMC meeting, which sets monetary policy.

While the news was as insignificant as a nose hair, stock markets, bond markets, gold markets, and crypto currencies all shuddered at the thought that the Fed might have to start to think about whether it should start to think about tapering sometime in the unforeseen, indefinite future.

The fact that global markets shook so much at a mere Fed whisper of tapering, tells you how fragile the Everything Bubble is due to all markets' dependency on the Fed's enormous money supply and its continued rapid growth.

Everything falls

Stocks end lower but cut earlier losses as some members of the Federal Reserve indicate they are open to discussing the scaling back of asset purchases 'at some point' if the economy improves rapidly. “A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases,†said the minutes from the April 27-28 meeting of the Federal Open Market Committee.

The Dow, at one point in the day, had fallen over 580 points, but closed at a 164-point loss. Treasury yields jumped up to 1.692% for the 10-year. Cryptocurrencies, already in trouble because of a couple of weak jokes by Elon Musk, bit the dust in a shattering plunge that saw anywhere from 25-50% declines in a day -- a mere trillion dollars in lost value globally. And then they rebounded some of that to where they were down over a 24-hour period about 11-30%. Just a little a jolt.

The Crypto decline was due to China's talk on the day about restricting use of cryptocurrencies because the central bank there sees them as too speculative, volatile and dangerous. So, it wasn't about the US central bank's taper whisper but about China's central bank; however, it showed that crypto currency is by no means a safe haven in an inflation storm either due to its own extreme volatility. With crypto currencies so susceptible to policies of central banks in terms of how their own member banks play with crypto and with the SEC and IRS looking to add regulations, they are far from being safe havens against inflation. Thus, they all plunged together even on a day when the stock market fell due to concerns of Fed tapering that are being raised due to rapid inflation.

Inflation is not about a hot economy

One of the things declared almost unanimously by market analysts about the recent inflation spike is that investors fear the Fed will be forced to stop printing money and to raise interest because a supposedly scorching-hot economy is creating inflation. That is the kind of universal balderdash I said a couple of articles back I'd have to start correcting. So, here goes:

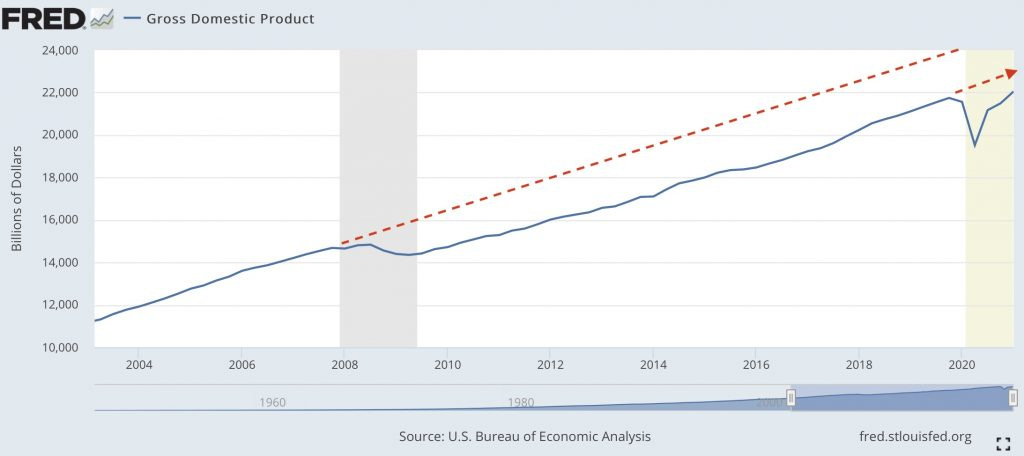

While inflation is hot, the economy is not. Yes, it is recovering quickly from the deep pit it fell into, but it is far from a hot economy, which is why the Fed keeps cranking up the power on its money printing presses (understanding, of course, money is rarely actually printed these days). The economy, in fact, is barely even warm. Here is the economy as it is and where it would have been if it continued on trend without the great Covidcrash:

As you can see, the economy's current rate of rise is not much steeper than it has been for the past decade, and it has not recovered to the height where the decadal trend would have carried us by now had the COVIDcrash not interrupted the flight. We've lost a year of growth, even though population has increased and money supply has more than doubled. That's not such a hot economy, and that's not the reason for inflation. Shame on economists and analysts for not figuring this out just because they all have an optimistic narrative they want to believe in.

The simple truth is, as I've been saying for months, this high inflation was predictable months ago and is happening because too much money is chasing too few goods. The money is not there because the economy is hot. The money is not there because employment is full. The money is not there because wages are rising.

The money is there because the Fed keeps printing it, and the Federal government keeps distributing it to the unemployed (and nearly everyone else). The other thing that is there in this badly broken economy is shortages -- all over the world in all kinds of materials and products.

I keep repeating this truth because analysts and economists keep repeating the lie. That is why the economic geniuses did not see this inflation coming, even though I've been laying out the likelihood of high inflation for almost a year in my Patron Posts.

That is also why the Fed will run "the presses" too hot for too long. It also believes that a hot economy is the only thing that will create high inflation and that will happen because a hot economy will drive wages up. The Fed is being blindsided by its ignorance. So, it will, as it has said many times, keep the money presses running hot until employment gets back where they want it, which is absurd because the Fed cannot create employment when it is creating money that is keeping people unemployed by paying them more to remain unemployed than if they go back to work.

The Fed, on the other hand, can do nothing about shortages, and it is shortages that cause people to bid up prices not possession of money. If you really want something, you don't pay more for it in a competitive marketplace just because you have more money; but you will pay more to get what you need or want in a badly broken marketplace riddled with shortages if you have the money to do it. Money creates the ability to bid up prices; but shortages create the need. The company that offers to pay more, finds a way to get limited goods transported to its warehouses. It then sells those goods for much more to desperate customers who will pay more to get what they need or greatly want.

The Fed only has its eyes on the unemployment gauge, which still looks terrible, and the wage gauge that sits right beside it; but the money flooding the country is not coming in through wages. It is through welfare. So, the Fed doesn't fully see or understand the inflation that is building around it, and neither apparently do financial analysts or economists, which is why I write this blog. That is why the were all shocked by April's inflation print while I would have been surprised if April came in any lower, and I expect May to be higher still unless there are a lot "adjustments" to the numbers to bury inflation.

The Fed can't have you believe inflation is going to run much hotter for longer because that awareness will crash everything; but it is going to have a hard time hiding what is now coming upon us and an increasingly hard time jawboning all markets into believing there is nothing of concern here. That's what Wednesday's market jolt showed -- fragility in the market place toward inflation fears.

Reverse repo crisis says banks have been Fed until too fat

There is more than one way to see clearly that the Fed has already overshot to where too much of the world's trade currency is already flooding the global financial system. One of surest is the Fed's sudden need to deploy Reverse Repos.

In 2019, I wrote a lot about the Repo Crisis the Fed was creating by taking bank reserves down too far. Since then it has built bank reserves up way too high. When this happens, banks look to offload some of their reserves to the Fed with what is called "reverse repos," wherein the Fed essentially pays banks to suck some of their reserves away.

That is where we find other far more interesting news in the FOMC minutes released on Wednesday than the mere whispers about thinking about thinking about tapering. The minutes noted that reverse repos with the Fed have skyrocketed recently.

The overnight reverse repurchase agreement (ON RRP) facility continued to effectively support policy implementation, and take-up peaked at more than $100 billion.... A modest amount of trading in overnight repurchase agreement (repo) markets occurred at negative rates.

That money-sucking surge of overnight reverse repos looks like this:

{kind=link}

Remember when the Fed had to start pumping in a hundred-billion dollars a night to stem the flood of red ink in bank repo loans. Now its having to suck out a hundred billion a night to keep money take money out of the system, even as it insanely keeps putting money into the system by buying US treasuries to keep funding the gorging government.

Says, former Fed staffer Zoltan Pozsar, who was the main ringer of alarm bells just before the 2019 Repo Crisis hit, and who was spot on in his warnings of bigger impending problems if the Fed didn't reverse its tightening back then,

The heavy use of the o/n RRP facility tells us that foreign banks too are now chock-full of reserves.... Use of the facility has never been this high outside of quarter-end turns, and the fact that the use of the facility is this high on a sunny day mid-quarter means that banks dont have the balance sheet to warehouse any more reserves at current spread levels.

It's a sign that money if flowing over the brim. To keep things short and sweet, I won't go right now into descriptions of how Reverse Repos works, but you can read how they work here if you need to. In short, this extreme level of reverse repo action reveals there is too much liquidity sloshing around in the banking system. We're in a bizarre situation where the Fed is hosing up US Treasuries to fund the federal government and then putting them right back into the market through reverse repos so banks can park their surplus cash in them by buying them temporarily from the Fed.

In short: the US financial system is starting to groan at every incremental new reserve created by the Fed's QE… and considering that there is at least $1 trillion more in QE to go, even with tapering, things could turn ugly soon. This, much more than any flip-flopping commentary from the Fed, confirms that we are rapidly approaching a critical moment when the Fed will no longer be bale to conduct $120BN in QE every month, as sooner or later someone will figure out that the Fed buying up hundreds of billions in securities only to turn around the then repo out the resulting reserves each and every day, amounts to outright debt monetization with potentially calamitous consequences for yields and the US dollar.

That is the financial precipice upon which the Everything Bubble now rests.

With the crypto market having just crashed in a single day, after weeks of declining, and the treasury market back to rising yields that are bumping up close to the 1.75% level on the 10-year that coincided with the market's last little bit of trouble, and with inflation so quickly hitting 4.2%, well above economists' estimates because they were basing their inflation guesses on their perceived hotness of the US economy, not on widespread shortages and force-Fed cash, who cannot see as much trouble brewing right around the corner as we saw in the Repocalypse?

Only it is trouble of a different kind, and I would say of a much worse kind.

Fed can't fix short supply

The Fed can't fix shortages of goods and services due to people staying unemployed, therefore unproductive, if politicians want to keep giving them money. Neither is that the full extent of the unemployment problem. The cannot fix shortages due to businesses that closed permanently over the past year; nor can it fix supply chains that began breaking down with the trade wars and then groaned and buckled more under COVID strains that shut down international transportation, especially between the US and China.

At the same time, the Fed and feds are fueling everyone to be able to pay more in order to get their hands on what they can, and Fed won't stop fueling the economy in time because it has its eyes on the wrong gauges, believing the nearly universal party line that inflation is only going to come from a hot economy pushing up wages. So, while they are watching wages, inflation is already well ahead of them.

The transportation side of the shortage problem is not going away soon either. Demand is surging due to plenty of cash during the reopening, so is transportation; but orders are backing up at ports, causing shippers to bid up container costs. Warned Nerijus Poskus, vice president of global ocean at freight forwarder Flexport,

"It’s not getting better. It’s getting worse.... What I’m seeing is unprecedented. We are seeing a tsunami of freight. For the month of May, everything on the trans-Pacific is basically sold out. We had one client who needed something loaded in May that was extremely urgent and who was ready to pay $15,000 per container [more than double the typical rate]. I couldn’t get it loaded — and we are a growing company that ships a lot of TEUs [twenty-foot equivalent units]. Price doesn’t always even matter anymore....

Sadly, the freight story between China and the US says the US lost the trade war. You see, shippers cannot find enough containers to ship goods from China to the US because so few containers full of goods are shipping from the US to China. As a result, major shipping companies are sending shiploads of empty containers back from US shores to China.

Dead-heading, as truckers would call that, is not something any shipper wants to do; but all those out-of work people in the US aren't producing product to ship. And producers in the US can't get all the parts they need to ship products, and maybe, just maybe, Chinese tariffs were more effective than US tariffs. For whatever assortment of reasons, shippers are having to send tons of containers back empty so more goods can be shipped to the US. That's a way of visualizing the expanded trade deficit.

This may sound like demand from a superheated economy; but a lot of this is due to restocking in the US now that economies are opening back up as COVID restrictions are relaxed. GDP (i.e., Gross Domestic Production] is down. We're not producing nearly what we were before COVID, so we're not superheated in that sense; but demand is strong because people have money even though the economy is producing at a level we'd normally call recessionary. Thus, we must try to get products from outside the country while we have few to sell in this horribly lopsided, wounded economy that some are calling "hot."

And this inflation is not merely "transitional":

"Restocking is actually affecting the trade even more than growth in demand. That tells me that this will last even longer. Let’s say U.S. consumer demand slows down in Q3 and Q4. That’s not expected, but even if it does, [capacity availability and rates] shouldn’t improve quickly, simply because of the huge restocking demand...."

Poskus also believes there is a growing export backlog piling up each day in Asia, awaiting available ship slots. If that backlog grows too big, he said, “I honestly don’t know what’s going to happen.†As a result of the backlog and restocking demand, he thinks “prices will remain high and shipping will probably remain difficult for the rest of this year."

In shipping alone, the problem is not so transitory as the Fed maintains, so those who have cash will continue bid up containers to get them, as they are doing. That means, of course, the cost of everything imported goes up because businesses and consumers are willing to let those costs pass through in order to get the goods.

“Buckle up. The month of May will be the worst people have ever seen,†he predicted. Because some shippers will have to wait in line behind the growing backlog in Asia, he expects “what’s going to happen soon is that some importers won’t even be able to get on the boat. For them, it will almost feel like trade is coming to a halt.â€

Because the various causes of supply shortages are not problems the Fed can fix, inflation is not transitional. The Fed is out to lunch. Shortages because freight won't be up to demand for months to come. Shortages because US producers don't have parts that they cannot get shipped to create what is needed over here. Shortages because US producers cannot get employees who make more products. Shortages because demographics changed abruptly under COVID to where people are relocating all over the US, creating massive product demand and resource demand in order to build new houses and new infrastructure. Shortages because of businesses that do not even exist any more due to COVID lockdowns.

Everywhere there are shortages. As inflationary pressures build in ways that will not easily prove transitory, as the Fed claims, the stock market groans, the bond vigilantes get itchy feet, and worry starts to build in the air ... as it should because there is something reasonable to worry about.