Is the Housing Market about to Top Out?

Several signs have appeared in the past few weeks that indicate buyers are suffering from fatigue and may have gone about as high as they are willing or able to go. While housing prices have shot up for months, wages have stagnated. Government stimulus checks have offset that, but you cannot really make a long-term home-buying decision based on temporary stimulus when you don't know if it will even continue through the year. Supposedly that government stimulus is supposed to wind down later this year, but who knows?

Home sales have been in decline for months!

Believe it or not, existing home sales tumbled for the third month in a row in spite of all we hear about the hot housing market. The following graph shows why the market is still considered scorching hot even though sales have fallen each month since January (which was flat) compared to the month before:

While sales have dropped each month -- and even though they had been making a drop year-on-year, too -- in April we entered that month where sales a year ago plunged to almost nothing because open houses were shutdown in the COVID economic lockdown across the nation. So, the YoY prices are skyrocketing because of a genuine base effect wherein sales numbers a year ago fell off a cliff (as opposed to the fake base effect referenced for inflation where prices did not fall last year but experienced for the most part very low inflation). Now we're comparing to genuine plunge in sales last April.

The year-on-year rise in sales is, therefore, not meaningful.

Existing-home sales were expected by economists to rise modestly month-on-month (about 1% ), but they fell almost 3%. New-home sales were also expected by economists to rise as we moved further into sunny springtime, but they did not. We see essentially the same story for new-home sales, but without quite the prolonged decline month on month:

Because the drop in new-home sales is only one month long compared to three months for existing-home sales, the year-on-year rise against last year's atrocious April is even more distorted.

April new-home sales fell month-on-month nationally by almost 6%. The only region where sales increased was in the Midwest, perhaps due to migration away from the highly populated coastal areas (up 0.8%).d

Housing prices still flying high

Prices have not fallen, but they typically do not start to fall until sales have been in decline for, at least, six months because seller's, unless they have to sell, are reluctant to take less than they could get only a few months ago. So, it would be totally typical for any price decline to significantly trail a decline in sales.

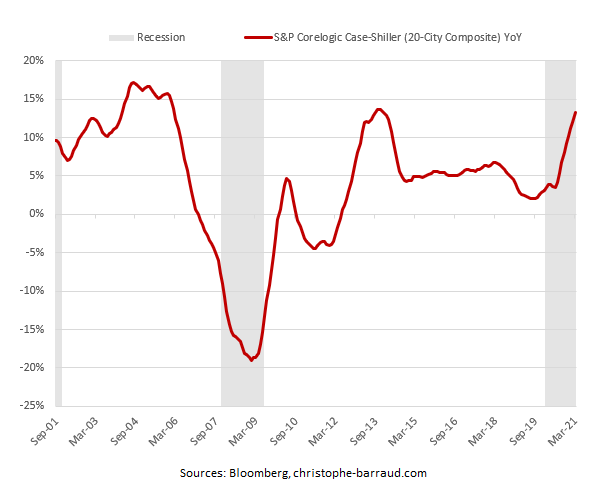

Year-on-year prices were up nationally 13.3% in March, according to S&P CoreLogic's Case-Shiller Index, which is a composite of 20 major cities. That looks nasty ... like this:

Bear in mind, however, year-on-year means you are comparing to last March when prices were already settling a little due to homeowners being reluctant to host open houses because of COVID even before the nationwide lockdown. On the other hand, this index tracks major cities, which is where people are supposedly exiting, so price gains could be worse in suburban and rural areas.

The index's founder, Nobel prize-winning economist Robert Shiller, summarizes the situation as follows:

In real terms, home prices have never been so high. My data goes back over 100 years, so this is something.... We have a lot of upward momentum now. So, waiting a year probably won’t bring house prices down.

According to Shiller, current home price action is also reminiscent of 2003, two years before the slide began. He notes the dip happened gradually and ultimately crashed around the 2008 financial crisis....

“If you go out three or five years, I could imagine they’d [prices] be substantially lower than they are now, and maybe that’s a good thing,†he added. “Not from the standpoint of a homeowner, but it’s from the standpoint of a prospective homeowner. It’s a good thing. If we have more houses, we’re better off.â€

Other indices with a broader scope show a similar trend with a sudden steepening:

The FHFA's YoY price increase for March is the largest in its history. So, prices are still climbing quickly, and, barring a national calamity from the total bursting of the Everything Bubble, past experience says they will take a few years to find a new bottom even if the market tops out in price later this year. The fall-off in sales gives, at least, some hope to home buyers that prices may not be able to rise much further as buyers appear to have stretched as far as they can reach.

Glenn Kelman, CEO at Redfin, agrees that housing prices have never been so frenzied but also states he thinks the frenzy is about to flatten out:

Kelman said the housing market is a frenzy, with most houses selling above the asking prices, which has never happened before. After record gains in the first quarter, some home prices are likely to stall. Kelman ... told Pellegrini that people placing bids well over the asking price might find their loan denied because the appraisal level will come in so much lower than what the house is worth. Kelman warned: "I think you're going to see a little bit of air come out of the ballon."

Kelman believes we could still see some rise in prices in the Midwest due to migration patterns, which squares up because it is in keeping with what we are also seeing in sales.

Goldman Sachs, on the other hand, believes housing prices will keep climbing all the way into 2024 at a pace faster than what was recognized in the 2006-2007 building of housing bubble.

You can see the difference in how all of this making home builders feel versus how it is making home buyers feel in this graph:

In fact, look at what has just happened to home-buying intentions:

Home buyers haven't felt this low in, at least, twenty years!

So, I am thinking Kelman is more likely to be the one who is right here and that the frenzy in prices will start to calm down. I won't say cool off, as in decline, but settle down to where we don't see the completely bizarre scenario where almost every home sold got bid up in price in most markets across the nation, except uncherished urban markets.

As an aside from the housing question, this certainly should increase pressure on the Fed to stop its Mortgage-Backed Securities purchases, even if it continues sopping up treasuries to fund the US government. That is not completely aside from the housing question because, IF it happens, it could make loans harder to get. It's just that -- so far -- the Fed still maintains it is not even starting to think about that. One has to wonder already, however, why the Fed is continuing to buy MBS when there is melt-up in housing prices and an ...

Inventory plunge

The question that has to be asked with these falling sales, though, is whether sales are down because buyers are saying, "That's it. I'm done," or because inventory has fallen so low there are even fewer homes to sell than there were a few months ago. You can't sell what isn't there even if buyers are still fully charged and ready to go.

That looks like it could well be the case.

The sales decline in April “is due to the lack of homes on the market,†Lawrence Yun, NAR’s chief economist, said on a call with reporters. “Even with home sales declining modestly, one can describe the market as being hot.â€

To be sure, inventory has rarely looked worse. It popped back up a tiny bump last month but not enough to mean anything for sales ... at least, nationally:

So, it is reasonable that inventory could be the main factor in declining sales, though the sentiment graphs above show buyers have never felt worse, either. IF inventory rises, I think we'll see prices start to flatten and bidding wars start to cool off in the summer for the reasons given above.