It Was Hell Week, and the Fed Can't Handle the Heat

Jamie Dimon, CEO of JPMorgan Chase, set last week off with a fitting sour note when it was reported across the financial news, he had updated his weather report for the economy:

I said there were storm clouds. But I’m going to change it. It’s a hurricane. Right now it’s kind of sunny, things are doing fine, and everyone thinks the Fed can handle it. That hurricane is right out there down the road coming our way. We don’t know if it’s a minor one or Superstorm Sandy. You better brace yourself.

Dimon indicated his bank was battening down the hatches for some real rough weather. Later in the week Alasdair Macleod, following Dimon's motif, explained why Dimon sees a hurricane brewing on the near horizon:

G-SIBs [global systemically important banks] have accumulated excessive exposure to financial assets, both on-balance sheet and as loan collateral. With vicious bear markets now evident and further interest rate rises guaranteed by falling purchasing powers for currencies, the one thing regulators have not allowed for is now happening: like a deepening meteorological low, bank credit is contracting into a perfect storm.

Jamie Dimon’s recent warning that his bank (JPMorgan Chase) faces hurricane conditions confirms the timing. Central banks, bankrupt in all but name, will be tasked with rescuing entire commercial banking networks, bankrupted by a collapse in bank credit....

Financial assets are in a bear market, driven by persistent rises in producer inputs and consumer prices, which in turn are pushing interest rates and bond yields higher. So far, investors have been reluctant to lose trust in their central banks which have been instrumental in supporting financial markets. But this is now being tested, more so in the summer months as global food shortages develop.

We have increasing evidence that bank credit is either contracting or on the verge of doing so....

Macleod explained that the core problem, even for central banks, is the ongoing bond-market wipeout where, if bonds are priced to market value, many banks -- even central banks -- are deep in the red on their balance sheets:

The Fed recently admitted that unrealised losses on the bonds on the asset side of its balance sheet stood at $330bn at end-March, which wipes out its balance sheet equity of $50bn more than six times over. Since then, bond yields have risen a further 1%, increasing the deficit to closer to $500bn.

While Dimon's proclamation set the tone for the week, CNBC bookended it by describing the week, once markets were closed, as follows:

Wall Street and the Federal Reserve appeared to enter a new reality this week, and the result for investors was big losses with no obvious end point in sight. The S&P 500 posted its 10th down week in the last 11, and is now well into a bear market. On Thursday, all 11 of its sectors closed more than 10% below their recent highs. The Dow Jones Industrial Average fell below 30,000 for the first time since January 2021 this past week.

They also noted a point I am prone to keep reminding people of -- there is no Fed save coming on this one. Father Fed won't be putting a bottom in for the market's fall. I have read frequently, even on popular alternative financial news websites, that Powell will soon be capitulating with the famous Powell Put, but my own response to that has been, "Not on your life. Not until the economy already lies in the ruins of recession and recession is bringing inflation back down."

Of course, by then, the dirty job is done. The bull will have had its guts strewn all over the field by the bear, and the Everything Bubble will be foaming its way across the field to wash away the bull's blood with scrubbing bubbles.

As Mohamed El-Erian explained:

Inflation has become so extreme it is not just forcing the Fed to tighten more aggressively than it has in decades, but it is forcing several central banks, including the Swiss National Bank, to tighten aggressively at the same time in somewhat of a currency war to maintain their positions relative to the Fed. With CBs jockeying to align with the Fed's tightening around the world, Bank of America equity strategist Ajay Singh Kapur joined El-Erian by warning that it is time for investors to stop fighting the Fed and its cohorts in global financial instability and give up the buy-the-dip mentality:

In a bear market, heroism is punished. Valor is unnecessary, and cowardice is called for in portfolio construction — that is the way to preserve capital and live to fight another day

Stocks were far from being the only bloodbath in the streets last week.

Bitcoin dropped more than 30% in a week amid reports about blowups of crypto-focused trading firms. Treasury yields, which move opposite of bond prices, have spiked.

Foo-Fighter Fed

With all of the week's financial destruction, you might think financial analysts are begging the Fed to stop. However, not all analysts want to see the Fed's FOMC rush back in to save the market. They prefer to take the destruction and see the Fed finish its fight against inflation because inflation erodes everyone's wealth, and markets have been running negative all year, even before the Fed did any fighting ... when all it was doing was a lot of big talk:

“These people need to fight inflation as fast as possible and as hard as possible. And the market has consistently been behind the curve on trying to understand how aggressive this Fed was going to be,†said Andrew Smith, chief investment strategist at Delos Capital Advisors.

Hopefully, you are among those who have accepted the fact that the Fed is not going to ride in like the Lone Ranger and save the day and that this time is different than anytime most investors alive today have experienced due to searing inflation. However, if you're too young to even know who the Lone Ranger is, then you are also too young to know what a monster inflation is. So, please do yourself a big favor and get the message completely now, albeit halfway down in the battle: A Fed save is not going to happen -- not until it is way too late to matter. The Fed will arrive like the cavalry when everyone on the battlefield is either dead or writhing in blood because it has to keep fighting inflation, which ripping into everyone one the battlefield with its teeth and claws. So, the Fed can't rush in with its usual medicine right now even as it is killing investors under friendly fire. It's a mess.

The Fed will fight until it sees inflation retreating just as Powell has said. He cannot run from this battle because everyone expects him to fight it, whether he can do much about it or not. After two decades in which the world has watched the Fed's various forms of loose policy pour money into markets and create bubbles that many warned about, no one will forgive him if he cannot wrestle inflation back to the ground as it destroys their retirement nest eggs and creates significant pain in their current costs of living. If Father Powell fails, the Federal Reserve's sole proprietary product will become decreasingly significant.

He will never get interest high enough to kill inflation by pushing it down with interest that is higher than the inflation rate because, long before he gets that far, the Everything Bubble will have broken over the entire planet, and all nations will be deep in recession, and the crushing global economic recession will be doing its own work of destroying demand by destroying purchasing power until the global economy's natural corrective forces do the job for him.

Faith in the Fed is almost dead

Powell and his cadre of banksters are already losing the faith of the masses, and faith is really the only thing they have to sell, as their money is backed by nothing other than the Fed's good faith and credit. So, lose faith, and the Fed loses everything, including the power that will be stripped away from it if its fiat currency continues to rapidly devalue, robbing all people who bank in dollars of their wealth.

The Federal Reserve’s missteps in waiting too long to tackle the greatest run-up in prices in four decades has shaken trust across markets and the American public that it is up to the task of curbing inflation.

That, of course, is why Powell had to pound the 0.75% button down with his fist and speak boldly about doing all it takes to beat inflation back down ... while reassuring the world with vacuous words that the US economy is fundamentally strong. The US economy has rarely looked worse in numerous ways that I'll lay out in my next article, so it is risibly insulting when the Fed says such stuff.

Before assuming bankers like Powell actually know anything about the economy, remember that the same Dimon that now yells hurricane warnings over our shoulders was not that long ago claiming to my great disagreement,

This is the most prosperous economy the world has ever seen. It’s going to be a very prosperous economy for the next 100 years.

Less than three months after he made that obvious-nonsense forecast for the next hundred years, the economy plunged into the Covidcrisis, which was easily the sharpest drop into a bear market and recession since the Great Depression, causing damage we are still dealing with all over the world, including the US no less than anywhere. Obviously, he had been schooled by Queen of the Treasury Janet Yellen in the Buzz-Lightyear school of "no financial crises for the rest of my life and beyond!" He made a similarly absurd proclamation at the start of this year when the present recession was starting to settle in.

Before the Fed's big meeting in the middle of this bloody week, MSN noted the fears that gripped the market ahead of the meeting and that would tear like claws through markets after the meeting:

Financial market volatility and losses deepened on Tuesday, fueled by fears that the Fed continues to misjudge inflation and will come down too hard on the economy, prompting a recession.

Better to fear what is already here late, I guess, than not at all. Not at all surprisingly, the Atlanta Fed came out hours later with its GDPNow forecast revised down for this quarter to 0.0% GDP growth:

This follows the progression I laid out in an earlier article as being most probable:

As we await the next quarter’s GDP report for official proof, note that things are falling fast now, rather than getting better as they would have to if we were going to avoid a second quarter of negative GDP “growth...."

Only a week after my claim that they would almost assuredly quickly revise further down, they are already revising their forecast for real GDP in the second quarter down to 0.9% growth. They are now less than a percentage point away from nothing, and they are still optimistic as far as I’m concerned....

Indeed, they were, but now they are getting real about where we are headed, and markets took the Fed's revised forecast as ugly news for the week that further bore out the Dimonic hurricane warning at the top of the week.

Even more concerning are new signs that families have lost faith in the Fed’s policies. Consumer sentiment in June sank to a low not seen since the 1980 recession, according to a University of Michigan survey. Similarly, a poll by The Washington Post and George Mason University’s Schar School of Policy and Government found that most Americans expect inflation to worsen and are adjusting their spending habits, a mind-set that can make the surge in prices even worse.

In case it's hard to understand how the Fed and feds could be losing faith in the US dollar so rapidly, let me present the following evidence of the quality of their foresight:

How competent did he say he and his buddies were?

A lot of people right now would argue that entire group didn't sound particularly competent, given that they were so far off in the realm of their own speciality and given that the Fed has only two jobs in the whole world -- 1) to fight inflation (maintain a stable currency); and 2) to foster a healthy jobs market. The latter mandate, of course, is a late-comer and should be removed from the incompetent Fed's goals because it is actually the mandate that gives its money mismanagers such gross overreach in managing the US economy as central planners.

History's crashiest soft landing

Everyone keeps speculating about whether the Fed can navigate a soft landing as if it is not already obviously way too late for that now that the top of the plane is skidding on the tarmac. In terms of how well Papa Powell and his flight crew are doing as they play inflation slasher, it sounds like the passengers are already feeling terrorized.

Fed policymakers were already under enormous pressure to slash inflation without inviting disaster for the recovery or spurring a new round of job losses. Now, the Fed is in an even more fraught position, one that goes beyond monetary policy and instead targets the Fed’s most essential tool of all: its credibility.

Look, when even MSN says these things, it has got to be bad. Clearly the Fed is not doing well if its credibility is noticeably strained this early in the battle even with those who usually see Fed failures last because they usually just bubble out of their collective mouths whatever they are spoon-Fed.

The moves come as investors are increasingly worried about a potential economic slowdown. Several key pieces of economic data fell short of forecasts this week, ranging from May retail sales to housing starts, and the Federal Reserve raised its benchmark interest rate by the most since since 1994.

“This week was brutal. … Let me tell you, we’re in a recession,†Wharton Business School professor Jeremy Siegel said Thursday on CNBC’s “Closing Bell: Overtime.†“It’s a mild recession. It’s not an official recession by the NBER, certainly not yet, but this first half is negative GDP growth, and it’s ending on a slide.â€

The S&P 500 is down 6% for the week, which would be its worst weekly performance since March 2020.... The Dow fell below 30,000 for the first time since January 2021.... The tech-heavy Nasdaq Composite has been hit even harder, and is down 6.1% for the week.

Looking beyond the week to the entire first half of the year, Zero Hedge said,

The Mood On Wall Street Has Never Been More Apocalyptic

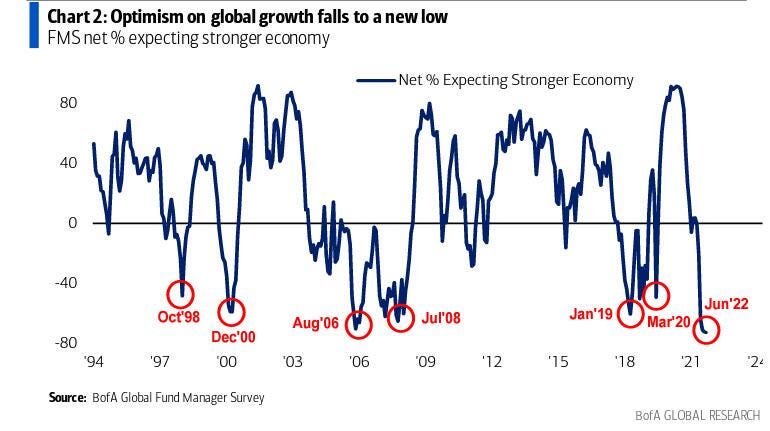

When [we] look at the latest BofA Fund Manager Survey, we find that the mood on Wall Street has never been [more] catastrophic, dire, apocalyptic, etc.. and 30 days later we find that said mood has turned even worse.... A quick look at the responses to Mike Hartnett's questions by the 300 panelists who manage $834BN in AUM suggests that one should not walk next to tall building[s] on Wall Street.

Indeed, the risk of falling bodies among market managers has never been more frightful nor the mood more sour in the history of mood rating with a likely trajectory out Wall Street Windows that looks like the last leg of this graph:

The typical body's flight path appears to have bounced at street level and then rolled into a manhole.

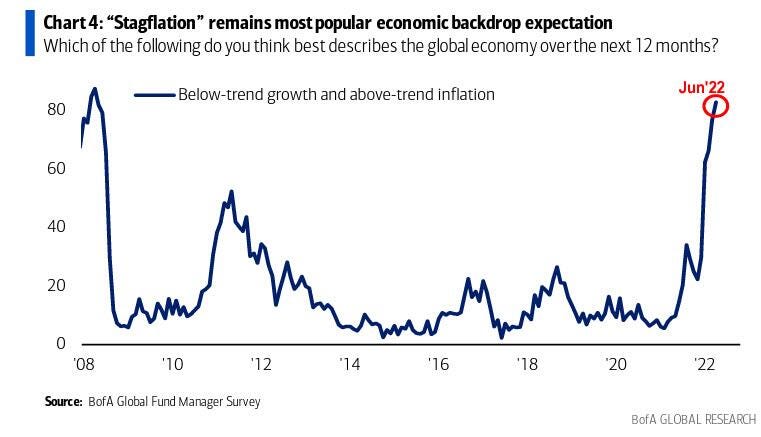

As for who market managers are betting on -- Fed or Fedflation -- it's pretty clear all bets are on the same side of the boat:

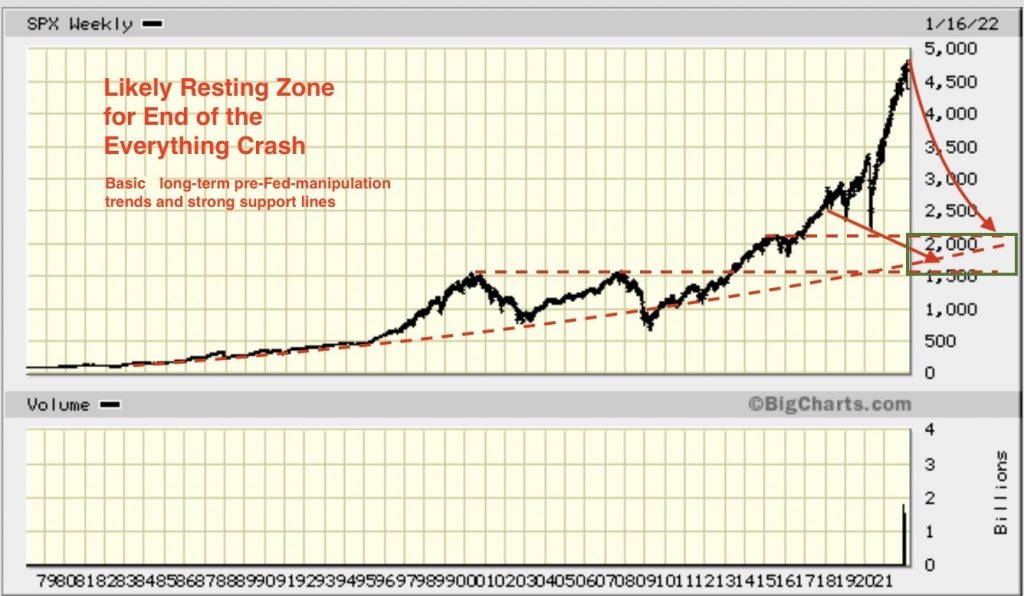

However, if you were to take the extremely negative mood right now as a contrarian indicator that it is time to jump in and buy stocks cheap, you would be very wrong. Here is the level I wrote months ago I anticipate to see as a likely final-resting place for this market, triangulating using several extreme trends:

Somewhere in that coffin-shaped box. That was the graph I made for a Patron Post at the start of the year, but I expected the market to take months to get there:

I don't think it will get there in one shot. I've never suggested that....

One of the most insane things I've heard recently is that this market still needs to form a blow-off top. Really? What on earth do you call that final rise compared to ALL other rises before it if that is not peak market-mania melt-up? That comment came after I shared that graph and became a self-parody, providing its own evidence of how irrationally exuberant investors have become.

"The Everything Bubble Bust Pt. 1: How Far Will the Stock Avalanche Fall?"

Clearly, the insane thinking that claimed back in January that the market still needed to form a blow-off top gave way completely to reality and is its own evidence of how deep in denial irrational exuberance becomes. It is stunning to think anyone could be starting to tumble off that precarious summit and fail to realize they have just experienced the greatest blow-off rush in the history of the world! The peak shown in that graph was, in fact, the S&P's final peak before plunging for months into the bear market that it, at long last, reached last week!

Because my position has always been that the crash that would begin along with a recession at the start of the year would play out like the dot-com bust, which took more than two years to find its bottom, there is a lot of breakage left to come. The bond market is just getting into the kind of crash territory that will soon become systemic and start bringing down a landslide of zombie corporations that don't even make enough cash flow to cover their debt under rapidly rising junk-bond yields. Until that happens, the stock market probably won't even experience its first Lehman moment in the present crash. Housing has only begun to slide; and, while stocks have been falling for more than half a year now, you can see they have only fallen about half the distance I expect them to eventually go.

Here is how insane market euphoria felt to me last January when I received that comment:

The longest, steepest, and (because it is happening during a global pandemic) most insane rise the market has ever made supposedly shows no sign of a melt-up yet??? Just put my head in a vice and squeeze it. That is by far the biggest rocket ride anyone has ever seen, and it has been happening while the entire underside of the market corroded away to where more than fifty percent of NASDAQ stocks are now in their own bear markets, leaving no support to the outer skin of the market that remains inflated. (Yet, there are still !@#$ saying, "Buy the dip.")

Permabulls felt secure enough at the S&P's top back in January to scorn those who warned them, having no concept of the slope to come, because they continued to believe Papa Powell would rush back in to save them as he always has. They should have known, based on inflation, that was not even possible. The Fed set up these expectations that are hard to break, however, and now it must break them, creating undoubtedly more feelings of distrust as it does so among those who thought they could do a backward faith-fall into Father Fed's ever-lovin' arms based on past experience, only to have the Fed walk away.

Last week, Powell made it clear he is still nowhere close to rushing in, even though the Nasdaq and Russell were in bear markets with the S&P sitting on the edge of the bear's pit. The S&P joined the other indices down in the pit a day after Powell spoke to let the world know he fully intends another likely 0.75% interest hike at the Fed's next meeting and will continue on that path until the Fed sees inflation move meaningfully lower.

The great Fed job fake

Bear in mind, the Fed just hiked interest rates the most it has in almost thirty years. And it plans to do that much again in about a month. And it is doing it when we are already sliding into a recession, which the Fed neither sees nor believes in any more than it saw or believed in inflation.

Even now, almost the entire financial media thinks they are being bold when they make such frivolous pronouncements as "We are heading for a recession as early as 2023" even as they tell us that the last quarter's glaring GDP fail was a one-off, in spite of the fact that the Fed's own GDPNow is finally saying, "No it isn't!"

The Fed's GDPNow forecast, by the way, has tended to run a little toward the optimistic side, even though it fairly consistently runs below the consensus of industry economists, but we all know mainstream economists are the worst people in the world at predicting recessions because they are too timid. They're caught up in their own academic groupthink, afraid to predict bad news with confidence and then be wrong among their colleagues because they are afraid someone will call them a "permabear."

Why? Because that is the go-to response whenever anyone predicts a major downturn that the majority doesn't wish to see coming. So, the mainstream economists are actually raising their bets, as you can see in the Atlanta Fed's GDPNow graph toward the blue-sky zone above 3% growth, hanging on to their delirious beliefs that the economy is swimmingly strong because jobs are strong.

Jobs are, in fact, not strong at all. That is a mirage created by the simple fact that there are a lot of people who quit the labor force with no intention of coming back if they can possibly avoid it. Really, the jobs market is horribly, horribly broken because it is incapable of supplying the level of workers necessary to build production back to where we need it to be if we are going to end the supply shortages that are contributing so much to inflation -- something the Fed can do nothing about. While the Fed created the too-much-money side of the problem, it did not create the supply shortages that emerged from supply-chain destruction under trade wars, followed by Covid lockdowns, followed by the widest sanctions in world history.

Pandemic-era checks rewired how these Americans see money: ‘Stimulus changed how I think about what’s possible’

For Denise Diaz, the benefits of pandemic-era stimulus checks went beyond everyday dollars and cents. They rewired how she thinks about money.....

The checks (and other federal funds) are at the epicenter of a debate as to whether and to what extent the financial assistance helped fuel inflation, which is running at its hottest in about 40 years....

Consequently, Diaz, 41, feels more financially stable than during any other period of her adulthood. The financial buffer and associated peace of mind also changed her psychology....“The stimulus changed how I think about what’s possible, personal spending habits and the way in which I manage my money,†she said.

The article goes on to explain how people used stimulus money in good part to pay down debts and how people during the time off work that came from forced lockdowns learned they could trim their budgets to where one member of the household would no longer need to work. Many liberated themselves by paying down debt. These workers, sick of the rat race, will only return when the economic ruin of their nation forces them to return. At the rate many are now piling debt back up, that day is sure to come, but probably not before the world lies in economic ruin because too many people are still consuming when matched up against the number who are willing to produce. For right now though, debt freedom has brought a form of jubilee that has set them free.

That is not a healthy job market, and economists who say that, including the Fed (which says it all the time), are thinking with their headlines, not with their heads. It is a badly broken job market that cannot deliver the supply that is needed to break the back of inflation until inflation breaks everything, including them, and burns itself out. Nothing causes prices to rise so easily as scarcity. (And, may God forbid the Fed goes back to money printing because if you try to solve a shortage problem with money printing, you go up in the flames of hyperinflation along with your money.)

When people feel that kind of liberation, it takes a lot more money to entice them back to work. And that is the self-perpetuating cycle of inflation mentioned above. People demand significant raises, driving up the cost of the goods and services they produce.

So, no, the economy is not strong and neither is the job market. The economy has too few workers to do the work that needs to be done to meet routine supply requirements, and the only way to entice workers back under the additional inflation yet to come will be by offering significant raises to offset that inflation, which creates a vicious circle, rather than a virtuous circle: