The Whacky Wonderland of Sovereign Debtors and their Central Banksters

Before delving further into the schemes of central banksters for saving their debt-addicted sovereigns from monsters the banksters created in their own laboratories, I thought it might be helpful to present an overview of just how wild their brave new world has become.

The spread of negative-yielding debt has raised profound questions about the extraordinary lengths central banks have gone to in a bid to revive the economy over the past decade. At the same time, bond markets’ journey through the looking glass has befuddled many investors. “Free money — it’s sort of an insane concept,†said David Hoffman, a bond portfolio manager at Brandywine Global in Philadelphia. “Having grown up in a very different world it’s challenging to navigate this.â€

Indeed. So, on with an overview of what has become a shrieking fun house of monsters and mirrors.

Everyone has a sovereign-debt monster

In just the past year, it has become popular mainstream belief, broadly accepted by economists, that there is essentially no limit to how much debt national governments can take on, and the United State's current debt expansion at an anticipated rate of $1.2 trillion dollars in fiscal 2020 will blow up to $1.7 trillion if we wind up in a recession:

In planning for next U.S. recession, economists say, don’t fret about debt

Economists are divided about when the next U.S. recession will arrive, but they largely agree on this: the country will need to fight it with a massive fiscal program, and be ready to swallow deficits that may eclipse the trillion-dollar shortfall run by the Trump administration this year.

Past discussion has focused on the Federal Reserve as the more powerful first responder, and how rising U.S. debt carries its own risks. Now talks are about how much money ought to be spent and where it should go - whether to infrastructure, programs to counter climate change or direct payments to households.

In the next recession, the United States should contemplate “a pretty generous package,†of perhaps as much as $1.7 trillion, double the amount approved for recession fighting in early 2009 during a steep downturn, Karen Dynan, a former Fed and Treasury official now at the Peterson Institute for International Economics, said in a recent discussion of the world economic outlook.

“We do have fiscal space,†she said.

This pro-debt attitude finds broad agreement among corporate economists, academics, think tank analysts, and private forecasters alike, and not just in the United States.

With everyone in the decision-making corridors of all the governments in this world hell-bent on supercharged debt expansion, central banks will be increasing pressed to finance those debts, just as the Federal Reserve and the European Central Bank recently sprinted back into doing after a brief hiatus (with the Fed being the only bank that ever dared to try -- quite unsuccessfully -- to roll back its previous assumption of government debt.

Until now, the Fed has maintained that it was not monetizing the US debt on the basis that it was only temporarily buying that debt and only for reasons of affecting long-term interest rates. Now that it has moved to a position of buying and holding debt permanently, it (and all other central banks doing the same thing) is monetizing the debt.

Monetizing a debt that is now set to grow forever at a rate of, at least, $1.2 trillion a year has to impact monetary policy. It surely creates massive back pressure for some sort of big change because the more central banks have to soak up that debt, the faster central banks have to print money in order monetize it all now that they have no intention of ever rolling that money off of their balance sheets.

Consider the size of this monster: Total US public debt (the debt the government owes to entities outside itself) is now rising more each year than the total debt the US had accumulated from its founding to the year before Ronald Reagan's re-election and the Deficit Reduction Act of 1984. We can now see how well that governmental dream worked as deficits more than doubled their rate of growth under Reagan from that date forward and then expanded exponentially under every president from 2001 to the present:

Here is the key to assessing this mountainous vault of debt: central banks all over the world are now forced to soak up all that new annual government debt issuance so that over a trillion dollars of new bond issuances (or whatever amount applies for any given nation) plus all the debt refinancing that has to happen each year so that the exploding debt doesn't push interest rates on those debts through the roof. Even if central banks didn't want to finance their government's profligacy, they would have to just to protect the economies they are partially responsible for shepherding because other interest rates paid by citizens are in various ways benchmarked off these government rates. Economies all over the world would choke to death if central banks did not take on this ever greater government debt issuance.

As that mountain of debt looms higher, there is more incentive for central banks to drive the interest rates negative in order to keep interest alone from suffocating their sovereigns. My point is never to suggest this is how central banks should roll, but to say that the path they are on requires they continue to soak up government debt in ever larger circles, or it will implode due to creating its own interest problems. (It should have never happened in the first place, but it has served bankers and their profligate governments well for as long as the CBs can keep all the plates spinning.)

Don't be so negative!

Fed Chair Jerome Powell has said the Fed will never go negative on interest rates. In response to President Trump's response to go negative, Powell said in September,

Negative interest rates is something that we looked at during the financial crisis and chose not to do. We chose to—after we got to the effective lower bound, we chose to do a lot of aggressive forward guidance and also large-scale asset purchases, and those were the two unconventional monetary policy tools that we used extensively. We feel that they worked fairly well. We did not use negative rates. And I think if we were to find ourselves at some future date again at the effective lower bound—again, not something we are expecting—then I think we would look at using large-scale asset purchases and forward guidance. I do not think we’d be looking at using negative rates. I just don’t think those will be at the top of our list.

That, however, is empty talk as evidenced immediately by Powell's twice saying "I do not think we would ..." and by his qualifying it the second time when he said he doesn't think it will be at the top of the Fed's list. In other words, it will still be on the list. I think the next situation will be one that requires bigger tools. By then the Fed should also have finally become apprised of the obvious, which is that their old tools did not create anything durable. So, Powell's stance on going negative is wide open to shifting.

With that said, the Federal Reserve doesn't have the need to go negative that other central banks have had -- particularly the ECB. Keep in mind that when the ECB creates policy that is intended to keep interest rates in places like Spain, Italy, and Greece at manageable levels, that means interest rates in much healthier economies like Germany's may go negative because interest between countries is relative to risk and governed by one central bank, even though the countries have very different needs. So, if German interest is near the zero bound, and the ECB tries to effect a 2% lower rate for Italy, where is Germany's rate going to go but south of the zero border?

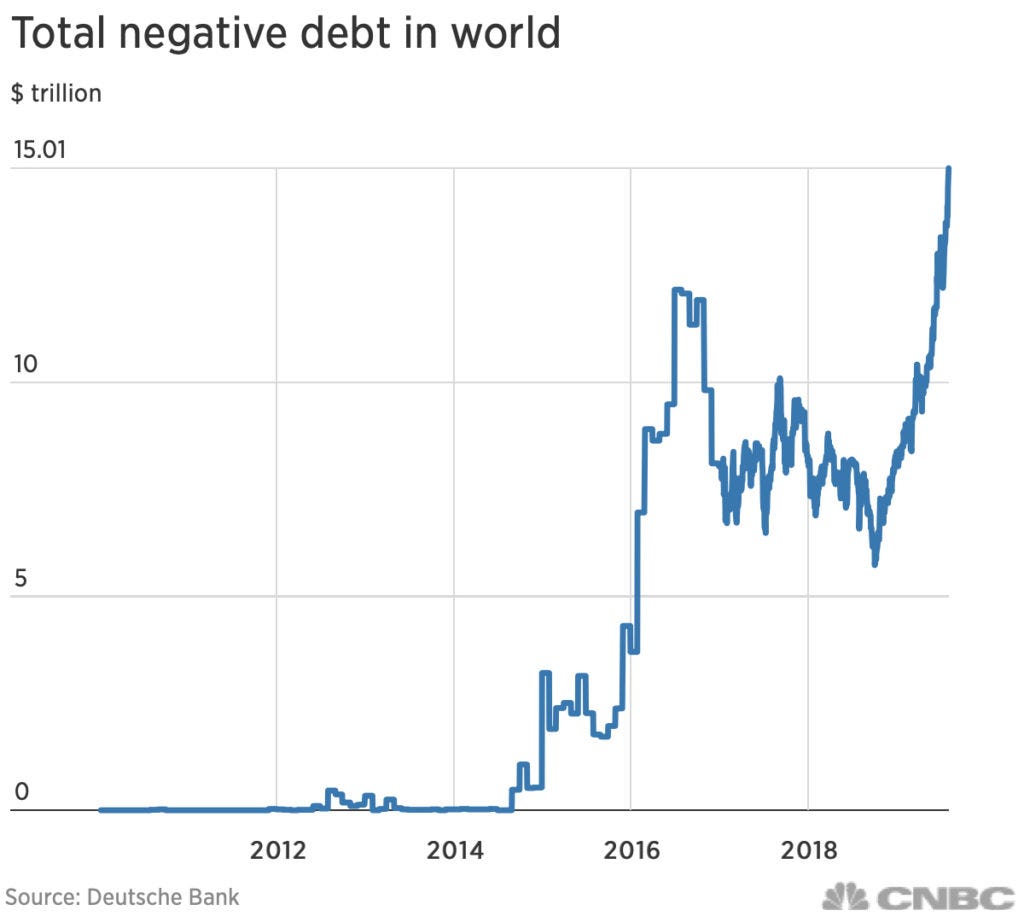

Central banks overall, have been pressed by their flailing economies to continue to expand polices that have taken over $17 trillion of sovereign debt into negative territory. That is more than 25% of the global government bond market that is priced at negative yields, an amount that has almost tripled in just one year:

You can see this is a rampaging problem that has no historic parallel. As central banks are pressed to perpetuate their economic recovery solutions with more extreme measures of stimulus, their new answers are creating this massive distortion in interest, which in prior years was virtually non-existent. That presses them further and harder to invent answers for problems that are exploding into the stratosphere.

While Powell would love to blame Trump's trade wars, you can see in the graph above that the monster was born before Trump even came along on the political scene. It is a problem created by central banksters.

What could look more like their plate spinning has gone out of control than the graph above? By stopping their quantitative easing and interest cuts or even reversing them, they got back some control in late 2017 and early 2018, but that created a severe liquidity crisis, pressing them right back into QE and interest cuts, which shot negative debt out of orbit after that.

Now the pain of letting what they have created correct is almost beyond contemplating.

Here is how the major economic realms of the world stack up to each other in this race to the bottom (using their ten-year bonds for the example):

With the US and China being the major holdouts, what happens if their trade war devolves into a full-on currency war? That's just one tiny tentacle of the sovereign-debt monster that now enwraps the earth.

With all of that debt spawned into Wonderland in order to provide further economic stimulus, the global economy is still grinding to a halt, so do you think central banks and their pocket politicians have painted themselves into a corner at this juncture? Given such apparent loss of control and the rush to invent solutions to the problems created by each solution, how far away can a global banking reset be?

At this point, it doesn't even matter if the Fed wants to take interest below the zero bound. Bond markets are global, and the global market is taking interest there. The US government, as any other government, is not going to be pressed to pay higher interest than it has to. The Fed is really just chasing interest where global markets are taking it. The best it can do at this point is pretend to have control in order to try to hold its currency stable.

Where is the pressure for the US government to keep paying 1-2% on bonds when the US is more stable than other national debt while other national debt is far below that? How can the Fed keep holding US debt interest up there even if it wants to? Granted, the US is issuing record debt, but so is everyone else.

It's a little hard to understand what is levitating US yields to such a high level above nations that have much riskier debt. The US now pays substantially higher interest than Italy (currently 1.75% on the US 10yr v 1.04% on Italian 10yr bonds.) Compare that to Spain which only pays 0.26% to fund its debt. Welcome to the oversized, upside-down world of Wonderland!

![By Germán Torreblanca (Own work) [CC BY-SA 4.0 (https://creativecommons.org/licenses/by-sa/4.0)], via Wikimedia Commons](https://substackcdn.com/image/fetch/$s_!w0BP!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fe1709dde-936e-492e-88b9-89163489262b_400x600.jpeg "By Germán Torreblanca (Own work) [CC BY-SA 4.0 (https://creativecommons.org/licenses/by-sa/4.0)], via Wikimedia Commons")

In fact, it looks like almost everyone pays less interest on their sovereign debts now than the US:

Even Italy -- not included in that chart but priced far below the US -- looks overpriced in that bottom-feeding company! Yet, Italy's debt is so great that it is third-largest in the world to the US and Japan! Even Greece, in all of its years of fiscal dissipation and with its aged sclerotic arteries, sports a shinier more youthful interest rate than the US at 1.32% for its ten-year (at the time of drafting this article). It's a good gig if you can get it!

As a result of all this, look at where the US dollar hangs out:

Clearly, beside itself and no one else.

Of all these countries, which one is the most over its eyeballs with the exception of Japan, which is literally on a scale of its own?

The US, of course.

The worldwide marathon downhill could become quite the pileup at that bottom:

If anyone can figure out where the bottom is now that the zero bound seems to no longer apply. I guess we'll know by the wreckage when we get there!

Why do people buy this garbage?

You may wonder why people and institutions are racing to buy all of this crappy quality, negative-yielding debt. The small answer in better nations like Germany is safe-keeping in uncertain economies. Investors are willing to pay a small storage fee to have their government's hold large amounts of money for them.

The big answer, however, is that negative bonds are highly profitable! Ironically, the inverted Ponzi scheme of negative-interest speculation can deliver huge profits on bonds SO LONG AS interest keeps going down (and the pressures noted above indicate it will go down until the nations, themselves, crash in a conglomerated heap, at which point all bets are off for everyone). So long as central banks are hell-bent on banshee bailouts of failing economies, a bad economy looks like a good bet for lower interest rates to come!

Here is where we find one of the quirks brought on by the large increase in the amount of outstanding negative-yielding debt: most bond investors have actually done quite well for themselves in recent years. Investors who bought Germany’s 10-year note in July 2017, which carried what appeared then to be an unacceptably low coupon of 0.50 percent, are sitting on a total return of 12 percent as the note they bought for €99.10 now trades at €109.90, for a yield of -0.71 percent (bond prices move inversely with yields). Not bad for a world of negative rates.

The thing to understand is that no one buying these bonds is making interest payments to governments to hold their money. What they are doing is paying a premium on the price of the bond -- buying, say, a $100 bond for $102. Upon maturity, the bond will be worth less than they paid for it, but the buyers have no intention of holding it to maturity. They are betting interest rates will keep diving so they can sell it at a better price in the bond market sometime later to someone else willing to bet interest rates/yields will decline further still.

If you do that on secure US bonds that are, at least, positive in payoff at maturity, you can't lose (unless the US government defaults on the bond, in which case all bets are off for everything) because you can, at least hold a positive bond to maturity and still make money if interest rates don't go down. If you do it on one where the premium means payout at maturity will be less than you paid, your losses are still, at least, limited down the road to that negative differential, but you are taking that risk in hopes of making a large speculative gain. (The gains on long-term declining bond prices are exponentially inverse to their yield actions.) We're on a race now to find out where the final tiers of sucker buyers are who have so little time left on the bond they buy to where they have to take what it pays out at maturity at a loss.

In usual central-bankster understatement, the Bank for International Settlements (BIS), known as the central bankers' central bank, has called this new development "vaguely troubling." But what do you expect them to do -- hit the alarm button and yell that there is a disaster on our doorstep?

“There is something vaguely troubling when the unthinkable becomes routine,†said the head of the BIS’s Monetary and Economic Department, Claudio Borio.

Well, OK, technically I guess they said it is "unthinkable" but now routine and that is "vaguely troubling."

AEI, the American Enterprise Institute, is a public policy think tank, and they think differently:

Severe economic recessions generally have their roots in excessive debt levels and financial market mispricing.

Well, who could be expected to see anything troubling here then?

Global economic policymakers would be ignoring those early warning signs at their peril. This is particularly the case considering how large the European economy is and how vulnerable its banking system remains to financial market turbulence. The most troubling sign of financial market mispricing is the fact that around one half of European bonds now offer negative interest rates.

Good thing, then, the BIS has put this group on watch that their situation is "vaguely troubling." Sounds like they have this all under control. Don't worry. Move along.

An extreme example of this phenomenon is the fact that the whole of the German sovereign yield curve, including 30-year bonds, is now in negative territory. It would seem that something very strange is going on when investors have to pay the German government around 0.75 percent a year for the privilege of lending it money for a 10-year period.

What could possibly go wrong with turning an entire realm of national debt into a speculatively priced Ponzi scheme? Hmm. Maybe the nations of Europe are all banking on stock market crashes across the face of Europe to send the final tiers of desperately fleeing investors into Europe's many sovereign bonds in a final Hail Mary that drives yields down ever further for the sake those who hit the exit gates in time?

So Europe gets a little repricing! Big deal!

No wonder high-yield/high-risk corporate bonds in Europe are also getting negative interest. Yes, corporate junk bonds are now able to attract investors to pay the junkie to help him finance his debt. What could go wrong there?

Well, at least, some people at the power panels of finance find all of this vaguely troubling and are flashing the lights.

Where do bottom feeders go when there is no bottom?

The bottom may be nearing, but who can really tell with no historic precedent to gauge for perspective?

In Switzerland, Denmark, and some other countries, negative yields are used as blatant currency manipulation ... but ... there is a price to pay - as we can see from the economic doldrums and the banking fiasco in Europe and Japan. Negative yields have been another blow for the European and Japanese banks hobbling from crisis to crisis, their shares wobbling along multi-decade lows. Negative yields are the final blow for pension and retirement systems. Negative yields distort the pricing of risk, and therefore distort the cost of capital and lead to business decisions that would otherwise be idiotic waste and malinvestment.

No one is getting any lift anymore from all of this QE. A lot of plates are wobbling badly, but we have no idea when they will fall. These plates are platters that serve up entire nations. The central banks of these nations are racing madly now for replacement strategies to their dinosaur systems; but nothing I've read gives me any confidence that their replacement strategies will be any better than the monsters they have already created. Nothing gives me any confidence they even begin to fathom what they have created. They are mad doctors, creating viruses to destroy the last viruses they created to cure the world's economic cancers.

And we're going to trust them (as a nation)?

I think so.

Because that is what we do ... over and over.

It is what we have always done.

I'd like to think differently, but I have no reason to believe otherwise. Best, in that case, as an individual, to have some idea of what these viral Mad Hatters are concocting next. I'll get on to that shortly. (I have jury duty for the upcoming week, so depending on what kind of duty I pull and how long the trial runs, I may be a little delayed.)