The Apple Cart is About to Tip

Rising energy prices will raise inflation and tip us into recession

When I stated the following back in January …

What I can say with certainty is that inflation will not back down to where the Fed believes it has won the inflationary war as easily as stock investors keep believing. This war will outlive expectations just like the Ukraine war that was supposed to be over in a month and still has no end in sight…. Inflation has that kind of fight in it that many in the stock and bond markets are not expecting, and it has empowerment behind it, too.

… I also wrote that a major driver in the Fed’s ongoing saga with inflation would be a rise in oil prices:

Fuel prices are back on the rise…. That doesn’t mean much if crude prices do not continue to rise; however, there are reasons to think they will, and gasoline and diesel, of course, drive the price of just about everything because they are involved in the transport of all resources and all finished products. So, they are a major leading indicator of future price rises in all goods and services IF the rise in crude prices continues.

From there, I laid out several reasons why crude oil prices were likely to rise this year, making the Fed’s inflation battle harder to win, particularly noting the combined effects of European crude price caps on Russian oil and Russia’s likely cutback in oil supply.

I wrongly noted the possibility believed by nearly all back then of China’s reopening rebound also contributing to the rise in oil. That certainly didn’t play out, but I was quick to voice against the commentary flow that the rebound was not happening and not likely to happen as that became evident to me early on. That said, I haven’t seen the failed rebound as mitigating the rise of oil prices much — for now anyway — because China’s lack of addition to the price of oil has been offset by OPEC’s (particularly Saudi Arabia’s) choice to cut back production correspondingly.

Having laid out a variety of contributing factors to the rise in oil prices I was projecting, I concluded,

Here is the important takeaway: One of the biggest factors that took down consumer price inflation in recent months was falling energy prices, but there is plenty of reason to think those won’t hold, so they could easily become one of the biggest factors driving inflation back up. And it is not just the “energy” component that will go back up in that case, but all components that use energy in their production and transport, which means everything.

Inflation was far from beaten in the last report, since it all hinged on volatile energy taking the overall numbers down, and the stock market was foolish to take that report as a sign that the Fed is winning its war. The Fed has absolutely no control over what happens in energy prices. It is hoping its high interest will cause enough economic destruction to bring down demand for fuel, but the question is will the demand drop as much as available supply may drop? If not, then prices will rise until demand and supply find their equilibrium. While the Fed can hope to have some impact on energy demand, it has zero control on the supply side, which is where all the problems are forming.

So, there is still lots of room here for CPI to rise if energy makes a sustained rise, and there are plenty of reasons to think that is likely.”

Now, here we stand with one story today reporting the huge gain in oil prices in recent months as they press toward $90 per barrel:

The Bloomberg Dollar Spot Index jumped to a six-month high this week as crude oil futures rose toward $90 a barrel, a rally of about 30% from this year’s low reached in March. The index is now on track for its longest streak of weekly gains since its inception, mainly at the expense of the yen and euro. Its correlation with oil prices reached … the highest in nine months.

Higher oil prices might also fuel concern that Europe faces stagflation — a combination of weak economic activity and high consumer-price growth….

“Europe is well into the danger zone and Japan is getting there,” said Timothy Graf, head of EMEA macro strategy at State Street, about the economic impact of higher oil prices. He adds crude prices only start to dent the US economy around $120 a barrel. “US inflation expectations do not look in any danger of getting unanchored.”

However, the danger for inflation and the economy due to overall inflation is not contrained to Europe, though the US benefits some from its positive trade balance in oil. As Zero Hedge reported today,

Rising Oil Prices Might Be What Tips US Into Recession

Household spending has kept the US economy afloat, but as growth slows a continued rise in oil and gas prices is poised to push personal consumption expenditure (PCE) lower and thus trigger a near-term recession - with stocks and bonds unpriced for such an outcome.

It is tempting to start with thanking Joe Biden for his infamous fist bump with the Saudi Prince when he begged him to lower the price of oil to help the US out, except that the rise in the price of oil was seen as likely here pre-fist-bump. Still, some credit where credit is due in a contrarian sort of way.

Once again it has been the redoubtable consumer that has thus far kept a recession at bay. However, Bloomberg Economics (BBE) pointed out in a recent article that negative household sentiment – in confluence with other drivers of household spending – suggests that we should already be in a recession.

Sounds like a point I would be making on just about any given day, and in my “Deeper Dive” this weekend I’ll be going into why I think Goldman was full of Sachs of something other than gold when it revised its recession predictions backward to neutral. (To that end, there is another article in the news today by an investment advisor, Lance Roberts of Real Investment Advice, who I think has done a solid job over the years, showing how, whenever GDP and GDI have diverged like they are now (as I wrote about on Tuesday), GDI has been the right party, aligning nine times out of ten during those divergences with a recession. I’ll let him do the explaining in the article below in order to stay here on today’s topic, not this past Tuesday’s. Just wanted to point you in that direction.)

The writer of ZH’s article, Simon White, a Bloomberg macro strategist, states that he prefers the University of Michigan’s Consumer Sentiment Index over the other prevailing model — the Conference Board’s Consumer Confidence Index — because of its much higher reliance on energy prices and their strong impact on consumer confidence. A change in confidence, of course, causes the consumers in our consumer-driven economy to pull back, tipping us into recession. That is why we track it.

By some measures (such as GDP), we have stayed out of recession because consumers still had a lot of free Fed float in the banks, which is coming to an end in October. That is when the Fed says the majority of consumers will have finally exhausted the savings they accumulated from all that Fed inflationary money-pumping during the Covid era (as distributed in large doses by both the Trump and Biden governments … especially to the rich, but also to the average worker to a smaller but still significant degree) that have driven inflation.

He also notes that the Conference Board’s index relies heavily on the strength of the labor market, which, as my regular readers know, is a measure I firmly believe is faulty because the labor market is not strong; it is weak due to the anomalous situation of being a badly shrunken labor pool that has kind of recovered, except that it remains far below its former trend line, as laid out clearly in another recent “Deeper Dive.” (See: “The Nation is on Fire.”)

Note that the individual laborer’s bargaining position is VERY strong, but that is because the completion among laborers is very weak due to their low numbers in the total labor pool, making it a worker’s market, not a businessman’s market. (Just as few buyers in a housing market tend to make a buyer’s market because they are not bidding each other up.) The market is weak in the sense of its ability to produce and rise to demand, which is recessionary.

Here is where I am going with this: White shows a large divergence between the Michigan index, which leans more upon energy prices and their effects, and the Conference Board’s index, which leans more upon traditional labor-market metrics, and the difference looks just like the divergence between Gross Domestic Income and Gross Domestic Product that I just wrote about on Tuesday. (See: “The Recession is Here!” where I wrote that I’d trust GDI (as we see today Lance Robert’s also leans to trusting) over GDP when there is this kind of divergence … as a measure of what the economy is truly doing.

Likewise, I’d trust, as does White, the Michigan index that leans on what I predicted for oil prices versus the index that leans on the extremely popular misconception that the labor market is strong in the sense of showing a vibrant and resilient economy (one with high demand pressing us to higher production):

The divergence between the two likely comes from the Michigan’s greater emphasis on frequent expenditures and business conditions, while the Conference Board’s index is more focused on the jobs market. As an employee, the jobs market has looked pretty good, boosting the Conference Board’s index, while the Michigan survey is more influenced by rising prices and conditions for small-business holders, which have been less rosy.

“As and employee.” Exactly. The individual laborer is strengthen when labor competition is weakened due to a severe shortage of laborers. These “prices and conditions,” of course, are always hugely contingent upon the cost of energy that goes into production and transportation of materials and eventual products, which is where White is going with that:

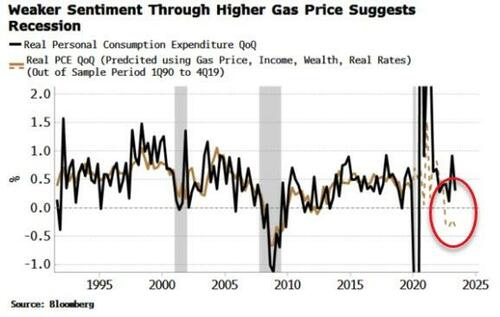

The Michigan survey is in fact very sensitive to gas prices. In the model, I added the average gas price to the model’s original inputs (i.e. ex Michigan). Doing so also improves the model’s fit, and as the chart below shows, implies notably weaker, and negative, PCE growth – and therefore an economy that would likely already be in a recession.

My claim has been we really already are in a recession of sorts, which shows clearly in GDI, which normally tracks exactly with GDP (and slightly leads it), and not in GDP, which is the party that has strayed in this normally tight courtship, as Roberts explains in his own article.

In the graph below, the barely visible dotted line shows where the Michigan Index would be if energy prices are fully factored in based on where they have gone:

In recession territory.

That is where sentiment would be if gas prices had been as high as they now are and as they are likely to remain.

Tailwinds remain for oil, and therefore the nascent recent rise in gas prices is poised to continue as well. That could be the final straw which unseats the US consumer and tips the US into a recession.

The point being that, as gas prices rise, consumer sentiment can quickly change. When that happens right as the last of consumer savings becomes largely depleted in October at a time when credit has nearly maxed out and becomes hugely pricey because of Fed interest hikes, then the economy can quickly make that shift into an unmistakeable recession. When consumers stop buying out of their remaining savings and petroleum-based energy prices press them to cut other budget areas to meet their heating and commuting needs, the nascent recession will open up beneath our feet.

It is already there in so many ways, masked by the gross misunderstanding of labor. An increase in CPI, correspondent with rising energy prices that effect the price of everything, will really push the consumer hard and turn not just the sentiment of consumers but the sentiment of stock investors and bond investors as well when they see those CPI number start to rise again … just like the PCE inflation numbers already are doing.

The Fed’s apple cart is going to tip over just as we get to that cider time of year.