THE DEEPER DIVE: Stop Feeding the Insanity and Let it End

Inflation is up and down due to tariffs and manipulation, particularly fueled by years of Fed manipulation, and now we're turning to government ownership and direct control of businesses!

The first news on inflation this week sounded good for America, terrible for my predictions. I should be glad to be so wrong, I guess. The news sent the stock market soaring again as it became known that the scorching-hot producer price inflation reported last month had cooled down to practically nothing. Of course, the market mostly rose because tame news on inflation all but assured investors of freer Fed money flows into stocks. With inflation cooling off, the Fed could now afford to pump up old bubbles that were at risk of deflating. Above all else, keep the bubbles going!

What happened was the PPI (Producer Price Index) actually fell 0.1% this month after its huge rise last month (See: “THE DEEPER DIVE: There is Inflation, and then there is INFLATION!”)

CNBC reported,

The report serves as a positive sign heading into Thursday’s more closely watched consumer price index reading that inflation in the U.S. economy is cooling.

Well, so much for me, then! If that is the case, you should stop reading here because you're getting a bum steer. Inflation is not rising, but is “cooling.”

Before you run off mad at me for bad info, however, note that they said it was a positive sign for what was about to come in CPI.

That didn’t happen, so MAYBE they were the bad steer, aiming too optimistic as usual based on a glint in the bottom of the gold pan that may have been nothing more than a fleck of gold-colored foil that fell in the river. Maybe the dip in PPI was a glint of fake gold on the inflation front.

Economists expect the CPI report to show monthly increases of 0.3%, according to Dow Jones. This includes the headline index as well as the core reading that excludes volatile food and energy prices.

CPI fails to land

So much for Powell making a soft landing. No landing has been made yet, and CNBC had to report later in the week that CPI came in a touch hotter than expected, and a slight rise was already epected:

Prices consumers pay for a variety of goods and services moved higher than expected in August while jobless claims accelerated, providing challenging economic signals for the Federal Reserve before its meeting next week.

We call that “stagflation.” It’s not a good thing. It is the squished gap between a rock and a hard place for the Fed. It doesn’t leave much room to maneuver, and it certainly is not a soft landing.

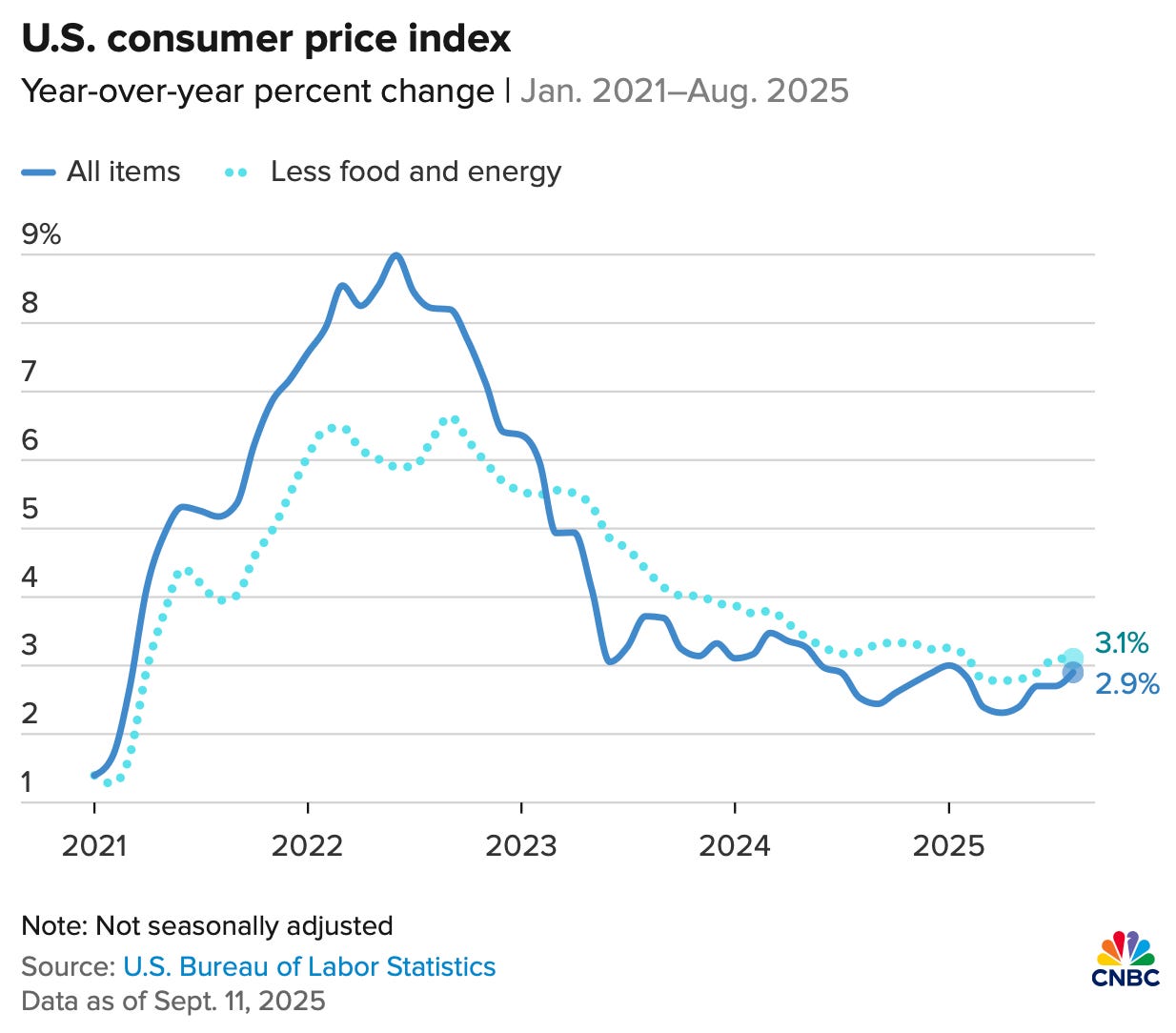

The consumer price index posted a seasonally adjusted 0.4% increase for the month, the biggest gain since January, putting the annual inflation rate at 2.9%, up 0.2 percentage point from the prior month and the highest reading since January.

So, not a huge jump, but the worst this year, and what it means from my point of view in tracking all of this is that the producer price inflation that I wrote about in that Deeper Dive last month is now squeezing its way into consumer price increases as expected.

As for that blip down in PPI, it’s not that surprising to see a momentary cool-down in the latest month reported after a scorching-hot read the month before. Think of it as PPI having “gotten it out of its system” for a bit. Like Kilauea Volcano, which has had large eruptions many times, only to cool back down for a bit after the huge built-up pressure was relieved and then spew more fountains of lava a month later. The eruption continues.

As I’ve said many times, a single cool-down or a single turn in economics does not a new trend make. There are no straight lines for long in economics. There are always little blips along the way in the opposite direction. So, we’ll have to see if the rising trend in PPI continues in order to know if CPI, which is downstream from PPI, will see any pressure relief.

This wasn’t a big move in CPI, and it doesn’t establish a new trend for CPI, which has been generally downward until now, either:

However, it is close to reversing the long downtrend in CPI, which has nudged up and up again but not broken above any of its highest readings in the past year.

Will it be enough to cool Powell off on his expressed willingness to cut rates at the upcoming FOMC meeting? I don’t think so. It was, after all, just a blip in the wrong direction, and Powell seemed more concerned about the declining economy, and we know how the Fed loves to reinflate bubbles whenever it can. Still, they hate inflation making them look like public enemy number one; and they also know Trump will place the blame for the fall of the economy around their neck again and again.

“Today’s CPI report has been trumped by the jobless claims report,” wrote Seema Shah, chief global strategist at Principal Asset Management. “While the CPI report is a tad hotter than expected, it will not give the Fed a moment of hesitation when they announce a rate cut next week. If anything, the jump in jobless claims will inject a bit more urgency in the Fed’s decision making, with Powell likely signaling a sequence of rate cuts is on the way.”

So, while the Fed is trying to land inflation in between a rock and a hard place, and, while it is loathe to apply more fuel and raise inflation before it ever touches down, especially after battling it from 2022 through most of 2024, the Fed does have a history of believing job one is to keep its bubbles aloft in order to keep the economy popping. The question is whether it will keep the bubbles aloft at the cost of more inflation or choose naively to believe today’s new inflation is “transitory.”

“Hit the afterburners, Captain!”

In fact, some are now practically demanding a supercut in interest rates: