THE DEEPER DIVE: Trumpflation and Predictions for the Crisis Ahead

We'll take a deep look at where we really are right now and why things are likely to go very badly as we head into what one economist calls "uncharted territory" for the rest of this year.

Trump Inflation is cruising in like a heat-seeking missile right now. First, it was tariff inflation that was staring to show up at the end of last year but getting ready, according to retailers, to really take off this year. However, just as the tariff inflation fired its main engines, the inflation from the oil wars in Iran also began:

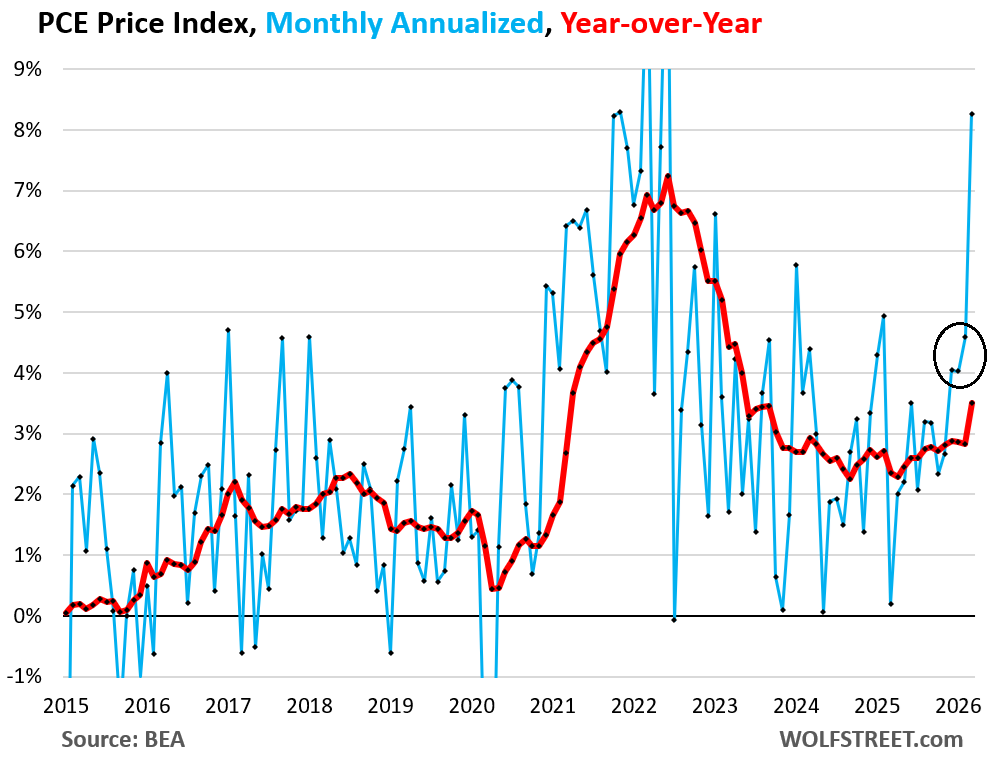

Inflation has been accelerating since mid-2025. In each of the three months of December, January, and February – so before the war and before the energy price spike – the PCE price index had already surged by 4% to 4.6% annualized (black circle in the chart). The March spike is on top of that acceleration (blue line). And it was energy, but not just energy. (Wolf Street)

With those words, Wolf Richter confirms my main thesis of last year, which was that tariffs would start to push through into consumer prices during the holiday shopping season. While, I had predicted the timing for the holiday season, it actually happened immediately at the end of the holidays because 1) retailers had laid in more overstock when front-running the tariffs than I estimated was likely and 2) they had strong incentive not to mess with their all-important holiday sales in order to end the year in the black.

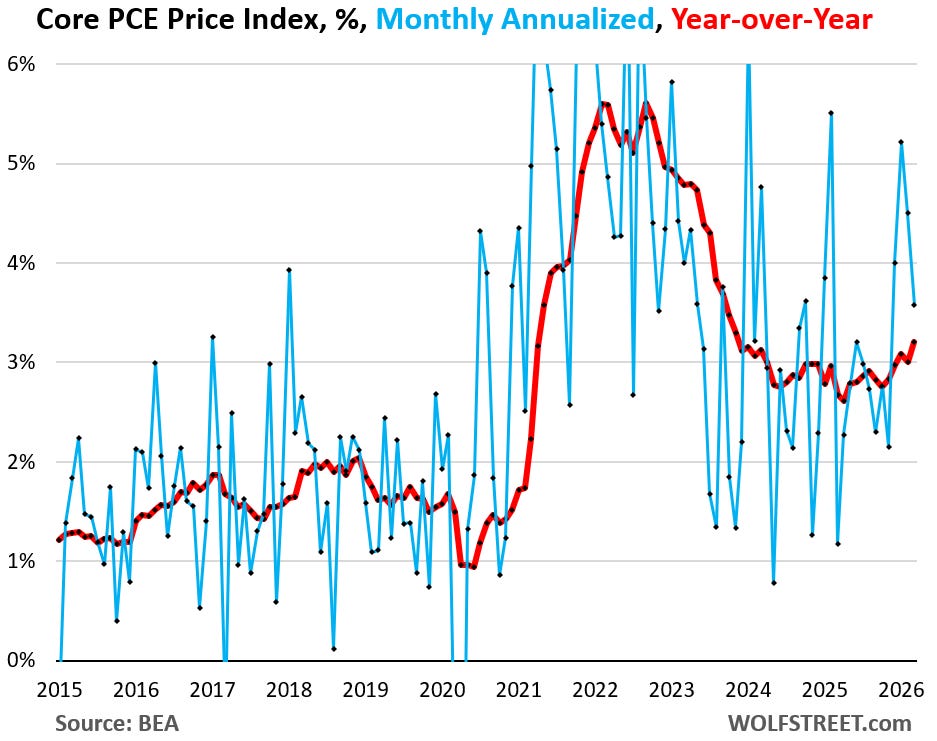

As you can see core PCE inflation, which excludes energy prices, started rising in December, and that was all from the tariffs pushing through:

Now the blue line in the first graph for all PCE prices, which means it includes fuels, blasted off in March, and that, of course, is war inflation due to the new historic energy crisis that hit at the start of March. That inflation, I’ve been saying, is going to be even worse than what was just starting to come through from tariffs.

Singling that move out to energy …

The energy PCE price index exploded by a historic 11.6% in March from February….

March pushed the year-over-year increase to +14.4%, from a negative reading in February. This is what a price shock looks like.

Here is how you know it is going to get worse:

The gasoline, whose prices spiked in March, had already been in tanks at gas stations or at refineries or in transit, purchased at the low February-and-before prices, and that price spike went straight to profit margins of oil companies, refiners, and gasoline retailers.

In other words, there was NO cost spike for the retailers of those fuels because the oil used to produce them had already been purchased at pre-war lower prices. All the Big Oil companies simply took advantage of what was coming and started pricing up to reap outrageous windfall profits, as they usually do. It is price gouging where they profiteer off war. It’s why Big Oil is such an major sector of the Military Industrial Complex.

Soon, however, price increases will be coming from the higher acquisition costs for all this fuel due to shortages and long shipping delays.

Diving for real answers

If we want to get a snapshot of the US economy, outside of deeply flawed government data (due to shutdowns and DOGE firings, then government restarts, plus all the usual biases that existed in the metrics to make the government look as good as possible for years), then we can look at April’s Purchase Managers Index (PMI), which is a strictly business metric.

There was actually a slight uptick in April’s overall PMI measure for how businesses were performing, but it came with a significant caveat as well:

“The surge in manufacturing activity in April is not the cause for cheer that at first glance it suggests. A key driving force behind the upturn is the need for companies to get ahead of further feared price rises and supply shortages, providing a short-term boost that could fade in the coming months as headwinds to the economy continue to build... Employment has fallen as firms grow increasingly worried over the need to reduce cost overheads amid an environment of rising raw material prices, while selling prices have jumped higher as producers seek to protect their margins. (Zero Hedge)

In other words, the very same kind of front-running we saw when tariffs were first being imposed hit in March as oil prices rose and companies rushed to get as much produced or shipped as possible in advance of even higher oil prices to come. That is business brought forward that will create a lull later on. Employment is falling as companies also start cutting to the bone to reduce costs. And the prices companies are charging are up because businesses can no longer afford not to pass along their cost increases, having exhausted that ability during the final months of last year when they did the last tariff absorption they were willing to do to preserve market share at the cost of profits.

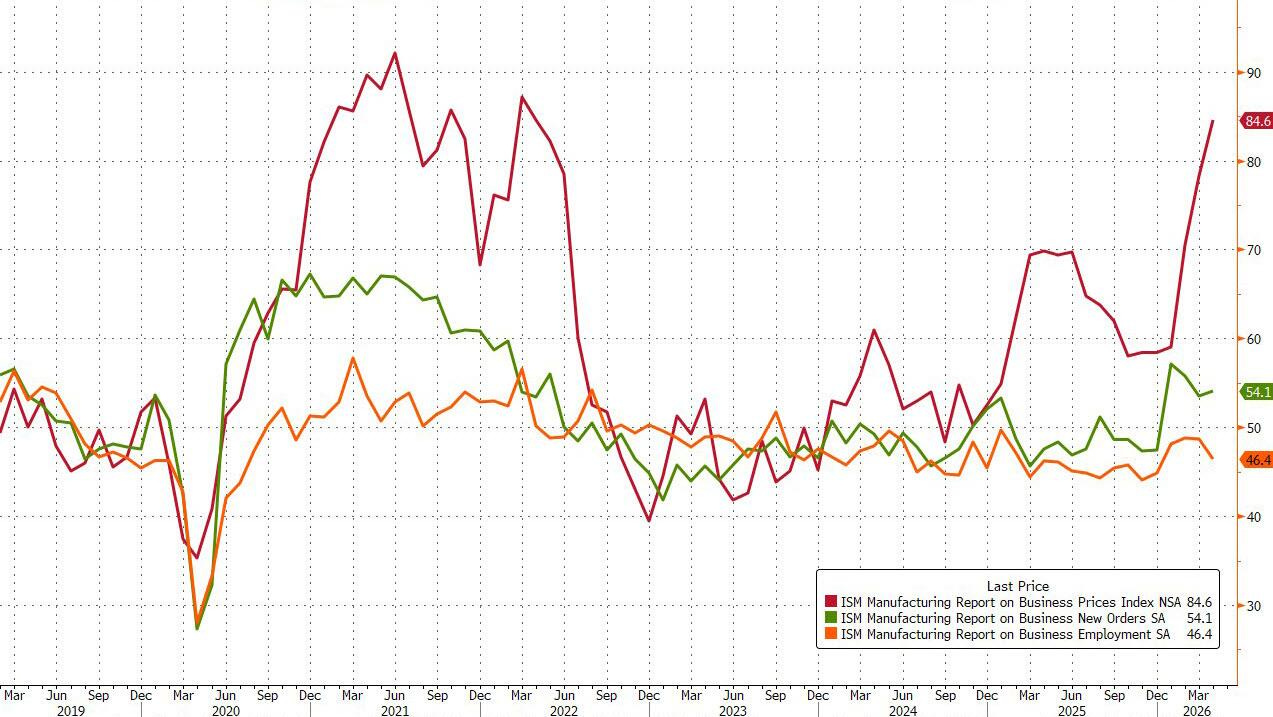

Under the hood, Prices Paid continued to rise dramatically while New Orders and Employment dipped again - another indication that stagflation remains the biggest risk for the economy.

New Orders 54.1, missing expectations of 54.5

Prices Paid 84.6, higher than expectations of 80.3

Employment 46.4, missing expectations of48.8

As you can see, the two main divergent lines here are that prices have soared since the start of the year while employment just started falling:

A lot of the price rise was pre-war, so that period was the effect of the tariffs pass-through finally beginning to show in December.

Obviously, if the war persists and price pressures and supply delays accelerate, demand, employment and production capabilities will inevitably start to be even more adversely affected until the broader economy finally cracks.

And, for right now, the Trump-Israel-Iran War has settled into a war of attrition where both sides are keeping the Strait of Hormuz locked down to see who blinks first.

What is with this week’s contradictory national-debt numbers?

Now let’s take a look at two seemingly conflicting numbers this past week that came out with the GDP report and look at what the rising GDP report was really made of. Then I’ll conclude with some major predictions about where we are heading from here.

“We’re headed toward uncharted territory…”