The Electric Kool Aid Stock Market Crash Test

How overpriced, overbought and out of touch with the overall economy is the US stock market? Let me tell you in pictures.

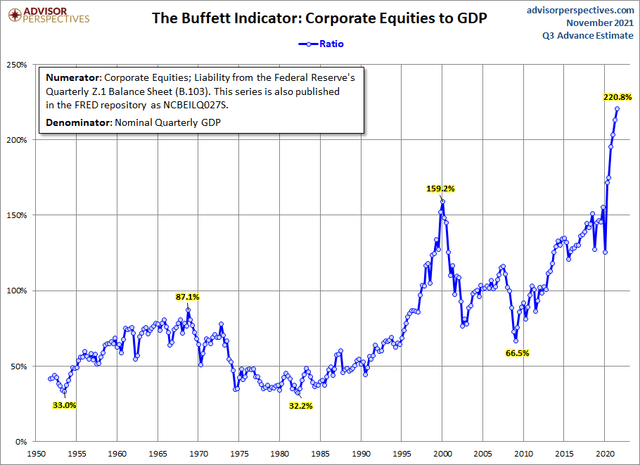

First, let's start with a comparison of stock prices to the US economy as it stands today:

Based on Warren Buffet's favorite indicator of stock-market over-or-under-valuation, the market is far more overvalued than it has ever been relative to the economy at anytime in history.

Keep in mind, the economy is on a shrinking trend, meaning the market will soon be even more overpriced relative to the overall economy. In fact, I've already stated I believe the economy will be sinking into recession by the end of the year.

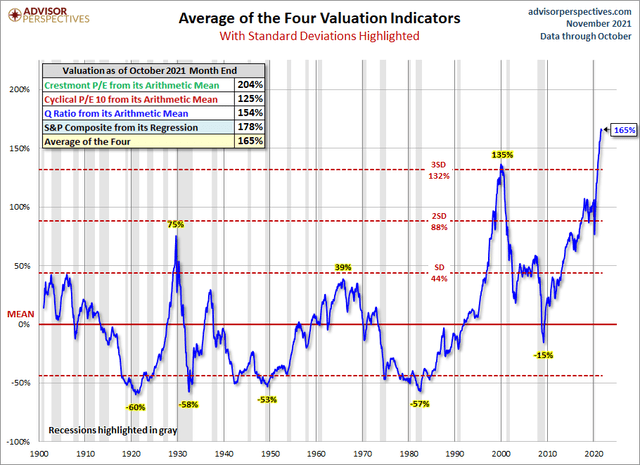

Here is a similar kind of measure that compiles four major valuation indicators compared to each one's mean:

Apparently, things don't do well this far above their means.

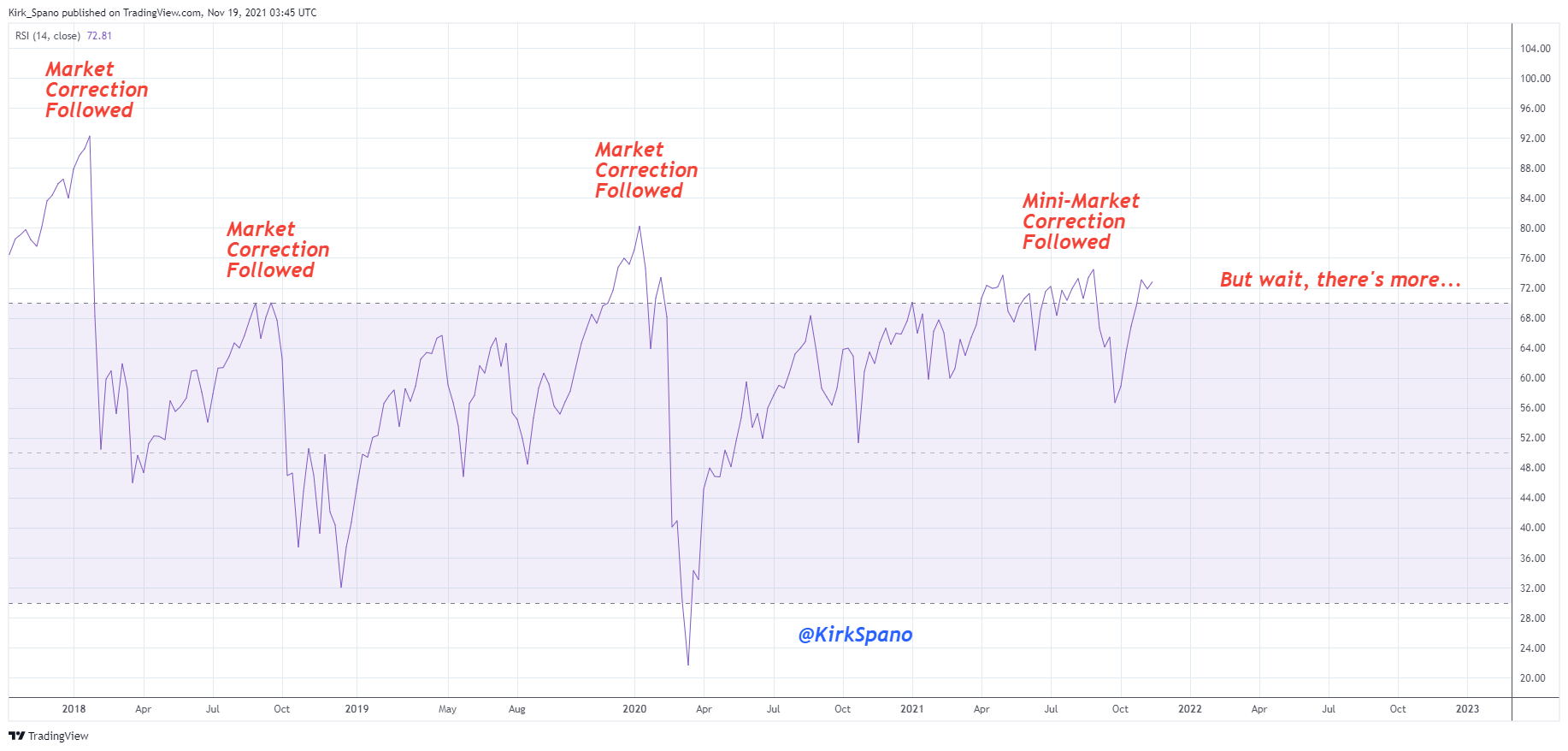

Here is the SPY (S&P 500 proxy) relative strength index:

You can see that the market does not tend to perform well whenever it gets up into this nosebleed section. It attempted a correction in September and October, months I've said the market tends to make corrections in, but it has since rebounded. That means it has been up in these top bleachers longer than it has in the past before a major correction or crash ensued. Let's see what happens now that the Fed has started withdrawing support (and, hence, liquidity) from the market. How long will the market hold against that falling tide of money supply? Ask yourself if it looks like a good perch now from which to fight the Fed, given the Fed has just changed directions.

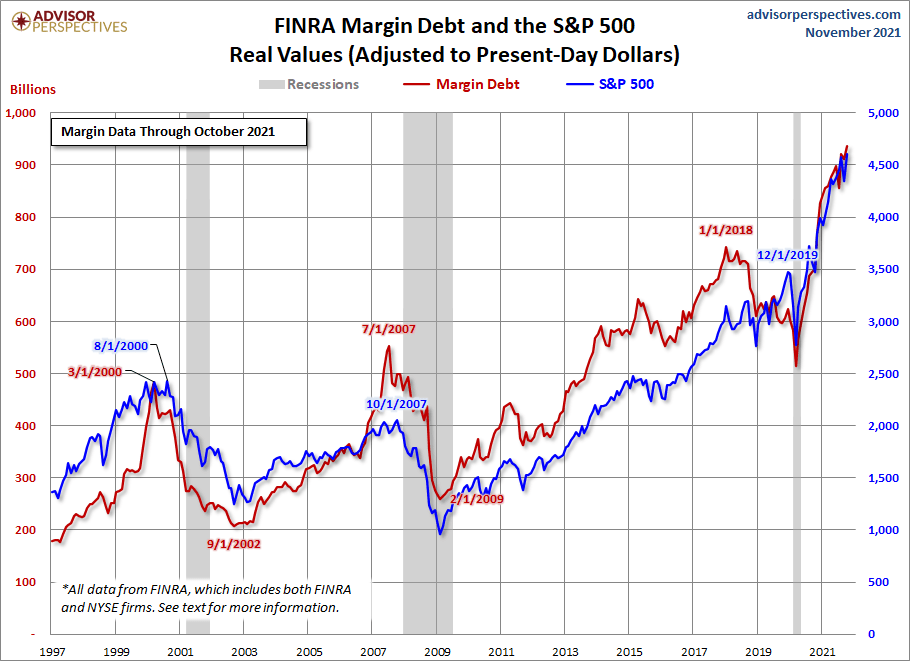

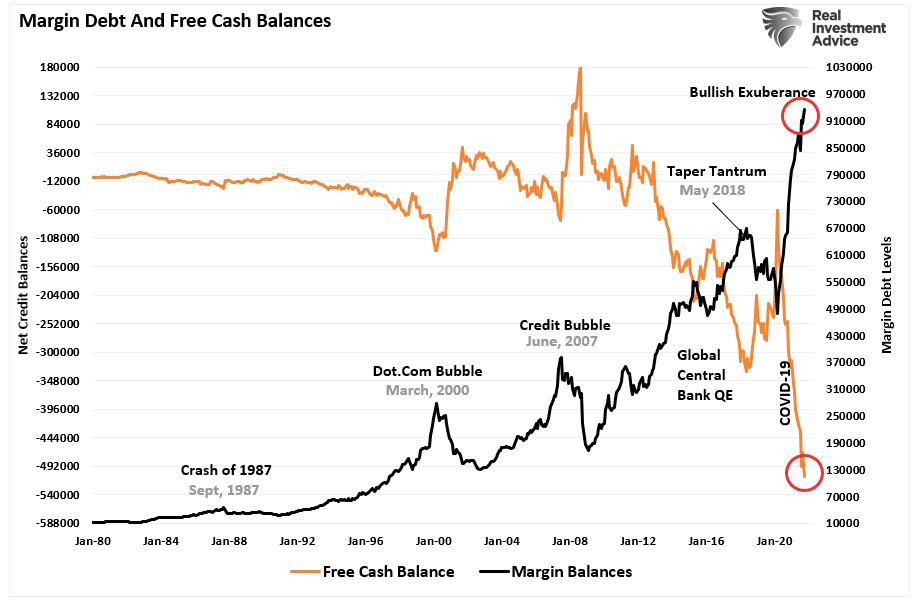

How about leverage? Is the market over-leveraged yet?

Oops. Looks like use of leverage used to buy stocks (money borrowed from brokers) is in the nose-bleed section, too. Leverage becomes tighter when the Fed tightens monetary liquidity, and leverage is already higher in terms of inflation-adjusted valuations (something we need to be factoring in now) than it was before the two worst crashes since the Great Depression.

Here is another view of margin debt of clients at brokerage firms:

That is an extremely precarious position, carried to such near-record heights (beaten only just before the Great Recession crash) due to extreme greed taking highly leveraged risks. When leverage tightens, as the Fed is assuring us it soon will, people in highly levered positions are pressed to sell. High leverage, thus, tends to equate with major and rapid crashes when a correction comes, especially if interest rises, tightening the noose on leverage.

I showed in my last Patron Post bond interest is going to do exactly that during the Fed's tapering, regardless of the Fed's target bottom rate, and treasury bond interest is the peg that establishes many interest rates. The key reason I gave for stating that bond interest will be rising, in case anyone missed it, is the one simple fact I alluded to in my last article but only revealed in my last Patron Post: the Fed is the biggest whale the treasury market has ever seen. It has been hosing up more than half of all issuances. That means the Fed is THE price setter in the treasury market.

The Fed, however, is now giving up its whaliness. It isn't selling, but it is stopping its buying. That inevitably means it will stop being the price setter as it steps out of the treasury market. The Fed's interference as a whale has kept the treasury market from pricing in inflation. As the Fed moves away from interfering, natural market pricing will be all that is left. So, interest rates will start to reflect true price discovery, and the discovery will be bleak when revealed because rates have a lot of catching up to do just to get to where inflation is today.

What does that interest-rate change mean for stocks (even without factoring the bond market's rising competition in terms of stock break-evens). Think of all the leverage above. Now think of leverage as the cornice of snow at the top of the mountain. The greater the overhang, the greater the avalanche when the weather changes and the cornice breaks off. There is more overhang than at any time in history, and the weather is now changing.

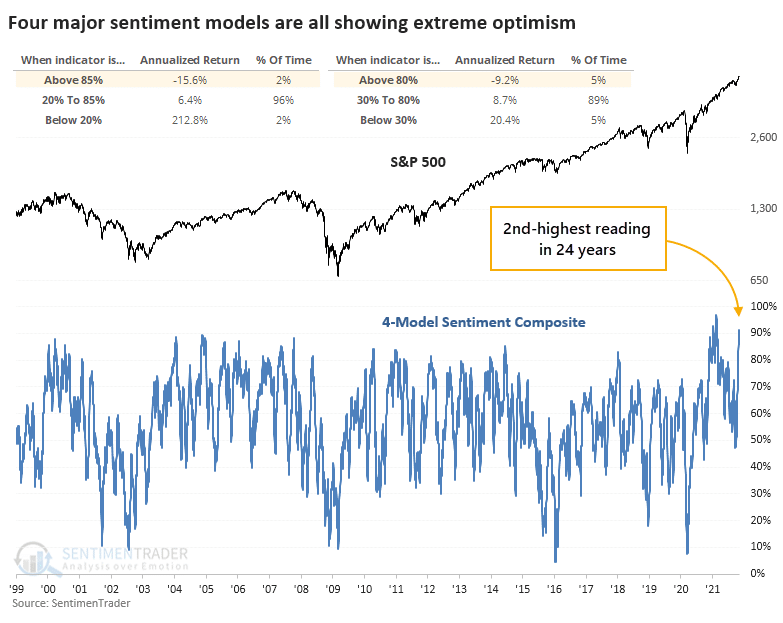

And the market is looking very, very greedy right now based on several measures of sentiment.

The chart [below] shows us that the S&P 500’s annualized return when the composite model was above 80% was a miserly -9.2%. When the model was above 85%, accounting for about 2% of all days since 1998, that return was a horrid -15.6%.â€

The chart is at 90% right now, its second-highest reading in twenty-four years (with both of those highs happening in 2021).

This kind of feeding frenzy is typical of late-stage, melt-up markets. Even Goldman Sachs says the market looks extremely greedy right now. Says David Solomon, the big GS boss,

When I step back and think about my 40-year career, there have been periods of time when greed has far outpaced fear -- we are in one of those periods. My experience says those periods aren’t long lived. Something will rebalance it and bring a little bit more perspective.... Chances are interest rates will move up, and if interest rates move up that in of itself will take some of the exuberance out of certain markets.

I think a lot of "perspective" is about to dawn, and rebalancing is not likely to be too much fun for those who buy and hold most stocks.

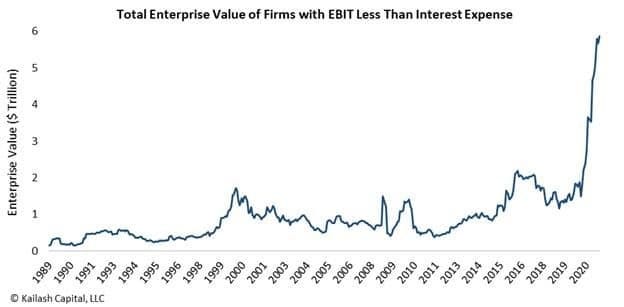

Next, take a look at the record number of zombie corporations -- meaning companies that are only serving on bond issuances, a position that become untenable when interest rises:

What happens to these companies stocks when they lose their ability to role over their high debts with low-interest bonds because even government bonds are rising in interest?

We don’t understand why others are not alarmed by an ‘anything goes’ attitude towards record levels of leverage where interest expense cannot be paid for by profits. Currently, the world is awash in financial alchemy.... Our research has documented that the world has never been less prepared or less equipped to deal with a possible outbreak of inflation or pull-back in Federal largess.

With the entirety of the financial ecosystem more heavily levered than ever, the “instability of stability†is the most significant risk. The “stability/instability paradox†assumes all players are rational and implies avoidance of destruction. In other words, all players will act rationally, and no one will push “the big red button....â€

And how often does that happen?

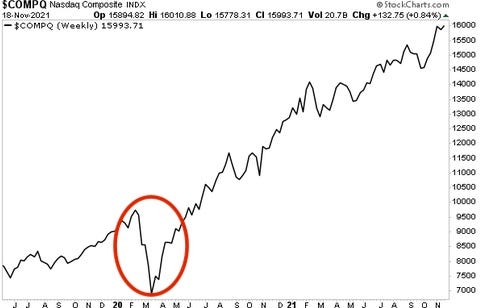

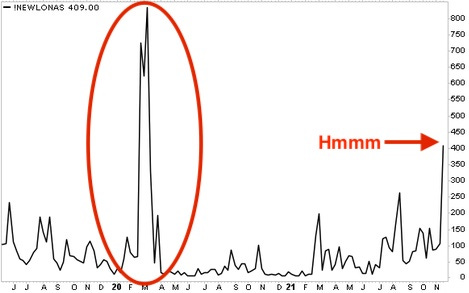

Remember the last time the market did this:

When that happened, the number of NASDAQ stocks hitting new lows looked like this:

Something looks troublesome in an unpleasantly familiar way at the end there. The present rise on this graph means that only a few stocks (the FAANGs) are continuing to do so well they are holding up the NASDAQ against the large number of stocks that are already not doing well. Now that the Fed has started slowing down the money pumps that inflated this market to the nosebleed overvaluations noted above, is that likely to go well?

It's certainly not a perch I'm willing to pile my money on at a time like this when COVID is taking parts of the world high into their fourth phase of rising cases and deaths and when vaccinations are showing they wear out more quickly than originally hoped and when a couple of countries have even reported their new case RATE for the vaccinated is higher than the rate for the unvaccinated, though they don't know why and when port blockages look worse than ever, meaning problems with getting products to market or even making products are still getting worse, and when vaccine mandates are further restricting economic activity by cutting back already short labor supplies.

That's a lot of weight that an overpriced, overbought, over leveraged market has to try to keep pushing uphill ... or not. So, is the stock going to keep rising against all of that when the Fed's hydraulic pumps are being slowly shut down?

I'm not, however, going to lay out in this article all the massive economic problems that are continuing to look worse -- just the market's own metrics of valuation and greed and its internal dynamics. Assess the pictures above to see if they portend peril or pleasure, especially in times like these. I have my reservations.

Others might want to consider their own reservations ... for a parachute out of the stock market before the liquidity squeeze starts taking away the oxygen supply that is necessary for continued breathing so high above the nosebleed zone ... just as the stock market's jetliner is entering a space of extreme economic turbulence. Is this the plane ride you want to be on right now?