The Fed is Dead!

The last few months reveal how dramatic failure of the Fed looks now that it has hit the wall of diminishing returns. I've warned for years that the next recession would look just like what we are now seeing. I'll show below why this graph shows in stark numeric terms just how bad it is.

I’ve said, since stimulus efforts began, that the belly of Great Recession was merely propped up into positive territory by vast amounts of artificial life support and that the Great Recession would reveal its true depth once the artificial life support finally ran out.

"Economic Collapse — The Train Wreck that is Happening Now!"

The next recession, I've written many times, will be something from which the Federal Reserve will not be able to extract us. It's old ammo will not be enough. This graph and present circumstances prove we're there.

QE used to be steroids for the economy; now the steroids are on steroids

It seems like a long time since I wrote the article titled "How Dead is the Fed?" It was, however, only back in March, and already the answer has crystalized in front of us.

Back then I wrote,

You can only be so dead, and that’s just “plain dead.†But there is also Feddy Krueger dead. The kind of dead that keeps on happening like a demonic death that won’t stay dead. It is in that nightmarish Elm St. light that I’m going to review the Federal Reserve’s death.

That is how the Fed dies. It keeps getting back up again and stabbed or chopped sent back down another time. Even back then, I wrote,

Let me pause to assure you, I’m not saying Feddy Krueger is down for the count and will not rise again. He always revives by inventing powers over market death never seen before. Feddy will return with extraordinary and permanent powers beyond those he once used to bring counterfeit salvation from the Great Recession. Feddy gets more empowered by scared government politicians each time the economy crashes. You can’t get rid of Feddy. At least, it seems.

That has already happened. The Fed, without any question, was allowed this week to start buying exchange-traded funds (ETFs) on the stock market to prop the market up a little longer, and the market is up again after a week of falling.

The Fed's impotence as a zombie central bank, however, is clearer now than in March. The Fed's increase in amperage in the graph above tells half the story. The obvious news already coming down the pipeline tells the other half.

Ignoring the period of "Not QE" that I said would evolve into QE4ever, which started in late 2019, look at what the Fed has done just since the start of the Coronacrisis in late February, 2020. The two vertical arrows in the graph are exactly the same size. (One is a copy of the other). In less than three months time, the Fed has done everything it did under QE1, plus everything it did under QE2, plus half of what it did under QE3! It did it all in less than one quarter!

In fact, the Fed has already done as much as everything it did in the first five years of its recovery efforts from the Great Recession. By the end of another month, the Fed will have done everything it did during the entire decade-long "Great Recovery" period and more!

A whole decadal recovery effort in one quarter! And what has the Fed gotten for that?

We still have an economy that is going deeper into recession and a stock market that has only recovered half of what it lost. While people crow about how fast the stock market has recovered, you have to weigh that bounce against the fact that stock markets always have major bounces right after major crashes ... and then they fall some more. (See graphs near the end of "Fiercest Economic Collapse in History is Best Month for Stock Market.")

Less bang for the buck?

For sure! The Fed's Greatest Recovery effort to date brought about as much recovery back to stocks as we would have expected anyway.

Maybe all the Fed's jolt juice made the bounce a little faster and a little higher. Maybe! (The bigger and steeper the fall, however, the more likely the bounce will be big and steep. This latest crash was the steepest in history, so I would expect the sharpest rebound in history.)

That's lot less bang for the buck, given that it was a lot more juice!

The Coronacrisis accelerant

To be sure, this "recovery" period has the coronavirus accelerating all of the damage. What it also has that you hear almost no one in the mainstream media talking about (as if it were completely irrelevant) is all the economic flaws the Fed created over all those "recovery" years with its massive misallocation of assets that drove a wild search for yield.

The Fed's getting a free pass on all that, but the Fed created the mess by permanently killing safe yields with permanently low interest rates. I always said there was no end game for getting off that road once the Fed held it in place as the new norm long enough for the economy to adjust around it.

We no longer have to rely on my claims that those interest rates will remain permanently low. We now know they will. We saw what happened when the Fed tried to raise those rates just a little -- before the Coronacrisis -- so we KNOW the Fed can never raise those rates without killing its recovery.

The Fed's rate hikes and its attempts to back down the money supply it had created with QE crashed the stock market in 2018. It would have crashed much deeper if the Fed had not slammed the brakes on its interest hikes in December of 2018, and then even reversed them in mid 2019.

Then, because the Fed did not immediately stop retracting money supply, it also crashed the Repo market in late 2019 and had to undo that, just as I said it probably would.

So, they're stuck. Period. They proved it. It's conclusive.

The Federal government would DIE if it had to pay real interest rates on the mountain range of the debt it now has pushed up when rates were cheap if it didn't have the Fed backstopping every government issue of debt in any amount necessary to keep those rates cheap. So, that makes low interest permanent, too.

Businesses would have started to die under their debts, too, if the Fed had not returned to artificially lowered interest rates months before the Coronacrisis. At first, it would have been financial businesses.

We saw that happen last year when financial institutions were starving for funding by the end of summer. The Bank for International Settlements reported later that some major financial clearing houses would have failed if the Fed had not intervened by restoring QE in the form of endless repos that quickly morphed into outright QE (the part called "not QE") even before the Coronacrisis began.

So, things were already falling down all over the place, and the Fed was already back to QE and lower interest ... all before the Coronacrisis hit.

It's QE4ever, Baby!

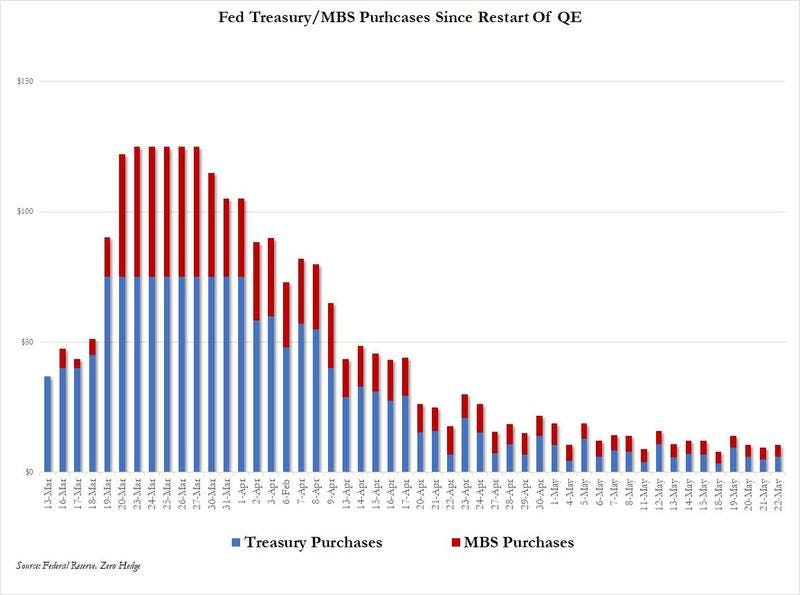

Even now, as the Fed tapers its QE, the Fed is still providing more QE every week than it ever did under QE3:

It looks like the Fed has tapered QE4ever to almost nothing, but that is an illusion. It only looks like QE4ever is dwindling to nothing because the first two months were massive by an order of magnitude above anything the Fed had done prior. That long "dribble" at the end is a continuing rate of $30 billion dollars added to the economy every week or $120 billion a month.

Under QE3, the Fed only added $80 billion a month. So, the Fed is cruising along under QE4ever at a continued clip that remains 50% greater than anytime during QE3! That's a lot of ongoing stimulus! Which the Fed now calls "a taper."

And how much do you want to bet that the Fed will have to up the amperage again when businesses start to fail under the damage from the Coronacrisis lockdown and start to default on their bonds as they are rapidly being downgraded?

How much do you want to bet the Fed will have to up the amperage to stimulate the economy even more when those failed businesses set many job losses in concrete this summer, causing consumers and home buyers to back down even more? Right now, people are thinking all their jobs will bounce back.

How much do you want to bet, the Fed will up the QE jolts because it has to in order to create more money to suck up troubled bonds of declining businesses in order to save the banks and other financial institutions, including retirement-fund managers, before the bonds downgrade to junk?

How much do you want to bet the Fed will have to hit the juice even more when the Federal government starts issuing trillions in new treasuries in the next month to fund the aid checks it is sending out in the mail and to make up for the shortfalls in long-postponed tax revenues and to continue to support unemployment payments on the 10-20% of job losses that turned out to be permanent.

All of that has a funding due date.

So, yes, this is QE4ever, so even the taper to a "mere" 1.5x QE3 per month won't stay down long.

The Coronacrisis (my name for our response to the coronavirus) is causing that damage, BUT the Fed created an economy and a debt nightmare that was already completely dependent on renewed low interest before the virus so much as breathed in our direction. Those zombie businesses that had already seen revenues and real profits decline for more than a year had already forced the Fed back to QE to save their sad souls.

The Fed now has to bail all of that out all over again in addition to what it has to do to offset the Coronacrisis. That was my point in originally stating the next recession would be worse than the Great Recession and an extension of it, because you get to do all over again all the things that just covered over to kick the can down the road, and you have to recover from the new damage of the new recession, whatever that is.

Each round of debt has to be enormously greater in order to swallow the last one and continue to build. Why? Because we don't just FLUSH all bad debts like a free-market economy does.

The government, meanwhile, is arguing about helping states in shutdown because some of those states also already spent themselves broke during the Great Recovery period, and the Republican senate doesn't want to bail out profligate states that destroyed themselves with welfare programs and immigration costs, etc.

So, that past license to spend states up to unsustainable levels of debt is hindering the Coronacrisis relief efforts (wherein we relieve ourselves from the damage we are self-inflicting as never before by shutting down the entire world).

If we were not, in other words, such a total financial heap of wreckage in the first place, the present crisis would be a easier to manage.

All of that is why, in my next article, I'll return to talking about the Epocalypse, which is where I said we would end when the Fed finally fails under a new recession.

Given how hard the Fed is struggling just to get stocks halfway back from their recent crash and just to keep the economy from falling even harder, it doesn't look like the Fed has far to go before all of this runs completely off the rails in one loooong train wreck.

Now that the train wreck has begun, let's see how close it is to what I described in the past.

![By Photo credited to the firm Levy & fils by this site. (It is credited to a photographer "Kuhn" by another publisher [1].) (the source was not disclosed by its uploader.) [Public domain], via Wikimedia Commons](https://substackcdn.com/image/fetch/$s_!ptfR!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9bffb733-56dc-4a86-b69c-9985b33dcd91_500x600.jpeg "By Photo credited to the firm Levy & fils by this site. (It is credited to a photographer \"Kuhn\" by another publisher [1].) (the source was not disclosed by its uploader.) [Public domain], via Wikimedia Commons")