The Fed is Still Spiking the Inflation Punch Bowl, but the Party is in Recess Anyway

Sizzling inflation is not going away as drunken market revelers are hoping. This party bore, in fact, will be long outstaying her welcome. While the Fed once said it wanted some hot inflation on the scene, she arrived a lot hotter and has stayed a lot longer than Father Fed expected -- now kind of embarrassing the old man. I'm going to tell you why inflation won't be leaving anytime soon nor cooling off but will escort us into the recession we are already staggering into.

Three weeks ago, Deutsche Bank shocked the polite world of finance - where nobody dares to tell the truth if the truth is unpleasant and runs counter to the commission-boosting bias of being bullish on everything - when it became the first Wall Street bank to officially make a US recession in late 2023 its base case.

The only problem with Deutsche's realization -- first of its kind in the world of far-flung finance as it was -- is that DB came up with it back on April 5th. Late 2023 made them the earliest date anyone was talking about. That would be a safe bet since it remains a year and a half from now! The problem I'm referring to, though, is that only a couple of weeks after they made that brazen prediction, the first quarter of 2022 came in recessionary. Nice to be early at being way late to the party!

Now, of course, many will argue -- and for the time rightly so -- that a single quarter of retreating GDP does not make me right in my prediction last year that we would be entering recession at the end of 2021. We won't know if I'm right on that until the second quarter of the new year is reported. Some people I respect a lot for their economic straightforwardness and clear thinking, like Wolf Richter, do not believe inflation and Fed tightening will drive us there that quickly. As a matter of fact, I'm still alone, so far as I know, on that assessment.

Better late to the party than last to the party

While we won't know if my proclamation that we are in recession now is accurate until the present quarter's report comes in, I have no doubt that Deutsche Bank is the first of bold banks that is way too late in predicting a recession when it sets the date a year-and-a-half from now, even though that puts them ahead of all the other bold and brilliant financiers in this world. That being the case, even they seem to grasp that inflation is driving us there faster, along with the supply shortages that are contributing to inflation in the midst of that great pool of money the Fed is drowning the economy in. The Fed is finally ready to start sucking the money back out now that it has learned the guest that it, alone, intentionally invited to the party is far from being "transient" visitor.

Last week, the bank doubled down on its shock factor when it came out with an even more bearish view in its latest "House View" note, in which the bank' top economist explained that not only is a recession assured but that inflation expectations "will likely move significantly higher, ultimately leading to an even more aggressive tightening and a deeper recession with a larger rise in unemployment" which in turn will mutate into the outcome the Fed has been so desperate to avoid: a hard landing.

I wrote about the inverted back-flop landing the Fed is about to make with its 747 a couple of days before the article I'm quoting was printed. Apparently DB got my memo because two days later they came out with a memo of their own asking,

How can it be that Deutsche Bank is the only "extreme outlier" that has recession as its base case for 2023 when "given the macro starting point, the burden of proof should be on why this boom/bust cycle won’t end in a recession?"

Indeed. I've been asking the same question. With the gathering of economic troubles we have become swept up in all over the world in the past months -- during which I said inflation would rise to searing heats because of those very kinds of troubles -- surely the burden of proof should lie on those who want to claim the economy will continue to run fine or the bull market in stocks will continue. Why should they continue? HOW will they continue? I think predicting they will continue and inflation will now recede is the extraordinary claim that carries the burden of proof.

However, the financial world has a knack for laying the burden of proof on anyone bringing bad news. They have a penchant for making the base case the most optimistic case -- I suppose because that is what sells stocks and sells loans. And it's easy for them to keep the burden on the bearer of bad-bear news because everyone making good money in stocks wants to keep denying what is happening. No revelers want to see the lights flashing that mean the party is ending, even as the floor is rolling up right under their feet as a pretty strong indicator that the prediction that they're about to take a polar-bear plunge wearing their party finest was right on!

So, I soldier on, often alone and sometimes disrespected by the majority who suddenly become known as the wise ones by simply saying, "I give a 35% chance of a recession within a year-and-a-half" before anyone else did, even though it turns out they were already in one when they made the proclamation that accredits them such foresight for being the first of the last to venture a guess with such a broad range for coming true.

DB came to its conclusion that "the upcoming recession will be more severe than even our outlier House view forecast" on the basis that it could finally see that inflation really was quite hot and holding after all. In other words, they are now recognizing what I was claiming all of last year as to where we would be this year. I might reasonably take note that no one is ever welcome early at any party, especially if they are ringing alarm bells. I might also note, though, that I did say no one at the Fed would realize how hot inflation was going to be until it had already hung around far too long -- an assessment about the Fed's timing that even Ben Burn-the-banky came out and confirmed this week:

Bernanke says the Fed’s slow response to inflation ‘was a mistake’

Former Federal Reserve Chair Ben Bernanke said the central bank erred in waiting to address an inflation problem that has turned into the worst episode in U.S. financial history since the early 1980s.

I'm a little puzzled by the wording of that last comment, but I guess they mean no one was paying attention to recording history (or inflation, anway) until after we all got blindsided by how bad it could be in the early 80s. Well, we didn't learn much because those who are supposed to have their eye on this ball more than anyone just got smacked in side of the head by the ball again with equally bad and even more foreseeable inflation than they had back in the eighties. People back then could be forgiven for not seeing it coming. It hadn't happened before.

One might have thought experiencing stagflation back in the eighties -- when Jerome Powell was young in his central-banking career -- and seeing how hard it was to battle once it got out of control -- that his Federation of Banksters might have kept their eye on the ball a little better than they did over the past year and a half when I kept yelling, "Look out! The ball's going to hit you in your transitory face!"

Sighs.

I soldier on.

And so does CNBC's article about Gentle Ben:

Bernanke, who guided the Fed through the financial crisis that exploded in 2008...

Hold up! Now that's rich. Would this be the same Ben Bernanke who didn't see the recession he was already standing in back in 2008 when the financial crisis exploded while he was telling the world all was well until it abundantly was not? Then he had the courage to lead and save us all from the financial crisis the Fed had created with its financial policy that had been running looser than a goose's bowels after feeding all day on blueberries?

Well, now old Foresight-in-Hindsight Ben lets us know he's gotten his glasses fixed and can see in hindsight agains that Papa Powell is late to the party, too:

“The question is why did they delay that. … Why did they delay their response? I think in retrospect, yes, it was a mistake.... And I think they agree it was a mistake.â€

One has to wonder why the keenly sighted Ben didn't warn us of this before it was obvious. Glad we can all now finally agree it was a mistake. Such a large one, in fact, that Burn-the-banky can probably even see it with his glasses (or contacts) off.

Like the Bernanke-era Fed ....

I assume that was a typo, and they meant the Bernanke-error Fed since the Fed would have never had to solve the Great Financial Crisis, or Great Recession, if Bernanke had realized much earlier that Fed tightening was taking away the punch bowl (driving the dollar-dependent world into a horrid recession) after too many years of also not realizing that Fed loosening was getting everyone drunk and ready to collapse.

But these are the geniuses we rely on and go to in articles like this one by CNBC to find out why we are where we are and to learn that no one could have seen it coming ... other than those who were ignored ... due to lack of credentials or whatever.

Now, stumbling out of the party, punch bowl in hand and slopping the goosed juice all over everyone ...

Now, the Fed is tightening policy with rate hikes and a reduction of its bond holdings that will start in June. However, the Fed is facing criticism that it waited too long to pull back and now confronts inflation running at an 8.3% annual pace.

Facing criticism that it has waited too long, the Fed will wait until June to get right on it.

And I have to actually explain to other market prognosticators why I know inflation will run hotter for longer???

Good grief!

Well, part of the reason is on the demand side of the "too much money chasing too few goods" equation for inflation. That's the only side of this the Fed can control, but the Fed is going to wait until June to stop juicing the party with its Everclear-spiked punch, knowing full well it's already waited too long because, well, it doesn't want to spook the stock market by jerking the punch bowl away.

Bernanke said he understands why the Powell-led Fed waited....

Oh, good. Tell us. Please. Why did they wait for months when it was so foreseeable a year ago? And why are they still waiting?

“One of the reasons was that they wanted not to shock the market.â€

Really?! Who could have guessed that was what they were afraid of? They're still afraid of it. That's why they kept spiking the punch and taking around glasses and encouraging everyone to keep drinking all the way from January to the middle of March, even when inflation was already running at about 8% annually. And that's why they are still saying, "We'll get right on that ... in another month!"

So, shouldn't the base case be that inflation is going to burn your skin off ... and the burden of proof being on those who say, "No, it's peaked and will start going down now" even as the Fed keeps feeding the fire Everclear?

Bernanke explains,

“Jay Powell was on my board during the Taper Tantrum in 2013, which was a very unpleasant experience. He wanted to avoid that kind of thing by giving people as much warning as possible. And so that gradualism was one of several reasons why the Fed didn’t respond more quickly to the inflationary pressure in the middle of 2021.â€

Indeed, we wouldn't want to throw that lush of a market into tantrums by talking too much about inflation back in 2021 when it was clear it was already rising. However, Powell didn't just avoid snatching the punch bowl away; he told the entire party that the punch wasn't even spiked -- that inflation would go away on its own -- so don't worry; keep drinking the goose juice. That'd be Grey Goose, in the very least. He didn't even tell them the punch bowl would be transitory. He told them the drunken stupor of inflation they were feeling would be transitory and that the hot flush lighting up their faces would go away on its own even if they kept imbibing for months to come.

Bernanke notes in the interview that even Powell concedes that he took the nation far beyond full employment. In fact, Bernanke says Powell took the nation to where there are now two jobs of every unemployed person so that he can supposedly whittle away a lot of jobs and we won't even feel the pain.

Thinking there will be little pain, of course, will prove to be another huge mistake when people are forced to go back to work because their stocks have crashed, their stablecoins have proved to be the least stable currency on earth, and even their bonds have gone bust. Suddenly, they will be needing real jobs again, and there may be hordes running to the job market, just as Powell is doing his best to dry those jobs up.

But I digress.

At that point, yes, inflation may cool itself off because people are out of money; but at that point its too late because you are taking away jobs and cooling the economy to kill inflation that is finally ready to dwindle on its own, so you'll be stuffing us down into a depression.

But I progress.

Now that Ben has explained for us how Powell & Co. completely missed the curve (hint: they were drunk), let's get back to today and Deutsche Bank being the first to perceptively predict what is already happening at the Fed's besotted party.

The last shall be first

DB says that it is surprised that of the 75 professional forecasters on Bloomberg, the bank's House view is the only one currently predicting a US recession by the end of 2023.

Being late to foretell what is already happening, they are surprised to be the first. Wow! What does that tell you about how bright the bankers of our world are and how bright the financial press is? DB is the first to come in, and it still thinks recession lies a year-and-a-half away, even with one recessionary quarter clearly standing right in front of them.

The only one not surprised they are the first of the last is me ... well ... and Zero Hedge ... and a few others, such as David Stockman, whom I will be getting to below.

Then again, when it is Wall Street's job to always put lipstick on the bad news pig, it's hardly a surprise.

You can't trust the experts because the experts all have a vested interest in lying to you. That or they're stupid. Yes, the pig is considered to be the one bringing true news if it's bad news, not the many who are slopping at the grand crystal bowl at the center of the party. The pigs are the few with a clear view of the economy because the economy they describe is a pig so ugly its ugliness cannot be hid ... and yet somehow it is hidden. Go figure! One must regale the blurry-eyed investors and their lavish financiers with tales of a long bull run to continue if one wants to be heard and not shouldered aside by the herd.

It is a little difficult in parts of the article quoted to listen to DB's leaders grunt about their foresight and how they came upon it, late as it will prove to be. So, I'll skip over their explanations of how they came to their brilliancy only to have recessionary numbers pop up in the headlines a couple days after they said recession was still almost two years away. In their boasting, they note such things as how many anti-inflationary fundamentals had shifted even prior to Covid to where they were no longer so anti-inflationary. So, their hindsight is now 20/20. That's something, I guess.

Then they make this keen observation:

Inflation is now being driven increasingly by rising costs

Is that not a self-evident truth. Is not inflation always driven by rising costs?

I mean cost v price is just a matter of whether you are the one paying or the one charging. One person's rising cost gets pushed into the next person's rising price. That's just how it works. It was on the basis of that simple knowledge that I started pointing out in the second half of 2020 why my readers needed to start keeping an eye on inflation because the costs going into the prices they would eventually be paying were rising quickly. It is now also partially on the basis of those continuing rising costs behind the consumer's point of purchase that I say inflation will continue to be hot for some time to come and likely rise even more.

I'll ignore the rest of their hindsight and cut to the chase:

Finally, policy measures taken by the Fed as currently envisioned by the markets will be slow to restrain inflation. With inflation remaining anywhere near current levels, the real fed funds rate will remain substantially negative and thereby fail to reach a “restrictive†level, even if balance sheet rundown does more to push up longer-term market rates.

There you go. The Fed's current rate increases, still leave its basic interest rate deeply negative, and it is awfully hard to even imagine how it is that a deeply negative, therefore highly stimulative, interest rate is going to tame inflation. And, yet, we read all kinds of inane articles in the financial news speculating that the minuscule dip in inflation from 8.5% to 8.3% in the last month reported is a sign that inflation is topping.

Nothing is ever a straight line in economics -- at least not for long -- so the fact that inflation is taking a slight rest on the way up doesn't mean much. With interest rates that are in real (inflation-adjusted) terms now more deeply negative than they were in 2020 and most of 2021, the Fed is still adding Everclear to everyone's glass even as the swine are drinking.

Yet, somehow the burden of proof supposedly lies upon those who say this revelry is not going to end well.

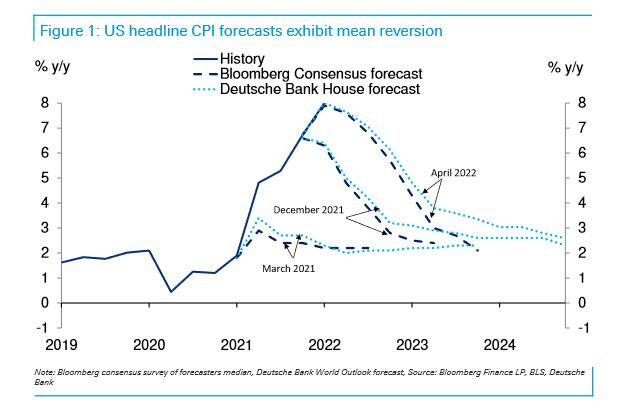

ZH presents this little graph of how the people who should know best have revised their forecasts rapidly upward as the future they were attempting to predict became the past and looked far worse than what they had predicted:

In other words, they keep saying, "Inflation is putting in a top," and then it goes higher, so they revise their forecast higher. You can listen to them, or you can listen to anyone else who started telling you well over a year ago that inflation was going to burn up the Fed's backside before it even started to tighten, forcing it to tighten much faster than it wanted to and to lose control of the situation.

The Fed, at this point, will have to slam the brakes on as hard as Paul Volcker did, and maybe harder, to drive inflation down. Inflation, by driving bond yields higher and the economy lower as inflation strangles consumers, may even do the job before the Fed gets serious enough to get it done. Ultimately, it is hard for a crashed economy to keep driving inflation. It seems counterintuitive as recessions are normally deflationary, but it can happen if the Fed's policies remain too loose, or it can even go hyperinflationary if the Fed tries to rush in and save the stumbling hordes from the disaster the Fed helped bring about by printing more money. We've seen it in history when highly impoverished nations like Zimbabwe faced the worst inflation imaginable, creating an almost hopeless drain vortex of inflationary/recessionary death.

The Fed is still spiking the punch

When you predict things earlier than the pack, the horde says you're dumb because you're too deaf to hear that everyone else is telling you that it isn't going to happen that way. Even now, when GDP already fell by 1.4%, investors demand you prove the economy is sinking into the very recession you said was coming and should now be here. I mean, what do you know? Just because the first quarter of the year did print out a recessionary number that it seems no one saw coming as even a quarterly print, why should we listen to you? Shouldn't the burden of proof be on them to say the factual decline was an anomaly that should be ignored, rather than on the person who said to expect it, and then it showed up?

So, yes, late to the party were all of the banks and investment advisors in seeing inflation, and I am here to say they will be just as late in seeing recession is here, even though it already knocked and told them it is had arrived in last quarter's GDP report. And they will keep demanding proof, no matter how much evidence you give them, because 1) they're not listening to you anyway, and 2) they have stocks to sell! The ability of anyone to hear the truth and especially to tell the truth is inversely proportional to how much his livelihood depends on the alternative.

Now, I'm not saying those who say this quarter's GDP may rise a little above flat again are necessarily wrong. It may be that GDP wavers upward to take a last gasping breath in this quarter, as some are saying it will; but, even if it does, what does that spurt matter, if it goes right back down the next quarter and then deeper the next one after that? It's academic at that point because it makes the upward spurt the anomaly that didn't hold -- nothing but a faint last hurrah if it even happens. And I think the burden of proof surely lies upon all of those who claim recession is far off to prove how that would possibly be the case with all that is cracking up the global economy.

Since my argument stands that inflation will force the Fed to tighten hard into a recession, in this article, I'm just going to look at inflation as the bore at this party who isn't going away because those who argue against recession anytime soon (a hard landing) lean heavily on the notion that inflation is topping, so the Fed really won't have to tighten as hard as it is pretending it is going to. I'd say, so far, the only tightening the Fed has done is pretend, and David Stockman would, it seems, agree. (Which is a strong reason to believe inflation will press in harder. Pretend tightening isn't going to get anything under control.)

Stockman starts by noting,

The 10-year UST yield has crossed the 3% mark. So you’d think this was a sign that a modicum of rationality is returning to the bond bits.

Indeed, you might ...

But not really. That’s because inflation is rising even faster than interest rates, meaning that real yields on the fulcrum security for the entire financial system are still dropping ever deeper into negative territory.

This, as I was just saying. The Fed's basic interest level, adjusted for inflation, is more deeply negative than it was when it was trying its best to stimulate the economy out of the Covidcrisis. So, it's going to have to try a lot harder.

Thus, at the end of March the inflation-adjusted (Y/Y CPI) rate dropped to -6.4% and even with the rise of nominal yields since then it still stands close to -6%.

Here’s the thing, however. For the past 40-years the Fed had been driving real yields steadily lower, although even during the money-printing palooza of 2009-2019, the real yield entered negative territory only episodically and marginally.

But after the Fed pulled out all the stops in March 2020 and commenced buying $120 billion per month of government debt, the bottom dropped out in the bond pits. Real yields plunged to territory never before visited, meaning that unless inflation suddenly and drastically plunges, the Fed is still massively behind the curve.

Stockman presents the following Fed graph to show how real interest is historically in the deepest sub-basement (stimulus end of the slope) the US has ever seen:

Presumably, the Fed might need to raise interest to where it, at least, cancels inflation out by reaching an inflation-adjusted level of zero. That is partly because, so long as paying interest is cheaper than inflation, there is an incentive to buy and have now with today's dollars, rather than wait to buy later with highly deflated dollars. That way, you'll be paying back your loan with dollars that have gone down in purchasing power by more than the interest on your loan. In other words, lock in today's price and pay it down with worthless toilet-paper dollars in the future. That's not tightening. That's stimulus. Inflation has always been an effective way of making debt repayment easier. We just devalue the dollar until your $20,000 loan balance is mere chump change. Then you can pay it off with a single paycheck.

The conundrum for the Fed is that, if it raises rates now to a level that crimps everyone's style, there is so much debt out there that has to be rolled over or has variable interest, such as is the case with revolving lines of credit and credit cards, that you'll strangle current debt holders with the interest they will be paying long before you get interest levels up to where they can strangle inflation. It will be the crushing of the economy that takes inflation down. I call that a hard landing.

The Fed isn't fixing the problem because a soft landing in that scenario is impossible. One has to venture to guess whether the Fed is corrupt and knows this or is just that dumb. For my purposes, it has never mattered whether one comes down on the side of corrupt Econ-crashing conspiratorial cabal of banksters or just plain dumb as Bernanke appeared to be when he smiled and pronounced from his crow's nest that he could see no recession anywhere. "No land in sight. Just endless sea," he said as the ship was already sitting on the rocks. Either way gets you to understanding where we are heading. So, I don't spend time on the conspiracies because I cannot prove them, but I can clearly show by getting out my astrolabe and laying out a few plot lines that the Fed is taking us straight into the rocks.

Stockman lays in one of those vectors for us in the following graph of the billions of dollars of debt added to the economy relative to the billions of dollars in return growth:

It's taking more debt to create less growth. Debt has been able to rise higher and higher to maintain GDP growth because real interest, as shown in the red graph, has gone lower and lower. Now we've reached a point where real interest is tunneling due to inflation soaring. The increase in the debt/growth ratio is falling, but it is still resting on a continuously upward trend line. And now the Fed want's to start kicking interest up at half-point hikes at every meeting and simultaneously flush money out of the economy.

So, how is the economy going to keep from receding if the Fed rapidly raises interest at a time when we are already getting less bang for the buck? Especially when interest is still ultra low and the economy and stock market and bond market and crypto market are all sputtering badly? The Fed has already promised it will soon be dumping $95 billion of bonds into the bond pits by the end of summer. How will the bond market absorb that when it is already the worst bond market in history? To me, the burden of proof lies in justifying the idea that the bond market can absorb all that extra bond supply when it is already in the worst sell-off we've ever seen. It makes no rational sense at all to say, "Prove to me that dumping all those bonds will make the situation worse?" I wonder are people thinking at all?

Investors have started backing away from the riskiest corporate bonds in the US, with the amount of debt that trades at distressed levels doubling since the start of the year.... The increase reflects a more hawkish Federal Reserve, which first lifted interest rates in March and is expected to do so again on Wednesday, the beginning of a forecast string of rate rises meant to combat US inflation.

The Fed still has deeply negative interest, and the bond market is already reeling. More tightening will force more debt into the hole. How badly is the Fed failing to tighten so far?

CPI surged by over 50 basis points in March, meaning that even as the Fed hiked 25 basis points, they fell further behind inflation. Absurd yet true, CPI has been over 2% for a year and the Fed just stopped doing QE last month.... So, how much higher does inflation go from here? Prior to the Ukraine invasion, it looked like inflation might have been on track to peak in February or March. With the war in Ukraine, all bets are off.

How bad is the bond market imploding? In another article, Stockman wrote,

As it happens, moreover, this lowest real yield in 60 years is not the end of the story. It can actually be well and truly said that the biggest bond bubble in 800 years is now deflating, and that will make all the difference in the world....

Moreover, the global bond market bubble is deflating at a fearsome pace. The value of global bonds dropped by another $754 billion just last week, bringing total loss from the recent all-time high in mid-2021 to a staggering $4.8 trillion or 7%.

That was published a month ago, and set has only gotten much worse.

At the time, the global bond market top, looked like this:

And, remember, many of those bonds are priced in dollars, even those outside the US, and the changes in Fed policy tend to affect dollar-denominated bonds in emerging markets much harder due to the strengthening dollar. And that was already a pretty ominous looking top in the giant global bond bubble.

Says Stockman,

Needless to say, when this utterly distorted bond market heads south, the global stock market won’t be far behind. After all, current nosebleed levels and out of this world PE ratios are predicated on ultra-low yields and the specious theory of TINA (there is no other alternative to stocks).

As interest rises and more bonds default, interest on bonds rises more. That cycle is certain to drive interest up a lot more than the Fed claims its own moves will ... in addition to its planned target increases of fifty basis points (half a percent) each month. And into this bond fury, the Fed wants to offload more bonds (more QT) than the full amount of QE it did each month during QE3. How is it even conceivable that this will not create exactly the amount of reverse economic pressure downward on top of the present bond bloodbath that QE3 was supposed to give in positive pressure?

This is basic logic that doesn't require any proof: What goes up, must come down. Every action requires an equal-and-opposite reaction. These are things already demonstrated to a level where one can safely use them as a premise, especially for arguments as mundane as action-and-reaction in the realm of basic interest. The Fed once told us it did QE to lower interest, so reversing QE (doing Quantitative Tightening) will raise interest, particularly in the bond market where all QE and QT happen.

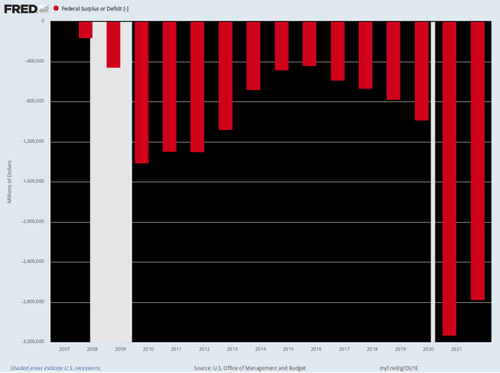

Note the deficits we have added to the aggregate of our national debt over the past decade:

I know. Deficits and debt don't matter because the federal government's banker owns a money press, so it can just print more money. Well, guess what? Even the bubble-headed monetary theorists in the Modern Monetary Theory (MMT) club state that the government can only print money up to the point where it starts causing inflation.

Hello!

We are already far past that. We are in the realm where printing more money in order to maintain loan service on this massively greater bond debt during a time of rapidly rising interest rates will create hyperinflation!

It's not an option.

That's why Stockman notes in the first article I was quoting,

The US Treasury is in a virulent catch-22 when it comes to impending borrowing requirements. That’s because debt service costs will be far higher as interest rates rise, while revenue growth will slowly sharply from current levels as the Fed’s pivot to aggressive tightening grinds the economy to a halt and then into recession.

In other words, current high inflation forces the Fed to tighten. That is the diametric opposite of printing more money for the government to keep servicing its debt. That means raising the government's interest, which means the government either raises your taxes, thus tightening the economy a lot more, or it defaults. The alternative, of course, is that the Fed rapidly resumes its role of being the government's printer of first resort and creates inflation to the moon, and then Zimbabwe-style inflation does the damage of destroying the economy.

Says Stockman,

As the Treasury debt rolls over—especially T-bills and 2-year notes—the average carry cost of the public debt will rise sharply.... In turn, that implies $975 billion of annual net interest expense or more than double the current fiscal year estimate.

That's if Treasury yields rise to an average of 3.75% nominal interest. I'll note, at today's inflation rate, that would still be deep in that sub-basement of a real yield that is close to -5% -- hardly inflation-fighting, albeit what it takes to crush the economy and, thereby, crush inflation in normal times is probably a lot less than what it took in Volcker's time when there was far less overhang of debt. The narrower spread in what it takes only means the attempt at a soft landing is a far more precarious attempt to be made. The numbers are thinner -- more fragile. Less of an error could cause a much deeper recession than Volcker tripped us into.

Stockman sees this strange confluence of enraged and inevitable conflicts playing out in a fierce battle in bond markets:

What that adds up to is the return of the bond vigilantes—a revival of the old “crowding-out†syndrome as the bond pits struggle to fund $3.2 trillion of government debt paper per annum with no helping hand from the Fed’s printing press.

And ...

Of course, the permabulls who were unaccountably out buying equities hand-over-fist after the Fed’s announcement are busy making up new delusions to convince themselves of the impossible. That is, that the Fed will engineer a “soft landing.â€

Not going to happen, he says, as do I.

That’s because a paltry 75 basis point Fed funds rate now, and 225 basis points by year-end, is not going to throttle headline inflation that is pushing 9.0%. And most especially when demand is cooling only slowly, while a whole lot of inflationary pressure is still building in the commodities, PPI and services pipelines.

You'd think some of this stuff would be obvious, but it is not even arguable with the permabulls who believe they can keep pushing up stock prices in the face of all this by pure testosterone. Those pressures Stockman names are the ones I laid out in my last Patron Post and will continue to lay out in order to present those reasons demanded by those who claim the burden of proof is upon the one wanting to say we're crashing headlong into a deeper recession than 2008 due to pervasive and persistent high inflation on top of all the other monumental pressures in the world today -- continuing Covid lockdowns, supply-chain breaks everywhere, and the broadest global sanctions ever imposed plus the residuals tariffs of an old trade war still choking away.

I'll lay out the proofs they are demanding if they want to join in supporting me so they can see them. Otherwise, they can wait for the reality to wash over them, and I'll dig back to those proofs later, opening up those Patron Posts to show them how they really could have and should have seen it coming.

That is all the warning those who arrive late to the party by predicting history get. In the meantime, let them continue to swill from the Fed's punch bowl, still completely full of Everclear, for the month that remains until the Fed finally proves it really will take the bowl way because inflation doesn't even leave the MMT folks in congress any room to stand for further money printing. Sure, they can print. The "press" still works, but it is all the way into hyperdrive inflation if they do!

Wrapping it up

Nothing is going to stop this grand economic collapse from happening. All you can do is protect yourself in the limited ways available and just ready yourself mentally for facing it. It will hurt everyone, but I dare say it will hurt less if you've seen it coming and have prepared what little you can and have steeled yourself to facing it.

I, for example, took 100% of our retirement money out of stocks and out of bonds in January, so I've avoided almost all of the market pain that has already happened. (I had already taken most of it out of stocks, but had a good portion in bonds and a dribble still in stocks.) I've also stashed away some reasonable amount of provisions of those things that we use on a regular basis, as I counseled my readers to do last year. Now, as shortages are appearing, I have a buffer. It's not enough to live on for a long time, but we have enough of each basic item to supply ourselves when store shelves are out and can, then, restock as product dribbles in so that we don't feel the crunch of temporary shortages that are now emerging.

It's a buffer. It doesn't mean I'll feel no pain from the times we are now already clearly entering. I expect that I will, but I've also readied my mind as much as possible to accept the new reality and have, at least, been cushioned from its initial blows with moves that cost me absolutely nothing. Even the laid-in provisions didn't cost us any extra, but saved us from the inflation we've had since I laid them in. As I noted last fall, they cost nothing because I would have had to eventually buy them at a higher price anyway.

Finally, when we sold our farm that was getting to be a bit too much work, what with all the writing I want to do, we banked plenty of good will with the new owners in the form of steeply discounted and even free equipment to sweeten the deal and help them get started and continued friendship with them so that we know we have a place where we can grow our own food if we have to. Good relationships are the most important stock you have for such times, and they can make hard times enjoyable and meaningful. We paid it forward. We chose a young couple from other competing bids who were not the highest bid, but who really wanted to farm the land and who looked like they knew what they were doing, and it turned out they do. Their purely organic crops last summer were outstanding.

I hope others have followed along with my suggestions along the way. I, of course, give my most thorough thoughts to those who deem them worth supporting, but I try to give something to everyone because that's how we get through this.