The Great 2020 Bailout Bonanza

Let us speak of megabanks and global corporations, chicanery and swine, and speak of how the great have feasted in the troughs of trillions dumped out by the present administration, congress, and the Fed, for 2020 makes the bailouts of the Great Recession look like childhood snacks.

Fargo banksters fail to forego illicit gains

Our story for the year begins back in January, well before the COVIDcrisis hit. It is not a tale of bank bailouts but of banksters getting "Get out of Jail Free" cards just as an apropos starting point.

It took four years from the time when Wells Fargo execs were "arrested," so to speak, for creating (of all things in this era of fake everything) fake bank accounts at the end of the Obama administration -- four years until penalties were meted out. Eight senior executives were cuffed to $59 million in penalties. John Stumpf, former CEO, took a $17.5 million whack on the hand from the hand of justice.

You may recall the crime: bank employees had been pushed to create millions of fake accounts in the names of Wells Fargo customers without the customers knowing. The bank, itself, paid billions in fines from bank money, but the crime instigators paid only millions. Now, you might say, $59 mil is a lot of dough, even divided eight ways, but if you weigh Stumpf's portions against his gains, as an example, he made off quite well.

Ordered to get out of Dodge, Stumpf was set to exit into early retirement with $130 million that he had amassed in stocks, cash payouts and other compensation over the course of three decades of bank fraud. $107 million of that was in the form of bank shares he had accumulated.

Of course, his fraudulent government of the bank had diminished his share value from an earlier high of $200 million, so he did take a hit from natural causes. National outrage also pressed him to forego $45 million of the $130 million that would have been his retirement take. More outrage stripped another $28 million from Stumpf's parting package before he got his butt safe out the doors of justice. He still exited with more than $50 million in retirement parting value.

Senator Elizabeth Warren tried somewhat unsuccessfully to press Stumpf to repay every dime he had ever made from his years of running the crime operation called "Wells Fargo."

If @WellsFargo’s John Stumpf is leaving with all of his ill-gotten millions, that's still not real accountability.

— Elizabeth Warren (@SenWarren) October 12, 2016

To frame it another way, Stumpf's target pay package just for 2016, his final year, was $19.3 million. So, with fines of $17.5 million, he conceivably made a profit even in his final year of $1.8 million, not counting his retirement parting gift. So, crime still pays, even after it costs you something. His replacement, by the way, received a 40% bump in that pay package to talk him into working with Wells. He'll need that 40% to cover his eventual crime fees if he follows the Wells' modus operandi.

While Stumpf was banned from ever working in banking again, he was old enough that he probably didn't want to work any longer anyway. More time for golf, and the best part is none of that tee-time was taken away by a pesky prison sentence. So, that was a bonus!

Hedge hogs wallowed in plenty

It’s a complete abomination.

That's how Bloomberg News quoted one business services provider regarding the amount of money hedge funds had managed to scrape off the top of March's bailouts in less than a month.

The April article noted that hedge funds and taken $350 billion in ...

bailout money intended to help cash-strapped small businesses in the throes of a deep recession wrought by the outbreak of COVID-19 ... to cover everything from payroll to rent and utilities for hair salons, restaurants and other businesses that have been bludgeoned by forced closures.

Hedge funds, the often notorious big speculative losers in past years, suddenly saw money floating along like a smorgasbord on a life raft to save themselves -- not from COVID but from years of bad bets.

Chamath Palihapitiya, chief executive of venture-capital firm Social Capital LP, last week argued that the Fed’s massive coronavirus stimulus package helps the ultrarich at the expense of ordinary American workers. “On Main Street today, people are getting wiped out right now — rich CEOs are not, boards that have horrible governance are not. People are,†Palihapitiya said.... "We’re talking about a hedge fund that serves a bunch of billionaire family offices. Who cares? They don’t get the summer in the Hamptons?... Who cares? Let them get wiped out."

Thank God the present bailouts, engineered by the administration's Goldman Sucks US Treasurer, saved them. Steven Munchkin's party invites to the Hamptons would surely have suffered otherwise. Where would he be next time he needed a swimming pool from which to text the world that he had called all the major US banks, as he did in December of 2018, to make sure they had enough money to survive possible bank runs?

Shouldn't the Coronacrash have been profitable enough for hedge funds? I thought they were designed precisely for times such as we saw last March when the stock market plunged:

In theory, the current environment for hedge funds should be favorable to stock picking, compared with the period that preceded this current environment, where hedge funds failed to outperform market benchmarks.

My thoughts exactly. The swine!

Hedge hogs not the only ones at the trough

In an article title "Wall Street feasts on federal coronavirus aid while Main Street starves," the New York Post said the bailout funds were designed perfectly to engorge Wall Street speculators. Of course they were. They were crafted by the Goldman sacks of excrement that float in the swamp-filled White House.

Wall Street executives and analysts predict a tale of two economies: Wall Street traders will make money, while Main Street businesses face economic conditions not seen since the Great Depression.

That depression is slowly building. The economy did no spring back in a full "V," and now we are going back into new shutdowns to add additional damage when we haven't even seen all the knock-on effects from the first shutdown. Those have been forestalled by these bailouts accomplishing some of what they were intended to for as well as a lot of what they were supposedly not intended for (although I'm sure the crafty ones knew exactly how they'd be utilized).

I hope the money made on Wall Street trades will trickle down to small businesses when the economy opens up. But there is good reason to believe the trickle-down will be pretty thin. Wall Street may recover fast as the economy founders.

It did. Stocks saw a V-shaped recovery. The main economy did not. Unemployment still beats any record during my lifetime. The Federal Reserve targeted $10 trillion to go into the financial system if necessary in those early months of this whacked-out year, which would be a huge boon to stocks, which is where the main flow went right from the start:

$3 trillion for Wall Street in a flash.

0.2% of $600B in 2 months for Main Street.

Money quote: “This whole thing is kind of a joke.†https://t.co/Yg4TimcCro— Sven Henrich (@NorthmanTrader) September 15, 2020

These trillions flowed into just about every corner of high finance; the Fed’s new programs even allowed it to buy up mortgage-backed securities pegged to strip malls that were teetering before the pandemic hit.

The crisis hit just in time to save some of the zombies that had managed to survive the Retail Apocalypse I wrote about for almost three years ... from the time when it was faintly beginning.

You read that right: The Fed is now bailing out Wall Streeters who bet on strip malls.

Not just those who bet on strip malls in a crowded retail market, but even those who did so as that market was already entering decline. Never let a good crisis go to waste when you can use it to save the rich and foolish.

Meanwhile, over on Main Street ...

The small-biz loans were ... slow in coming because of confusion on how to administer the program. Thousands of small businesses applied, but many were turned away, even though they operated thriving companies.

Well, that's what happens when you install tentacles of the vampire squid in the US Treasury.

Wall Street execs are scared. They vividly recall the last time economic bailouts were skewed to high finance in the aftermath of the 2008 banking crisis, when firms like Goldman Sachs began announcing record profits, largely on trading, when the Fed slashed rates while Main Street was mired in the Great Recession.

Surprise, surprise. Goldman made sacks of gold all over again in this crisis because the funds were administered through them and other major Wall Street banks. (More on that to follow.)

The result was public scorn and the Occupy Wall Street movement. Wall Street fears that, given the manifestly unjust disparities now, the country could soon see social unrest not seen since the 1930s.

That was said before riots broke out all over the nation.

As the article concludes, devils swarm in the details of rescue packages. They also swarm at Goldman Sachs, the US Treasury, and the Federal Reserve.

The Wall Street Journal noted one of the primary stimulus programs has been fraught with complaints of fraud:

The federal government is swamped with reports of potential fraud in the Paycheck Protection Program, according to government officials and public data, casting a shadow on one of Washington’s signature responses to the coronavirus pandemic.

JPMorgan hogs the show

Goldman sat in the government trough, but JP wallowed in there with them. Bloomberg reported,

JPMorgan Chase & Co. provided loans to virtually all of its commercial banking customers that sought financing through the small business relief program, while the lender’s smallest customers were almost entirely shut out, according to data disclosed by the bank.... Only 6% of smaller customers got paycheck-protection loans….

Who woulda thought that, if you put Wall Street's commercial banks in charge of administering all this free Fed float, they would give the boar's share to their biggest clients, watching out for them before looking out for the little guy? No one could have seen that coming. Right?

The income made from transacting the loans is why major banks were able to report such handsome profits in their quarterly earnings over the last couple of quarters, driving up their stock prices, even as the economy remained bogged in the mud. Thus, these programs were also pass-through bailout to the major banks, which got bailed out first and foremost ... again.

As I also reported in articles last spring,

Restaurant chains, including Shake Shack Inc., Ruth’s Hospitality Group Inc., which operates Ruth’s Chris Steak House, and sandwich chain Potbelly Corp., received loans through JPMorgan.

Some of those were quickly returned when public outrage came swiftly. Many of those were not returned at all. They morphed into government grants over time.

“We helped our clients as they came to us and stand fully prepared to help tens of thousands more small businesses apply as soon as additional funds become available.â€

The big pigs were able to crowd up to the trough first because the programs were complicated and required teams of lawyers to apply, making it almost impossible for small businesses to even get in line. So, yes JPM helped its (big) clients on a first-come-first-serve basis, and then promised that, if more funds became available, they would certainly be glad to help small businesses, too.

The sweetener in the deal was that the commercial banks got a percentage of the deal. So, helping one business with a whale of a loan at 5% or whatever the going rate was makes a lot more money a lot faster for a lot less work than helping a hundred smaller businesses.

Banks earned origination fees of 5% on loans of up to $350,000; 3% on loans between $350,000 and $2 million; and 1% on loans between $2 million and $10 million. That means they earned $17,500 for processing a $350,000 loan, compared with $100,000 for a $10 million loan.

So, you pick the low-hanging fruit first, then take care of the rest.

In the end, a lot of small businesses did get loans. A lot didn't.

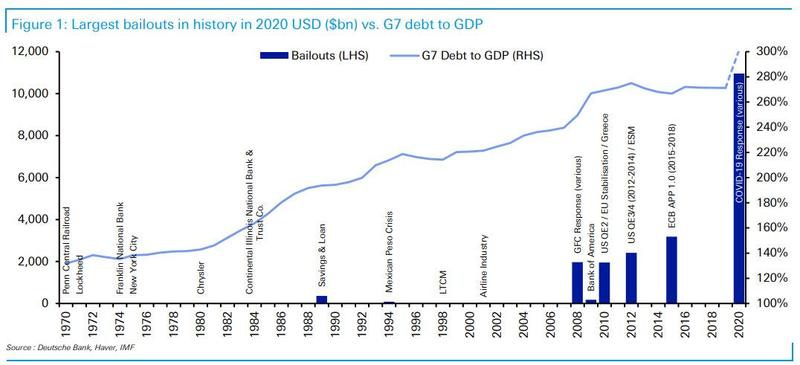

How big da pig?

I'm not saying no bailouts should happen in such extraordinary circumstances, but many major global corporations that starved themselves for cash by doing stock buybacks to grossly enrich their stockholders who also suckled sweet dividends at high levels for years, ran squealing to government troughs all over the world. They would have had enough to whether through tough times if they had not engorged themselves on their own fat for years.

So, let's do take a look at how these 2020 bailouts compared to all previous bailouts in history on a global scale:

The point is that we are once more in too big to fail territory and the authorities are doing everything they can to minimise defaults in this crisis - defaults which somehow are nobody's fault yet the world has never had more debt making it the most prone to even the smallest shock. As such to say that the aftermath of the coronacrisis is nobody's fault is a borderline crime - it is the fault of everyone who believed that the Fed has made any future crashes impossible… starting with the Fed itself. After all who can forget Janet Yellen's idiotic declaration that there will be no more crises in our lifetime.

Even Crazy Cramer gets it:

The pandemic led to "one of the greatest wealth transfers in history.... I think we're looking at a V-shaped recovery in the stock market, and that has almost nothing to do with a V-shaped recovery in the economy," he said. "The companies that took the money just got a big break: they only need to spend 60% on their employees to get the loans forgiven, down from the original 75%."

Where are the swine herders?

Another big problem is that no one is watching over the hogs. Bloomberg Law reported in June:

Trillions in Stimulus Go Unchecked With Watchdogs Kept Toothless.

The U.S. has spent more than half of $3 trillion in economic rescue funds passed by Congress -- with little of the oversight intended to ensure the money goes to the right places.... A special inspector general was only recently sworn in, a congressional panel still lacks a chairman and staff, and President Donald Trump quickly removed the official who was going to lead a separate accountability committee.... Mistrust in Washington is so deep that the oversight groups’ investigations are already mired in politics.

But why would congress want watchdogs? Of course, they were slow in forming the oversight committee and could not agree. After all ...

Congress sucks up part of the swill

Some of the beneficiaries from this ocean of funds were owned in whole or in part by members of congress ... and by the president ... and their friends and family. So, better to keep the watchdogs tied up in committee formation as long as possible.

Of course, I'm not suggesting any wrongdoing here. (I don't have to, it's suggesting itself.)

When filling these hog troughs, people like Father Fed Powell and the Munchkin don't ask, "How can we design these programs so the big banks and major corporations don't suck the sow's share off the top?" Why would they do that when that is the purpose? Who cares about the runts in the litter as the sow steps all over them?

Many in congress don't ask that either. You tell me why they wouldn't.

New data shows lawmakers secured millions in small-business aid.

Companies linked to lawmakers and congressional caucuses have received at least $11 million in aid from the federal program that Congress created to help small businesses....

Members who have in some way benefited from the Paycheck Protection Program but were previously unknown include Rep. Rick Allen (R-Ga.), the founder of a construction company; Rep. Mike Kelly (R-Pa.), who owns several car dealerships; Rep. Kevin Hern (R-Okla.), the owner of multiple McDonald’s franchises; Rep. Markwayne Mullin (R-Okla.), who took over his family plumbing business; and Rep. Matt Cartwright (D-Pa.), whose wife is a partner at her family law firm..., including GOP Rep. Roger Williams of Texas, a wealthy businessman who owns auto dealerships, body shops and car washes, and Republican Rep. Vicky Hartzler of Missouri, whose family owns multiple farms and equipment suppliers across the Midwest.

Ah, well, that's small potato peels.

But the program’s connections to Congress, the majority of which were previously undisclosed, have raised new questions about the administration’s secrecy of the $670 billion program, as well as potential conflicts of interest as lawmakers prepare to craft the next coronavirus rescue package.

The Paycheck Protection Program has faced transparency complaints and intense scrutiny over charges it was helping the well-connected after reports revealed that large corporations ... were among the first to be awarded loans, while smaller businesses were stuck in line....

In May, Democrats tried to pry free the list of recipients, but their push in the House to require disclosure of at least some companies was blocked on the floor by Republicans — including Kelly, Allen, Hern, Mullin, Williams and Hartzler, who all voted against the bill.

There was a lot more feet in the slop than just those in congress:

Trump’s Small Biz Rescue Bailed Out Kushner’s Family, Obama’s Aides and Other Political Elite

It turns out that Trump’s pals weren’t the ones catching the windfall so much as Washington, D.C.’s well-off and well-connected in general. Among the entities cashing six to seven-figure checks from the federal government’s Paycheck Protection Program in recent months were a fiscal responsibility advocacy organization run by anti-tax crusader Grover Norquist, a high-powered consulting firm run by former Secretary of State Madeleine Albright, the nonprofit headed by former Trump campaign official David Bossie, and a political strategy firm linked to two alumni of the Obama White House.

It turns out that Trump’s pals weren’t the ones catching the windfall so much as Washington, D.C.’s well-off and well-connected in general. Among the entities cashing six to seven-figure checks from the federal government’s Paycheck Protection Program in recent months were a fiscal responsibility advocacy organization run by anti-tax crusader Grover Norquist, a high-powered consulting firm run by former Secretary of State Madeleine Albright, the nonprofit headed by former Trump campaign official David Bossie, and a political strategy firm linked to two alumni of the Obama White House.... Businesses tied to the president’s son-in-law as well as members of Congress got taxpayer funds.... The Observer was not the only Kushner family business to take advantage of the PPP program. Two of the family's New Jersey hotels also cashed in....

Meanwhile, the conservative online media outlet founded by Trump confidante and Fox News host Tucker Carlson, the Daily Caller, received as much as $1 million. Carlson sold his stake in the company on June 10. And Newsmax, the conservative TV network and website owned by another presidential confidante, Christopher Ruddy, got a loan worth $2 million to $5 million....

Albright Stonebridge Group, the Albright firm that declares itself “the premier global strategy and commercial diplomacy firm,†took a loan totaling between $2 million and $5 million....

Notable campaign vendors on both sides of the political aisle also managed to secure PPP loans

The article runs on and on with names.

Lesson to be learned ... again

You can't expect big banks and other global corporations and members of congress and people with high administrative and congressional connections not to come running when Father Fed and Friends holler "Sooooie!" on a multi-trillion-dollar feeding frenzy of free Fed funds and taxpayer debt.

Almost daily, new major transactions are announced, many of them connected with "blank check" deals that help to generate lots of wealth, especially for the wealthy. The Federal Reserve has, once again, provided massive amounts of liquidity for the financial markets and like the period following the Great Recession that are being swooped up. So, wealth creation is being underwritten by the Fed once again, the worry being about the massive amounts of debt that are being created....

For quite a few years, my most popular article ... was one entitled “Bernanke Is Underwriting the Wealthy.â€

... what has been done will be done again; there is nothing new under the sun.