The Recession Begins! GDP Subsides, Inflation Heats up, Jobs Fall into a Pit.

The moves are not big yet, but there are good reasons for that, and they are all in the wrong direction.

According to the Bureau of Economic Analysis, real GDP just went from a positive 2.4% annual growth rate to -0.3%. It will, of course, take two consecutive quarters of the “growth” rate coming in below zero for the present quarter to be officially designated as part of a recession, which is always done retroactively after giving lots of time for all the economic revisions to come in. As it stands right now, though, we’re on track for the first quarter of 2025 to be declared the start of a recession.

The slide into recession is confirmed by the recessionary plunge in new jobs, which came in way below expectations at a net increase of just 62,000 jobs for the past month (April). Anything below about 150,000 net new jobs each month is generally regarded as recessionary because it takes, at least, that much job growth just to stay even with the rate at which population growth feeds into the labor pool of those wanting or having jobs. That was down by more than half from the previous slouching month of 147,000 and missed economists’ expectations of 120,000 by about half, too.

I said earlier that I would not have been surprised to find this quarter did not quite go negative because of the huge flood of businesses and consumers who are rushing to front-run the Trump Tariffs. I know I was one of them, deciding to move my purchase of a vehicle up about a year from where I was originally anticipating because the … well, the old buggy now had 260,000 miles on it, so it owed me nothing, as I had put almost nothing into it during the time I owned it. Because I bought it used at a good price five years ago, I may even sell it for more than I bought it for as I hold it to see if tariffs drive used-car prices up, which I believe they will do. As its replacement, I bought a 2015 Jeep Grand Cherokee in cherry condition, loaded with options, with only 55,500 miles on it for $16,500 because that was already a fairly good deal in the region where I live, rather than risking a higher price later.

You can multiply that kind of front-running all across the nation as people buy whatever they know they will need now or will soon need or just want badly enough to use tariffs as their excuse for jumping in now. That had to be a huge boon to real GDP, and we can suss that out if we parse the numbers carefully. Unfortunately, most people do not understand at all how to parse the import-related part of GDP. Even some economists get it wrong, though the Fed and the BEA have spelled it out carefully for anyone who chooses to read carefully.

Let’s start with Trump’s Tradesman, Peter Navarro, who classically gets it completely wrong to his own team advantage, and then I’ll explain for those who remain mystified how this actually works why he’s wrong. Too bad we either don’t have a trade representative who understands or we don’t have one who cares if he lies. I can’t say which because I truly have no idea.

White House trade advisor Peter Navarro brushed off concerns Wednesday about the unexpected drop in U.S. gross domestic product last quarter, saying, “We really like where we’re at now,” and pointing to a surge in new domestic investment.

“I got to say just one thing about today’s news, that’s the best negative print I have ever seen in my life…. The markets need to, like, look beneath the surface of that…. We had a 22% increase in domestic investment,” he said. “That is off the charts when you strip out inventories and the negative effects of the surge in imports because of the tariffs, you had 3% growth,” Navarro said.

Talk about spin! “Best negative print” is the best he can say, and it was only the best negative because of that huge surge in front-running tariffs, as I’ll explain below. Zero Hedge, now a shill for all things Trump, makes the same mistake, claiming that, without the front-running in imports, which get subtracted from GDP, GDP would have come in at a strong 3% growth. That is complete balderdash if you understand how the numbers work, and it’s inexcusable for an economics site of that kind to not realize that. I think they do and are just beguiling their readers with Russian confusion.

So, here is how it works

If you are an honest person, and you want to dismiss the negative impact of imports and tariffs on GDP, then you also have to dismiss the positive impact that is hidden in the numbers. The positive part is that whopping 22% increase in domestic investment and the huge increase that happened in retail sales. You see, ALL of those imports the BEA subtracts out of GDP were, first of all, included in that huge surge in domestic spending and inventory builds and retail sales etc. If you didn’t have all those imports, which show up as being a negative line in GDP, you also wouldn’t have had them included in all the positive sales figures. Imagine how much smaller those sales would have been if we had no imports to sell!

Most of the huge surges mentioned for sales happened because of the front-running of tariffs, which Team Trump takes as a positive for them, as is fair. What Navarro and ZH are not telling you (on purpose?), however, is that the front-running of imports they are talking about has to show up somewhere in all the positive numbers because most of the stuff people and businesses are buying is imported or, at least, made partially from parts that were imported.

Because it is virtually impossible to figure out with every product bought in all of those sales what portion of the product was made from imports and, therefore, what portion of the sale’s price should be considered due to imports and not domestic production, the government does this calculation in a very simplified but reasonable manner, given how nearly impossible it would be to run the actual numbers: They count the FULL sale price of everything that was added to inventory, consumer sales, domestic investment, etc. as being DOMESTIC production. Then …

Of course, imports are NOT domestic production, so counting them would give the US a huge GDP gain all the time for stuff it didn’t actually produce because, as we now all have certainly heard, we import a lot more than we export. So, in order to strip FOREIGN production back out of total US Gross Domestic Product, the government subtracts out all imports that came through US ports and boundaries as a single line-item adjustment based on manifests or bills of lading that state their wholesale value.

They have NO IDEA what all of those imports went into and no record in GDP of what they even were, but they know those imports all went somewhere into that vast sea of positive sales figures for the economy. The logic is that, if you subtract out what was paid for imported items as they crossed the border, you collectively negate their addition to total GDP, even though all the component measures in GDP have the value of those imports included in them. It is purely a reconciliation figure to the bottom line.

So, nothing is lost from GDP when you reconcile those imports back out, BECAUSE imports are not domestically produced and have no business being a part of GDP in the first place.

People see that and think imports are hurting our GDP. Not at all. They actually enhance it a lot, even after the wholesale price is stripped out, because the retail sales include the full marked-up value and the only thing you’ve stripped back out is the retailers original cost. The rest is value added that the US gets credited for, which wouldn’t have happened without those imports.

So, when someone says, “GDP would have been much higher if not for all the imports that got subtracted out,” they are either lying or ignorant because the truth is that all the positive inputs to GDP would also have been much lower by that same amount if imports were never included in all the final sales used to measure GDP in the first place.

There is, of course, one caveat to all of this that muddies the picture. Imports do not necessary come into port or cross boundary lines in the same month or even same quarter in which they are sold over retail counters, car lots, etc. Take, for example, that Jeep Grand Cherokee I bought. It came out of Canada half a year ago, but just sold to me a couple of weeks ago. The dealer wanted way too much for it, and finally put a clearance price on it on the day I bought it (and then I talked that down).

So, while this all averages out neutral over many months, there will always be some port figures subtracted out in a different quarter from the one in which those products actually made it to the shelves and got sold. Retail sales of imports obviously lag the day they were imported, but that can vary from a couple of weeks to several months. There is a caveat to that, too, because they do get counted in reported inventory, even if not sold to the final consumer yet, but only at the level of their wholesale price that was paid. So, the cost gets neutered almost right away with a buried plus and an evident minus on each side of the ledger, but the profit from the sale may not add in until later if the item sits in inventory awhile.

So, yes, the figures carry distortions that level out over enough time. However, we know from the figures given that retail sales really surged and so did inventories, so a good part of those imports that surged through customs and got reconciled back out of GDP had to be part of the retail surge that added to GDP. Even if it wasn’t the actual same inventoried serial-numbered import that sold, it was a positive sale that happened because of the front-running surge, so the surge is contributing huge positive numbers at the same time that the rise in imports crossing the border is surging. We don’t know how precise the matchup in timing is with all of that and cannot know that, but it appears to be reasonably inline because the huge positive impacts on GDP from sales happened at the same time as the huge negative reconciliation.

At the end of the day, the goal is to reduce the positive contribution to GDP from imports to leave only the value added by the retailer's’ services in finding, shipping, storing, then displaying, advertising, heating and lighting, and providing all the real estate and people to make that happen. That part is all domestic production of services, while the actual imported item is not. That huge volume in sales would not have happened if we did not have massive amounts of imports to sell.

In conclusion

Finally, with all of that, we know that impact of on-again/off-again/much-more-on-again/partially-off-again tariffs can only have been playing through in March. January was the Biden economy, and Trump was just getting tariffs started in February, which he largely put on hold. So, the real tell will be in what happens next quarter, though some of these lag effects will still be playing through.

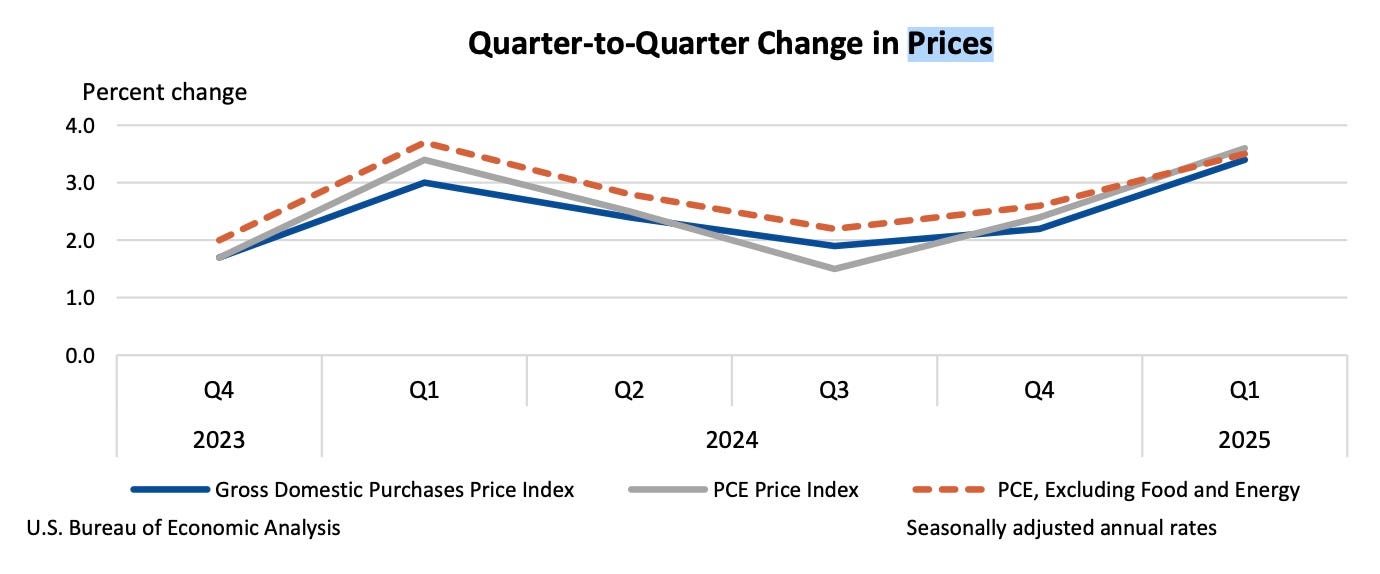

According the BEA, inflation also rose significantly, as I’ve been predicting here:

The price index for gross domestic purchases increased 3.4 percent in the first quarter, compared with an increase of 2.2 percent in the fourth quarter. The personal consumption expenditures (PCE) price index [the Fed’s preferred gauge] increased 3.6 percent, compared with an increase of 2.4 percent. Excluding food and energy prices [core PCE, the Fed’s ultimately preferred measure], the PCE price index increased 3.5 percent, compared with an increase of 2.6 percent.

Those are pretty big jumps that take us higher than we’ve been in over a year. Of course, this inflation gets subtracted out of raw GDP to get to “real GDP” because, in measuring gross domestic product growth, we’re interested in sales growth (but as measured by dollar value), so we want to make sure we are not just measuring the increase in price due to the loss of the dollar’s value).

So much for the always-lame argument that tariffs do not cause inflation, and we are only barely getting started with really only about a month of tariffs in the bag and the lag times for those, too.