What Will the Fed Do, Part Two

That didn't take long! After posting yesterday that the Fed would try to save the stock market with more rate cuts and more QE that wouldn't work, the Fed overnight seriously upped the amperage on its QE repos. And it didn't work spectacularly! That is to say, it was a total face plant in terms of the stock market. There has not ever been a more spectacular financial fail.

I refer to these as "QE repos" because they are continuously rolling over exactly as I said they would from the start until they are (as of late) converted into quantitative wheezing, which is what we should perhaps call QE that is "not QE" according to the Fed and that also doesn't work anymore.

The New York Fed's statement regarding its shocking "not QE" jolt to the overnight and term repo desk read as follows:

The Open Market Trading Desk ... at the Federal Reserve Bank of New York has updated the current monthly schedule of repurchase agreement (repo) operations.

Beginning with today’s operation and through March 12, 2020, the Desk will increase the amount offered in daily overnight repo operations from at least $100 billion to at least $150 billion. In addition, the Desk will increase the amount offered in the two-week term repo operations ... from at least $20 billion to at least $45 billion.

Consistent with the FOMC directive to the Desk, these adjustments are intended to ensure that the supply of reserves remains ample and to mitigate the risk of money market pressures that could adversely affect policy implementation. They should help support smooth functioning of funding markets as market participants implement business resiliency plans in response to the coronavirus.

As the biggest of repos during the entirety of the Repocalypse, this may have helped stabilize money markets, which subscribed to $112 billion worth this morning, BUT it sure didn't help the stock market, which took its biggest intraday point drop in history -- Dow down more than 2,000 points!

So, the first count in my case was proven in just one night: Expansion of QE via repo isn't going to save the economy or the market anymore. We are clearly at the critical juncture I spoke of in that last Patron Post.

Meanwhile, the market also priced in a Fed reduction in interest rates of 100 basis points by April, meaning the market is expecting the Fed to hit the zero bound by April. That means anything less than that will be "disappointing" and will be met with disapproval at the stock exchange.

Therefore, the second count in my case (that interest-rate cuts have hit the level of diminishing returns where they will now be ineffective) has been proven overnight, too. Anything less than plunging to the zero bound on the Fed's part will result in further market disturbance; and, of course, interest cuts will do nothing to aid a breakdown in supply chains or stir an economy where people all over the world are being commanded to isolate themselves due to a virus.

So, as I said in that last Patron Post, the Fed may continue to try some of its old ammo because it doesn't know what else to do that it CAN do, but it is now finding the old ammo is all past its shelf life, and its powder is all wet. The Fed is backed up to the Law of Diminishing Returns.

Meanwhile, people today were panic-searching Google for "Black Monday" as market circuit breakers were tripping to stop the fall for the first time in years. "Market halt" was reportedly a popular term today, too; but the Donald was enjoying a nice round of golf, so he must have been confident that his Plunge Protection Team would carry out his bidding. But that didn't work either!

All of this brings us in just one night back to the question of ...

What does the Fed do now?

The Fed's next brightest plan, after the failure of QE and interest cuts appears to be moving to outright purchases of stocks. We've already seen in the last post how that has not worked sufficiently when the Fed used proxies to make those purchases (or when CBs stepped in for their own reasons, whichever was the case).

Imagine, though, what the Fed could do if congress gave it permission to purchase stocks directly. That might not be an easy sell to congress until the financial situation becomes dire, but the situation will become dire ... quickly. With unlimited money-creation capacity, the Fed can keep any falling stock market up for as long as it wants. All it has to do is buy every stock that is falling at its current price and buy as much as it takes to keep it there. It can even buy the stock price up, even if that means being the only buyer in the market. And it never has to worry about whether it loses money on these stocks later because profit is meaningless to an organization that has the sole national power to create money at will.

But is the Fed interested in taking the market into receivership by absorbing private industry into the Fed's own centrally owned economy like a giant ameba? Can they overcome public resistance to such ownership? (The answer to the latter is probably only if they set limits and promise congress that it is a "temporary" solution to the current covidcrisis and if the public is desperate for salvation at any price.)

With US$2.5 trillion wiped off the face of the earth in global stocks, it may not be long before this crash overcomes that barrier to total Fed manipulation of the market via hostile takeover. Today gave us the worst market plunge since the start of the 2008 Great Financial Crisis. In point drop, it was the worst in the history of the stock market. So, that sets in motion the needed sense of desperation with a deadly virus crawling into our lungs at the same time.

Right now, the Fed will not likely encounter more than lip-service resistance to gaining this new power. (It's not even clear it needs congressional approval, though congress could certainly stop the Fed if it wanted to since it operates at the pleasure of congress via its charter.) After all, the Donald wants his badge of success -- the stock market -- to do him proud throughout the length of his campaign, and Republicans want to help the Donald at any conceivable cost, lest they lose the White House to the Dems. (It's always party before country with both of these self-serving assephants -- what you get when you cross a donkey with an elephant.)

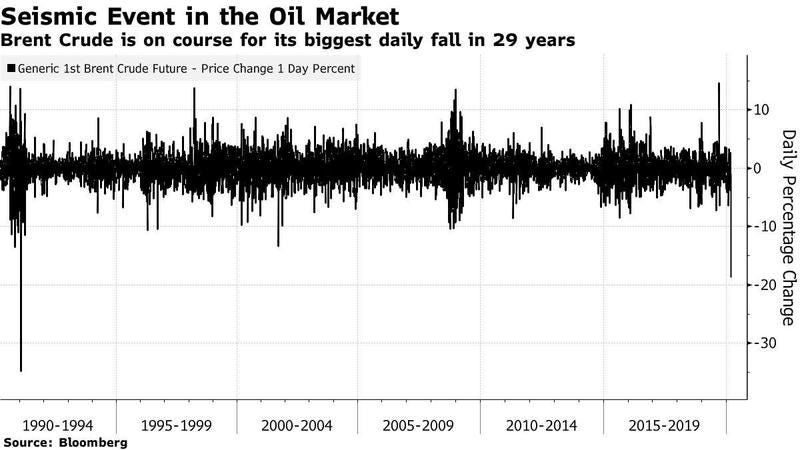

Oil lost $16 a barrel over the weekend, cratering at the open to $27 a barrel. By the end of the day, it settled at $32. That opening number was a 30% plunge overnight! That takes us back to the days of the gulf war to see that kind of price swing. Wow! This was a day of disasters all over the place….

I recall the huge upward price swing of the 1970’s oil embargo that sunk the US into a long recession by creating massive inflation in the price of everything. A price swing this size in the other direction can also cause a recession in today’s junk market in a much different way, which we saw today. The overnight oil crisis exploded into carnage on Wall Street because many oil-related companies have already taken on all the cheap credit they can afford, so they’ll die quickly with oil falling far below what they need to maintain their debts, which were already rated as junk.

Oil did this because Russia and the rest of OPEC broke off negotiations to reduce oil supply, turning their pumps up all the way, while the coronavirus is shutting off the demand valves as factories slow down. It looks like the coronacrisis just shifted into a crudecrisis, making this now a full-blown, multi-faceted crisis. That combined with more news over the weekend about parts of Italy shutting down and more corona deaths (Aye corona!) kicked the legs out from under a stock market already struggling to catch down to the economy.

Crisafulli explained in a note just how critical oil is to the U.S. economy....

“The sector is like the ‘FANG’ of credit, esp. high yield, given the enormous amount of debt it has outstanding,†he said. “As a result, the implosion of crude prices delivered a major blow to fixed income over the last 72 trading hours, exacerbating overall market panic.â€

And that's how the Fed failed to improve anything with its major overnight and term repo revisions. With the real economy -- not just stocks -- overwhelming the diminished potency of the Fed's normal tools, we've arrived in one night to the place where we need to look back at what the Fed has said about buying stocks directly (and why not oil, too, while they're at it ... or just soak up oil companies and create money for them to pay their debts). When you have infinite money creation powers, you can buy as much as you want of everything to rig prices back up. All possibilities are on the table now. Some will require congressional approval.

Where does the Fed stand now on buying stocks directly to prop up its beloved and beholden market?

Three weeks ago, former Fed Chair Janet Yellen incepted the idea that during the next crisis, the Fed should consider expanding the range of assets it would purchase, most notably buying stocks. Our comment to this was that "thanks to Janet Yellen, we now ... know that before the current fiat regime of central banks finally ends and before stocks go limits up as the revolution starts, the Fed will order a POMO of, well, everything in one final, last ditch effort to keep social stability by creating the impression that stocks are stable and rising even as society implodes."

More recently, Boston Fed President Eric Rosengren chimed in to support Yellen's plea:

In a situation where both short-term interest rates and 10-year Treasury rates approach the zero lower bound, allowing the Federal Reserve to purchase a broader range of assets could be important....

Such a policy, however, would require a change in the Federal Reserve Act. … Alternatively, the Federal Reserve could consider a facility that could buy a broader set of assets, provided the Treasury agreed to provide indemnification.

We are now rushing headlong for the zero bound on the 10-year treasury, which briefly touched 0.34% early this morning. So, the zero bound could be only days away. It sounds, though, like the Fed wants some sort of insurance policy from the US government in addition to permission before going down this road and like it probably does need some sort of permission.

Clearly direct stock purchases, as seen already in Japan, are being considered, but I pointed out yesterday that we also already know those have very limited effect in propping up the economy based on what we've seen in Japan's secular decline. The Fed is aware of this. But stocks are a tool they may reach for in desperation.

Is there any interest in negative interest?

The Boston Fed also noted,

Goodfriend suggested that negative interest rates might be an effective policy tool in some situations – but Rosengren remains skeptical, saying the experience in Europe and Japan shows the adverse side effects are likely quite large.

You see, the Fed is are already catching on to the worthlessness of negative interest, as said in my Patron Post yesterday. This is realization of the reality that their old ammo just doesn't work if it has to go lower than the zero bound. They are slow, these central bankers, but they do eventually catch on to things some of us saw as a guaranteed outcome more than a decade ago when the Fed first started down this path -- back when I was endlessly saying they had no end game.

Now we clearly see they did not and still do not. They are scrambling to figure one out and patching in desperate attempts with their old medicine as they did last night in repo to no other effect than to keep the repo market calm in the midst of this crisis.

So, we are hitting the zero bound where plans have to change ... even in the Fed's mind. We also saw in past Patron Posts that central banksters were realizing that going ZIRP or NIRP wasn't going to get us any further:

I am sure they must be as smart as we are to know that QE and negative rates cannot go on forever.... Not everyone wants to park money in banks where they are charged a storage fee....

To manage the negative-interest stresses that are starting to build all over the world now and keep the merry-go-round spinning, central banks will inevitably need to move out of hard cash that you are able keep outside of a bank just to close off that option.

CBs are not ready to move out of hard cash yet, though they are getting ready. They have already said moving out of hard cash for the sake of enforcing negative interest rates is not a reason for moving out of cash Many people think the banks need to go cashless in order to be able to push interest rates negative, but the Fed doesn't want to go negative. Various members of the Fed have spoken out quite plainly against going negative or going digital for the sake of enforcing negative interest:

CBs shouldn’t go digital just for the sake of being digital or just to be able to drive down negative rates.

To which I replied ...

Of course not. They should do it for monetary control, which does not necessarily require negative rates. If banks can get people to move money without pushing them via negative interest on their money, I’m sure they would prefer to avoid the problems of negative interest, which are manifold; but how can they do that?

Going cashless is about monetary control. Banks have no desire to take on all the problems of going negative. However, the crisis came early, thanks to a little virus, and central banks are far from ready to go digital.

I noted in that same Patron Post that Adam Posen, President of the Peterson Institute for International Economics, and a great friend of central banks has pointed out the negatives of going negative:

I think Adam Posen sees that negative interest rates are going to cause all kinds of other problems and believes central banks can find better ways of manipulating their currencies and their economies. So, he may be genuine in saying that CBs need to stop thinking of CBDCs [Central Bank Digital Currencies] from that perspective. Once the central banks have total control over your use of money, they may not even need negative rates in order to effect their monetary policies or their economic stimulus goals. (If they do, though, they will certainly have that power; and without that power, negative interest is just killing banks.)

...I think Brainerd and Posen are seeing it right when they try to clear that argument away. After all, why are negative rates currently necessary? They are an effect of the central bank’s efforts to finance their governments by monetizing debts and to stimulate economies with lots of new money; but they are clearly not creating much stimulus because the economies that are the most negative are in worse and worse shape. So, they are starting to lose that reason for being, except that, once there is a lot of debt resting on them, you become pressed to maintain them. Negative rates are not inherently desirable to banks, which are still figuring out how to work with them. Banks have struggled under them and do better when there is a good positive interest spread that they understand....

Consider the downsides to negative rates that can be avoided if digital currencies give banks the ability to manipulate monetary policy without creating negative rates:

The Japanification of the world is now essentially complete with most central banks on a path of easing forever. The Ponzi scheme that will blow up if negative rates normalize is unbearable. From the banks’ standpoint, that may be seen as both an argument for keeping them out of necessity now that they are so prevalent but also for getting off this path before it becomes worse.

There is much more that can be mined about negative rates in that Patron Post, which goes deep into the pitfalls that central banks want to avoid. Without rehashing that, I just wanted to bring back to awareness the essential fact that central banks don't want to go negative for many reasons. It is just what happens if they get all the way to zero in trying to carry out their duty to stimulate their economies and that the Law of Diminishing Returns gives them no bang for the buck. They have tried pushing rates down further (below zero) and have found it was detrimental in almost every way, even some ways they didn't expect:

Going negative resulted in slowed — almost frozen — money markets, causing overnight funding to coagulate [certainly not a problem they want to perpetuate in the middle of repo crisis].... Of equal concern, the nearly frozen money markets did not thaw when the ECB temporarily ended its QE....

Banks became less profitable, not more profitable ... because banks were unable to pass negative rates on to their customers....

Pension funds became less profitable....

Greater income inequality resulted....

Reduced credit creation in the real economy came as a surprise. If the goal is stimulus, it backfired.... [This was completely contrary to what CBs that went down this path expected. Remember what I said in the last post about hitting a point where diminishing returns actually go from diminishing to negative, actually worsening the situation rather than just not making as much difference to the good as they used to earlier in the curve?]

In Denmark, it has resulted in mortgages that pay you money to service them to maturity....

Another bizarre result was that negative rates resulted in higher stores of savings, not in less as people thought would happen. No one knows why. It just did.

So, there are many reasons it is not in the best interest of bankers to take interest negative. NIRP IS OUT. (Except that it may happen in spite of the Fed if bond vigilantes keep driving bond interest down on their own.)

Negative interest heightens the risk of policy errors in a universe where bankers don’t even know how to function efficiently. Things don’t seem to move in the direction you intend to send them by your actions in the negative universe.

But don't just take my reasoning for it. Let me recall to your mind the words of the big central banksters, themselves, on this subject from another Patron Post:

Fed Chair Jerome Powell has said the Fed will never go negative on interest rates. In response to President Trump’s response to go negative, Powell said in September,

"Negative interest rates is something that we looked at during the financial crisis and chose not to do. We chose to—after we got to the effective lower bound---we chose to do a lot of aggressive forward guidance and also large-scale asset purchases, and those were the two unconventional monetary policy tools that we used extensively. We feel that they worked fairly well. We did not use negative rates. And I think if we were to find ourselves at some future date again at the effective lower bound—again, not something we are expecting—then I think we would look at using large-scale asset purchases and forward guidance. I do not think we’d be looking at using negative rates. I just don’t think those will be at the top of our list."

"The Whacky Wonderland of Sovereign Debtors and their Central Banksters"

There you have it: they lean more toward large asset purchases. That's more QE -- so QE4ever as I've said -- if by "assets" he means bonds, but now we see the Fed is also leaning toward direct purchases of stocks (in the words above of Yellen and Rosengren.

To Powell's comment, I added my own, which I think has just become completely apropos:

I think the next situation will be one that requires bigger tools. By then the Fed should also have finally become apprised of the obvious, which is that their old tools did not create anything durable.

There is a lot more about going negative in that Patron Post, too, and there is certainly always room for Powell to flip flop on not going negative. The Fed, however, didn't go negative before, but stopped for a long time at the zero bound and watched others go negative and fail. So, I don't think it will go negative now that it sees that even lowering interest rates did nothing but crash stocks a week or so ago, and juicing up repos last night did nothing but crash them again. We have clearly reached the point where old tools are now have negative results.

So, the Fed is going to have to bring out bigger tools that worn-out interest cuts. The obvious options we've discussed outside of NIRP, which even Powell doesn't like, are ...

1) more failing QE (probable in the immediate term where it is demanded to avoid a huge resurgence of the Repo Crisis, but no longer effective for stocks just because it is something they are adept at),

2) large asset purchases that have to include stocks directly if they are not just going to be more QE that is further down the curve of diminishing return (which the Fed has indicated will require congressional approval and which could see huge negative public reaction), and

3) the creation of Central Bank Digital Currencies, which will give CBs total control over money:

Going cashless

First, it's not ready yet, and it's not as easy as it sounds, but the big boys already have it coming!

Reaching back to another one of our Patron Posts, which were always intended to lay the path to get us to where we are now:

BIS General Manager Agustin Carstens gave a speech at the Central Bank of Ireland 2019 Whitaker Lecture. Under the heading, “The future of money and payments,†Carstens mapped out what has been a long standing vision of globalists – namely, to acquire full spectrum control of the international financial system through the gradual abolition of … physical money…. Carstens explains that the current system of central banks issuing banknotes, and commercial banks providing electronic money, is being targeted for reform – in the shape of central bank digital currencies (CBDC’s). A CBDC would allow ordinary people and businesses to make payments electronically using money issued by the central bank…. That would mean that you and I could open bank accounts directly with the central bank….

"I am particularly interested in the implications for central bank money and what so-called central bank digital currencies (CBDCs) would mean – not just for the system, but for all of us as citizens."

"DIGITAL CURRENCY: The Central Bank Rush toward a Global Cashless Society is on and Very Public!"

There is a whole lot more about that in the Patron Post just referenced if you missed it because you were not Patron earlier or want to refresh yourself. For this summary of where we are, quotes from one more major central banker should suffice to show how badly CBs want this solution:

Christine Lagarde, IMF Managing Director, wholeheartedly agrees:

I would like to … evaluate the role for central banks in this new financial landscape—especially in providing digital currency….

For Lagarde, now head of the European Central Bank, the hold up is not social resistance -- as people once thought was the big limiting factor on going digital -- but technical readiness:

You—young and bold entrepreneurs gathered here today—are not just inventing services; you are potentially reinventing history. And we are all in the process of adapting....

A new wind is blowing, that of digitalization. In this new world, we meet anywhere, any time…. Money itself is changing. We expect it to become more convenient and user-friendly, perhaps even less serious-looking…. We expect it to be integrated with social media, readily available for online and person-to-person use, including micro-payments. And of course, we expect it to be cheap and safe, protected against criminals and prying eyes. What role will remain for cash in this digital world? Already signs in store windows read “cash not accepted....â€

Let me be more specific:... Various central banks around the world are seriously considering these ideas.... They are embracing change and new thinking.

Make no mistake about it, central banks are fully on board with going digital, and they are open about it as they believe society is ready. Lagarde sees a world where cryptocurrencies are inventing the technology, but central banks will be needed to regulate it and administer it:

For their part, cryptocurrencies seek to anchor trust in technology. So long as they are transparent—and if you are tech savvy—you might trust their services. Still, I am not entirely convinced. Proper regulation of these entities will remain a pillar of trust....

You needn't worry, then, about central bankers inventing the technology behind the scenes. They know they are not technologists, and they know the free market will experiment with numerous ideas until one platform rises to the top. Then central bankers will take over as the regulators, and they will have the backing of the their marriage partners -- governments -- to do this.

For a start, private firms may under-invest in security to the extent they do not measure the full cost to society of a payment failure. Resilience may also suffer—with only a few links in the payment chain, the system may stop working if one of these links breaks. Think about a cyber-attack, a glitch, bankruptcy, or a firm’s withdrawal from the local market.

In other words, a true global digital currency (or many national digital currencies) needs the robustness of a central bank behind it and managing or regulating it to imbue trust and assure smooth global transactions and full regulation. So, what is holding them back on this?

Carstens answers that quite simply for us:

The monetary system is the backbone of the financial system. Before we open up the patient for major surgery, we need to understand the full consequences of what we’re doing….

Central bankers have no need to be first out the gate to beat cryptocurrencies. They have the full power of government at their backs when the right system is available for modification.

Mark Carney, governor of the Bank of England, leaned more transparently global in one of my past Patron Posts than Lagarde's "various central banks around the world" developing or regulating their own independent CBDCs by speaking of developing "a network of central bank digital currencies."

He also said,

While the rise of the Renminbi may over time provide a second best solution to the current problems,… first best would be to build a multipolar system.... While the likelihood ... might seem distant at present, technological developments provide the potential for such a world to emerge. Such a platform would be based on the virtual rather than the physical.... Retail transactions are taking place increasingly online rather than on the high street, and through electronic payments over cash.... Let’s end the malign neglect of the [international monetary and financial system] ... and build a system worthy of the diverse, multipolar global economy that is emerging.

It's easy to see how all of these central bankers are speaking the same digital language. Concerned about US dollar hegemony, Carney even proclaimed this "could dampen the domineering influence of the US dollar on global trade." (Something many nations would love to see.)

Those are just a few of many quotes from pervious Patron Posts showing the rapid and very open move of central bankers toward establishing central bank digital currencies. Review them at your leisure to capture the broad strokes in just the past two years. So, this big ammo is definitely arriving soon!

In fact, speaking of the Renminbi, China is already rushing forward with this, even as the Fed takes the more sage approach of letting other work out the bugs:

As the war on cash escalates, officials from The IMF to China are seeing the opportunity to control the world’s money through virtual (cash-less) currencies…. As Bloomberg reports, The PBOC is targeting an early rollout of China’s own digital currency to “boost control of money†and none other than The IMF’s Christine Lagarde added that “virtual currencies are extremely beneficial.â€

PBOC has asked its research team, which was set up in 2014, to study application scenarios for digital currency and strive for an early rollout…. It can reduce the traditional distribution of digital currency note issue, the high cost of circulation, improve convenience and transparency of economic transactions and reduce money laundering, tax evasion and other criminal acts to enhance the central bank’s money supply and currency in circulation control, better support economic and social development, the full realization of inclusive finance help

All that's holding central banks up is letting the techno wizards get all the technology right while waiting to see what technology functions the best and how it might need to be improved. They are letting the free and creative market work its best magic. They can swoop in and take control when it is finally all ready for them because they have no idea how to create complex software. Might as well let competition work its charms./

Soon but not yet

The Fed, unlike China, I am almost certain is taking Carstens' conservative approach, which is to be cautious and let others make the mistakes as they want to see what the full consequences are. China needs to rush because it wants to be the new hegemon. Let cryptos experiment with the technology. Let China or someone else experiment with making a CB currency, and learn from their failures. You don't have to be the first fish to wake up and eat in the morning if you are already the biggest fish. You can let others do all the eating for you, then when they are fat and slow just eat them.

Carstens was less concerned about the technology than the social consequences. He said he wanted "the decline of cash [to] be perceived as organic rather than premeditated." In other words, let it work through as a demand of the people that the central banks then fulfill, rather than shoving it down their throats and creating resistance. They have time because the technology isn't there yet anyway.

There is, however, nothing nothing so opportune as a global crisis to create public demand for a global solution, as I've said all along.

Since the Fed does not seem anxious to be the first to jump in, I think it may go for large asset purchases in the stock market first. (Well, second, because it needs something immediate that also helps resolve the repo crisis, which means the extension of QE4 into QE4ever as something that will coincide the next step of stock purchases. QE is not going away because the US government has a $1.2 trillion deficit to keep financing.

I may write one more Patron Post on this theme to bring all arguments as current as possible and to cover one more big but less likely move (helicopter money), but these moves above are the ones I think the Fed is most likely (and most unlikely) to make:

No negative interest period, except what might happen accidentally due to bond vigilantes or the side effect of the following policies:

Repos and QE4 ("not QE") all rolling over, as I've said will happen to become "QE4ever" in order to finance the US debt for years to come and because number three will take some working through congress:

Purchase of stocks directly, ostensibly at first perhaps, to save zombie companies that will soon be dying because investment-grade credit will be downgraded to high-yield (junk) in the developing repo/financial/credit crisis and coronacrisis.

Last of all, central bank digital currency for which weakness of all the above in resolving the crisis now upon us will push through whatever social resistance remains.

I will be surprised if we don't make it all the way to number 4 in less than two years what with the coronacrisis accelerating everything.