Why are Bonds Going for Broke?

One argument for last week's extraordinary plunge in bond prices, which I explored as something that might happen this time of year in one of my earlier Premium Posts, was that bond prices could get crushed by the supersized US treasury auctions planned for September and October as the government makes up for its inability to issue new debt during the debt-ceiling standoff.

While pointing out the concern to patrons, I decided in the end for my own investment purposes that the Fed's termination of quantitative tightening and its return to reducing interest rates would likely offset the impact of the government's sudden debt expansion. Evidence is solid so far that the ballooning treasury auctions have not been the cause of the sudden collapse in bond prices (rise in yields).

(I also got out before the carnage of last week.)

So what caused the bond breakup?

I believe the sudden change in the bond market since September 4 has been due to a few factors.

First, the violent momentum trade in stocks in the past week became the biggest stock rollover of its kind since 1999. The change in momentum trading means investors are defensively selling off growth stocks (stocks that have been rising on a bender) and rolling the money into value stocks (stocks of good companies that have remained underpriced compared to the rest of the market). That sea-change in market factors likely forced numerous managed funds (such as risk-parity funds that guarantee a certain ratio in stock values to bond values) to sell off bonds, whether they wanted to or not, just to maintain their promised balance between equities and securities.

Second, at the same time the momentum rollover was going on, corporations leaped into the bond market with their own sudden record bond issuances to fund future rounds of stock buybacks or refine current debt at lower rates. Inflated supply means raising yields to attract additional buyers into the market. Another way to look at that is that bond prices have to fall to attract buyers.

Third, as Goldman Sachs also noted, the rotation, itself, came because...

Perceived improvement in US-China trade negotiations and better-than-feared economic data helped ease investor concern about an impending recession, lifting bond yields and sparking the market rotation.

What I've realized about the stupidity of the stock market with respect to how it rises every time Trump tweets some inane and fake promise about the end of his China trade war is that algorithms were probably not created with any ability to discern the truth value of headlines that are input into their data streams. I presume they take all data at face value. So, garbage in, garbage out.

If Trump says China is about to accept a trade deal, the algos bid the market accordingly. Since presidential headlines are undoubtedly given high weight in the formulas, that makes it easy for Trump to tweet the market up. (Of course, I also began writing because mainstream financial reporters/commentators seem to readily accept what is fed to them at face value, too. I found it frustrating how readily they would just parrot the noises they heard.)

Finally, inflation may be getting factored in. Treasury yields, especially bonds -- because they payout over long time periods -- have to factor inflation in dollar-for-dollar on top of any yield investors want to see. The bond market moves yields to track with inflation, and inflation just took its largest jump in years.

That could be due to transitory tariffs, but it's hard to say. In fact, tariffs don't seem to be the most proximate cause because inflation rose most in services, particularly financial services, not in goods sold. Inflation in services for the first two quarters of 2019 rose 5.5% year-on-year with finance and insurance having risen 32%! Core inflation rose 2.39% year-on-year in August. It's had similar YoY rises in July 2018, February 2016 and April 2012, but August's year-on-year rise was the highest in eleven years (since 2008), though still not that significant unless it continues to rise. (See Wolf Richter for more on recent inflation.)

Bear in mind, we're going with the inflation numbers the Fed uses for its decisions and that the bond market steers by, not your actual daily life effect. By those measures, overall inflation was not bad at all. Because energy costs sank, core inflation (the Fed's preferred measure) was only a little higher than its past highs. (Again, I recognize the numbers the Fed and markets steer by don't bear much resemblance to your daily reality with tuition costs, food, housings costs (poorly calculated by the Fed) and fuel costs.)

Since the bond market got a whiff a week ago of core inflation rising above its previous peaks over the last decade, maybe that added to its troubles this past week. It's possible the bond market sees an inflation trap coming where, on the one hand, bond investors have been telling the Fed interest rates need to go down more; but, on the other hand, if bond investors see inflation rising, bonds could quickly reverse to make it so the Fed cannot cut rates, lest bonds anticipate more inflation and rise even more, causing the cut in the Fed's rate to actually tighten the economy by raising financing costs. Treasury markets can exhibit a hypersensitive, knee-jerk reaction to a change in the inflationary picture.

(Note that, if inflation starts rising, the Fed's rate cuts will actually hurt the bond market because they'll be seen as being likely to drive inflation even faster. For that reason, the Fed may be less likely to cut rates because driving bond yields up to match anticipated inflation is counterproductive in terms of economic stimulus, as is inflation, itself. That would normally be the Fed's concern; however, as reported in my Patron Posts, the Fed has said it may, in that kind of situation, choose to run the economy hot if necessary on an inflation basis as running above 2% now "makes up" for inflation's decade-long run below a 2% average. However, reactive bond rates means running the economy hot in terms of inflation won't help because numerous financing costs that are particularly effected by the ten-year bond rate will also rise. If the Fed does hold back on interest-rate cuts because inflation is rising, its stock-market step child isn't going to love that and may throw a tantrum. That's why I say this could turn into an inflation trap for the Fed -- stagflation if the Fed goes one way and a stock market that is utterly dependent on Fed largesse throwing a tantrum and crashing if the Fed goes the other way.)

Bonds not bursting due to a treasury-induced meltdown

The fact that little of the current hit to treasury prices has anything to do with the larger government treasury issues can be seen in how the last three government auctions had rock-solid internals.

While yields rose ever so modestly in two auctions, the bid-to-cover ratio for all three of the last treasury auctions has been stable. (Meaning the treasury got a lot more bids than it needed to sell all the bonds it wanted to sell.) In fact, for one auction, the bid to cover was the best since June; for another it was only slightly lower than in recent months.

For the 30-year auction, the yield actually dropped to its lowest in three years!

The percentage of indirect takedowns (such as treasuries bought by foreign governments) in each auction held about the same or actually improved, leaving US dealers holding fewer bonds they have yet to sell.

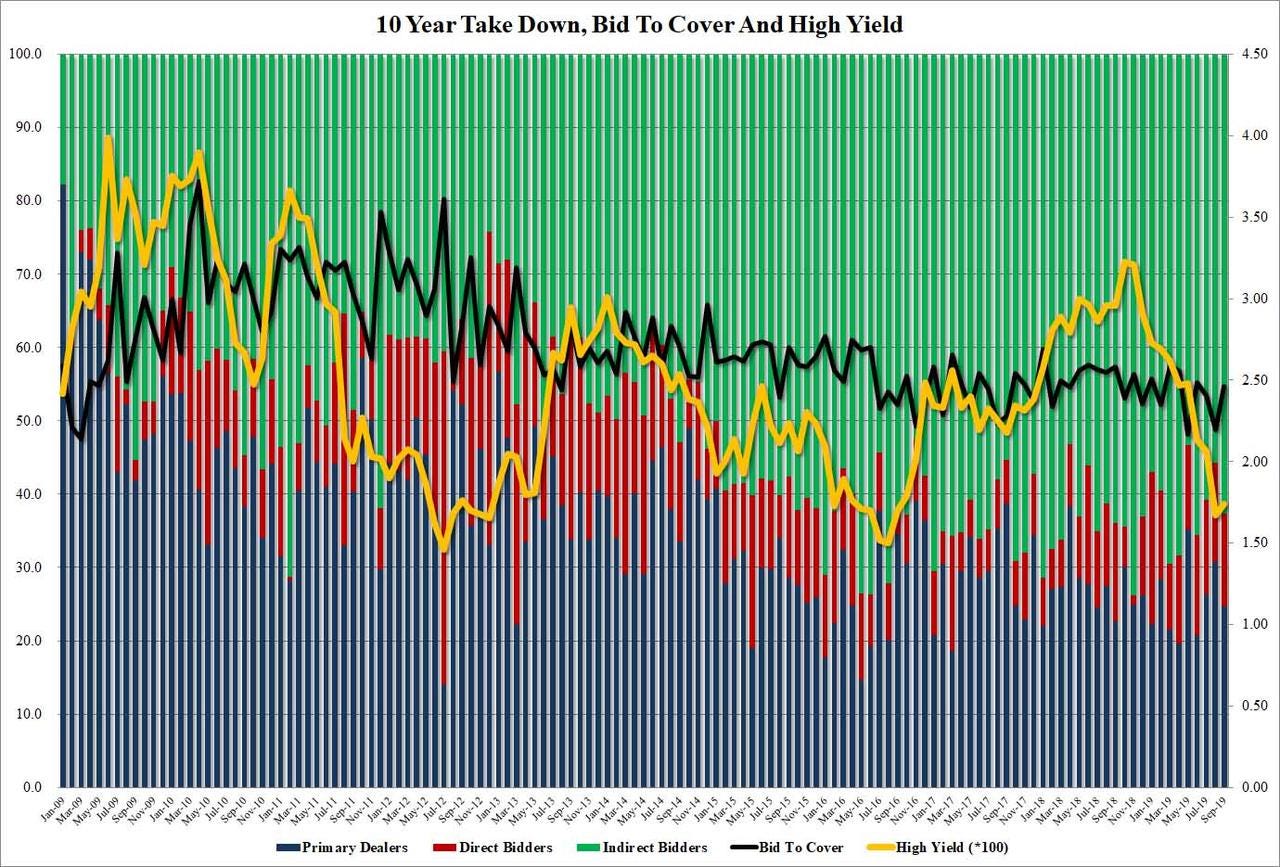

In all, a stable, maybe slightly improving picture. Take the much-watched 10-year for example:

The uptick in yields was historically slight when compared to numerous other yield moves from one auction to the next in the same graph, and the bid-to-cover actually improved.

Bearing in mind that the US Treasury stated it would accomplish all of its debt-ceiling makeup this month and next, these are good results as far as treasury auctions go.

It's a global bond breakdown

The fact that the plunge in bond prices is not constrained to the US is another indicator that the big change in the direction of the bond market doesn't have much to do with treasury auctions. The Austrian hundred-year bond, which has been trading at deeply negative rates plunged in price (soared in yields) this month, too -- so much that it entered a bear market in a breath-taking two weeks:

That looks like a melt-up where prices soar and then crash.

Likewise with the soaring problem in global negative-yielding debt, which had risen to a mountain of over $17 trillion as of August. In less than two weeks, it has plummeted worldwide to $14.5 trillion. Not a small fall for such a short time. So, something big is boiling over in the bond market worldwide.

Something wicked this way comes

Central banks are losing control, and are admitting they don't even understand what is happening.

If you're confused about what is happening, just as I am in trying to sort out where all of this turmoil is suddenly coming from, you're in big company. James Bullard of the St. Louis Fed is also confused and seemed to admit recently that even the Fed doesn't know what to make of the financial changes now playing out in the world:

The developed world had experienced a “regime shift†in economic conditions, James Bullard, president of the St Louis Federal Reserve, told the Financial Times. “Something is going on, and that’s causing I think a total rethink of central banking and all our cherished notions about what we think we’re doing,†he said. “We just have to stop thinking that next year things are going to be normal.â€

There is, in other words, no normal in our foreseeable future.

Even the central bank's public narrative sounds confused. "Something is going on" does not exactly reassure one that central banksters have any better understanding than the rest of us about what is happening in their realm of finance.

You either have to believe they don't understand the monster they've created (as Bullard sounds above) or that they are beguiling us into thinking they don't know what is happening (making themselves look foolish) even as some insidious masterplan to crash the world plays out -- the 4-D chess view. (As my readers know, I'm of the former camp; but either way gets you to the same serious trouble dead ahead.) The best one gets to, taking Bullard's words at face value, the CBs are flying by the seat of their pants as they try to figure out why normalization of their policies proved impossible and scrambling to figure out what to do from here.

The banks appear to be losing control of interest rates and to be, themselves, controlled by market forces they can no longer contain or fully manipulate. Their policies clearly did not perform as promised, yielding a weak and unsustainable recovery that greatly widened the gap between rich and poor; yet they are already going back to them as if they will create anything more sustainable than they did last time. Our foolish leaders show all signs of being ready to go along with that, and certainly stock market investors are begging for it. Bond investors have, until recently, been pushing for it. CBs are going back because addicted markets demand it. (I'll be continuing to explore the new emergency plans the CB world is plotting in the Patron Post I'm working on now.)

Even more peculiar than the admission above is the sound of banks that most benefited from the bankster bailouts of yesteryear now complaining that the changing financial world is the Fed's fault due to its recovery efforts. Listen to Bank of America's disingenuous complaint:

Ultra-easy monetary policies have led to distortions across various asset classes.... It [the Fed] also stopped normal economic adjustment/ renewal mechanisms by for instance sustaining economic participants that would normally have gone out of business....

You mean like Bank of America? Economic participants like Bank of America and its ilk might have gone out of business --as they should have -- if the Fed had not wrongfully interfered to sustain them (because they were "too big to fail").

Find that an oddly candid admission? BofA goes on to even more bizarre admissions:

We fear that this dynamic could ultimately lead to "quantitative failure,..." which would in all likelihood lead to a material increase in volatility.... At the same time, and perhaps perversely, such a sell-off may prompt central banks to ease more aggressively, making gold an even more attractive asset to hold."

O.K. I'm sure I never saw that coming. Talk about things you never thought you'd hear a major bankster say: "Buy gold; it may soon be worth more than our money." That is the world we have now entered, which should tell you all you need to know about how perilous the present times are. Banks stating publicly that CB policies, if continued, will likely be a "quantitative failure" and will make gold more attractive than bank money? (And the banks are now set on continuing them with the European Central Bank having just led the new charge.)

As I've said for years, the Fed's recovery plan never had an endgame, so the central banks are scrambling for an end game as their recovery crumbles into a myriad pieces, causing the banksters, themselves, to realize they may be facing "quantitative failure." This clear failure that is already playing out led the head of foreign exchange at Deutsche Bank to boldly ask all kinds of stark questions at the recent Jackson Hole central-bank symposium:

Will the Fed/ECB buy equities? How far are central banks willing to distort underlying value, or is distorting value intrinsic to Central Banking as per the Austrian critique? How much are Central Banks going to be complicit in a collapse in fiscal standards, by buying public sector assets...? Has asset inflation hidden an even more meaningful deceleration in the natural rate of growth that will evident in the next decade? Is it the Central Banks job to do away with business cycle? And at what price? Are we witnessing ... a great collapse in confidence and wilder big credit cycle, and greater long-term misallocation of resources?

Whoa! Those are some amazing questions for a high executive at one of the world's largest failing banks (and one of the largest beneficiaries of central-bank largesse) to be asking. It would seem big banksters all over the world are now starting to see the problems manifest that I have always said were baked into their recovery plans. There is nothing happening in these realizations that was not posited on my site as a definite endpoint to the recovery plan we have been on.

The only hard part is sorting out whether the major moves in bond market right now mean the bond bubble is bursting or are something more benign. The certain part is the failure of central-bank recovery efforts and the banks' current public struggle for direction along with their oft-stated concern about maintaining public confidence as their failures play out. Why should the public trust their next plans? (Obviously, it shouldn't, but it probably will enough to allow them to happen, albeit with a lot more suspicion that makes those plans, as I've said from day one, all the more problematic in terms of efficacy.)

It's interesting to see so much of what I've been writing about for so long now coming about. It's also unfortunate.

Whether the present bond turmoil is the beginning of a glacial bond breakup or is just due to the rotation in stocks and trade concerns noted above, I don't know. I'll just say we had all better watch and be wary when even the biggest banksters can only say "something is going on" that may "likely" lead to "quantitative failure!" Maybe all will be fine soon in the bond world again, or maybe this great glacial ice flow is beginning to roll over -- and we just don't know that's what is now happening because we've never witnessed something this big in order to know what it looks like!

On a related note, I’ll add that the sudden steepening of the yield curve that came about because of the past week's bond carnage is makes my recession predictions all the more likely. As I’ve stated in a couple of previous articles, inversion of the yield curve cocks the gun for recessions, but the reversion back toward the norm, pulls the trigger.

Yes, recessions follow yield-curve inversions, as everyone now knows, but not before the yield curve reverts back toward normal. In fact, I’d say this is the penultimate forward indicator that needed to come in for my summer recession prediction to come about. (The ultimate being the first upturn in unemployment, which is also putting in signs of emerging soon.)

Whether the massive global bond bubble crashes first or the massive US stock bubble has always been a conundrum to me. What is not in question for me (at least, not much) is the recession we are entering and that the recession will take down stocks.

One reason I'm less sure of how and when the bond bubble finally implodes is that a recession may breathe new hot air into the bubble as the Fed reverts to more ultimately failing QE and interest-rate reductions. That QE will without a doubt be much less effective so may not last long before the Fed has to switch to even more drastic manipulations and controls, as I am teasing out this year from the central banksters' own words.