Zero Hedge Confirms Fed is Dead

It is always good to have a statement from the coroner when pronouncing death as I did on May 19, 2020. That is when I gave time of death and pronounced "The Fed is Dead." You especially want the second opinion when you're talking about Feddie Krueger, who has more extra lives than a cat ... a really bad cat.

Zero Hedge's adopted motto from The Fight Club is "On a long enough time line the survival rate of everyone drops to zero." Apparently, ZH thought Feddie's time line had been long enough. Today Zero Hedge stepped in as coroner.

It's proclamation is a long article, so I'll distill the applicable parts of it below, but if you want to read the whole piece, with formulas for interest rates, etc., you can find it at "The Biggest Credit Impulse In History Leads To Some Very Awkward Questions."

Back in June of last year, I only had the courage to ask "Is the Fed Dead?" It seemed likely to me that Feddie was nearly dead. So, I kicked him a few times and raised the question. This year, when the Fed's heartbeat (the stock market) didn't start ticking, even after injected with massive QEpinephrine, it seemed clear the Fed had finally met the end I said it would.

Now with ZH's affirmation, we can say the wicked Fed is not only "merely dead but really most sincerely dead."

Ding, dong the Fed is dead

First, the coroner took the Fed's pulse:

Regular readers know that it has long been our contention that - under the current regime of debt-fueled growth - one of the clearest indicators of future economic growth is the present credit impulse.

Zero Hedge

And then the coroner noted the amount of epinephrine the Fed had self-administered (something only a freak like Feddie Krueger can do):

In just the past 3 months we have seen a gargantuan $18+ trillion in fiscal and monetary stimulus, equivalent to just over 20% of global GDP? ZIt should hardly come as a surprise that as a result of this unprecedented firehose of credit-enabling liquidity, the recent spike in the credit impulse has been the greatest in history.

And then noted the lack of response:

Yet for the first time, GDP is not keeping pace.

I've noted for some time that the stock market had built up a tolerance to FedMed to where no amount would save either the economy (as measured by GDP) or the stock market in the next (now present) recession, also known here as The Epocalypse.

This point of failure, I've said for years would certainly arrive because of the Law of Diminishing Returns wherein the problems you start building up by administering one particular remedy start to outweigh the benefits and bring down the very thing you are trying to save. If what you are doing to cure the patient does nothing to eliminate his underlying cause of ailment, you can only pump more and more medicine, trying to effect the cure, until toxicity from the medicine, itself, takes the patient down.

So, when one of the many kinds of cancer taking this patient down was too much bad debt, you cannot cure the patient by getting him to take out a lot more debt in order to keep advancing to a higher cycle of debt-based economic growth. And that was only one thing the Fed was making worse, not better, by its cure. In essence, its approach to saving us from imploding bubbles was always to blow the bubble bigger.

Others have noted this phenomenon in the Fed's inability of late to get a response from FedMed:

As Deutsche Bank's Francis Yared writes in the latest Fixed Income Weekly report, "credit growth and lending surveys have historically been good indicators of underlying GDP growth." However, "the sharp divergence between credit and activity observed in the US, the eurozone and China is particularly unusual and highlights how different this crisis is relative to the GFC."

To be more prices in how I pronounced this death, I should have said all along that FedMed is dead. The Federal Reserve, of course, still exists and still carries out monetary operations. What is dead is the effectiveness of any of its remedies to bring recovery to the collapsing economy or a crashing stock market.

The surge we got in stocks this last time came well after the Fed started raising its injections of stimulus. It's too early really to know if the economy will respond because the economic delay is usually six months or more, but the stock market usually responds immediately.

This time the market did not respond until it was able to come to a belief that full recovery would be as quick as economic collapse had been.

ZH concludes there are two alternative ways of understanding the stock market's delayed response and GDP's total non-response:

i) either the credit impulse will have a massive impact on global growth, although somewhat delayed until the credit ends up in the broader economy unless of course it remains stuck in the stock market which has already wiped out most of its covid-losses [what I just said above about a delay for economic response], or ii) we are well and truly in a "newer abnormal", one where even drowning the world in cheap debt fails to boost GDP.

It would be too early to conclude the latter due to the normal lag, except ZH gives a strong indicator that nothing is happening even beneath the surface that can eventually stir life on the surface.

The economic establishment has bet its credibility on the first alternative [the normal delayed response].

And, thus, the stock market is going up because it believes the recovery will come and come quickly.

ZH argues for the latter alternative:

Recall that just one month ago we pointed out that the ... marginal utility of debt has collapsed to all time lows, as it takes ever more debt to result in economic growth, which is just another way of saying that the positive economic impact from any outsized credit impulse is virtually nil.

That would be the Law of Diminishing Returns, which I've long said will bring the death of FedMed (which I have more broadly called the death of the Fed (as in so far as both the stock market and the general economy are concerned).

And tied to that, is another reason why any day now the current system may be the last: the marginal utility of every new QE is now declining to the point where soon virtually none of the money created by the Fed out of thin air will enter the economy and instead will be stuck in capital markets, resulting in hyperinflation for asset prices even as the broader economy collapses.

I've described that as possible bizarre Wonderland where the stock market would continue to rise for months even as the economy continued to fall sharply, which would ultimately create a situation where bankrupt companies trade like trillion-dollar chips in the Wall Street Casino.

Because of the V-shaped recovery fantasy, the market didn't take long to do exactly that. I was able to report just in the last couple of weeks that the train wreck was already arriving at that station:

In this whirling dervish of a casino, you can buy bankrupt Hertz and see nearly ten times your money over the weekend! The stock is up 1,450% since the company declared bankruptcy. The Fed supplies the money needed to keep the casino open, while the reopening supplies the fantasy fiction needed to keep the bets coming.

In that article I quoted David Rosenberg making the conclusion I had said was coming if stocks kept going up while the economy collapsed:

It’s the mother of all “money illusion†rallies. In 3 months, the Fed juiced up M2 by a cool $2.5T, and the S&P 500 mkt cap surged dollar for dollar. Who needs earnings? Who needs productivity? Who even needs buybacks anymore? MMT arrived early and with a Republican in office!!

That is what ZH meant by "resulting in hyperinflation for asset prices even as the broader economy collapses." They go on to explain ...

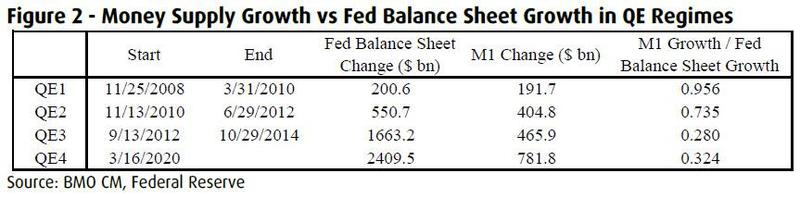

Or, as BMO's Daniel Krieter writes, "QE has fed through to the real economy in a slower manner than previous QE campaigns" and for each dollar the Fed's balance sheet has grown, M1 money supply has increased about $0.32, compared to $0.96 and $0.74 in QE1 and QE2. "The expansionary policy thus far has mostly resulted in increased asset prices", BMO writes concluding what had been obvious to us and our readers since 2009. Only now we are ten years closer to what is the inevitable endgame, one where the Fed has no impact on M1, which will also be known as the "game over" phase.

Game over

Some will say we are not, yet, at game over because the market is still rising, but my statement in my own article that I just quoted from was that the market is no longer rising because of the Fed, even though continued Fed support is essential for it to rise. It is rising based on the delusion of a V-shaped recovery, and there will prove to be nothing the Fed can do to save the market when that narrative fails.

In other words, the market remains entirely dependent on the Fed's support, but that support by itself, even in such historically great quantities as were are now seeing, is no longer sufficient to lift the market on its own. The market now needs a particular delusion to prove true. When the illusion of the delusion breaks, the market will fall.

Two things I said would be able to cause that failure: It will come in a little over one-and-a-half months when the V-shaped recovery hope fizzles out of sight like a mirage that gives way when reality makes itself more forcefully known (like when you start drinking the sand), or it will give way before then because the news starts bringing stories of a resurgence of COVID-19. After all, the recovery from economic collapse cannot happen if the disease that everyone believes brought the collapse shows it isn't going to take a recess in summer and isn't going to remain knocked down as the economy reopens from its globally enforced quarantine shutdown.

I cast a bet based on my total certitude in that premise as to why the market was rising, saying that the market would rise until reality started tearing down the delusion in late July, then it would fall with nothing the Fed could do to stop it. My one stated caveat for that bet, however, didn't give me time to hold on to the end of that ride. It popped up almost immediately (and certainly more quickly than I though it would): COVID-19 made a rapid resurgence, at least, in the headlines.

I figured we wouldn't see any resurgence for, at minimum, the fourteen-day incubation period that, according to WHO's and the CDC's and the government's statements, we were supposed to be able to expect after reopening. I figured, either they were right, so it would have no reason to blow back up before then, or they're part of a conspiracy in some sort of ginned-up viral event, in which case they would MAKE SURE no news popped up before then in order to prove they know what they're talking about.

My game ended quickly because news came out right at the fourteen-day point, but the news was about the week before, making the re-emergence actually before the incubation period. So, I had to cancel my floolhardy bet quickly based on the caveat I had given. (Never bet on a virus to keep its head down like the experts say it is supposed to do.)

As a result of the rapid re-emergency, we see the market already faltering, even as Fed stimulus continues at a rate of 1.5x QE3 and as Trump talks up another trillion in Fed-funded government giveaways.

One thing the resurgence, small it has been so far, did show was how sensitive the market is to any threat toward its "V" narrative. Instantly, the market plunged a whopping 1800 points. It hasn't recovered from that since, so that proves the "V" narrative is as essential as I said it was to the market's continued rise. Now it looks like the market is treading water to see if the viral news is going to continue to worsen and wipe away hope in the "V" or if the news was just a small bump and not the start of something worse.

But let's back up.

Traditionally, as BMO explains, we analyze the business cycle from a classical economic perspective where monetary authorities are more passive and “the invisible hand†guides economies (this used to be the case before the Fed went all Politburo on the USSA and decided to nationalize capital markets, crushing any "signal" the bond market may have; the final step will be the launch of Yield Curve Control which will be game over for the market).

That will be my theme for my next Patron Post, where I will continue to write about where the Fed goes next, which I've said (rightly so far) will not be negative interest rates. It's going to be a new form of "not QE" that is far more dangerous because it really QE without limits. It's "whatever it takes" QE; whereas all previous QE was in predetermined doses -- whether one-time megashots or in long-term repeating smaller doses. This will be a whole new kind of monster called "Yield Curve Control."

Why the plate spinner is losing control

Unfortunately, since 1913, theory has not worked due to the intervention of the Fed. So now let’s look at how all this works in reality, and introduce an active central bank with a wider range of monetary policy tools at its disposal.

By which ZH means the kind of central bank we have today with all of its new-fangled torture tools that it now uses to manipulate the economy and the stock market upward to meet its demand, creating zombie corporations all along its path.

The Fed embarks on asset purchases during QE and is successful in spurring consumption, as evidenced by the strong correlation between increases in excess reserves and increases in M1. M1 is the most basic measure of money supply and includes essentially only cash and checking/demand bank accounts.

The theory is that for a good or service to be consumed, it must be paid for out of M1. Therefore, the increase in M1 following QE is a measure of the degree to which QE results in actual consumption.

Based on that measure of how money supply should increase under massive doses of QE -- and always has until now -- ZH claims the rise in GDP is dead -- isn't going to happen because the monetary expansion from QE is not happening. It is merely backfilling all the damage.

The combination of QE-driven consumption ... and fading uncertainty after a trillion dollar fiscal stimulus package ... ultimately pulls the economy out of recession. However, the pace of response in 08/09 was slower. QE was not announced until late November 2008, after large defaults were already experienced. Fiscal stimulus ... didn’t arrive until February 2009 with an additional lag in implementation that featured incremental defaults. In the end, almost a trillion dollars’ worth of debt was affected by default in 2008/09, but QE certainly prevented actual defaults from being likely exponentially greater. BMO notes however that defaults avoided were once again economic resources that were not returned to the economy and barriers to entry that are not lowered. This argues that attractive investment opportunities following the financial crisis were not as abundant as the depth of recession would suggest.

As a result, the recovery was slow, ultimately prompting the Fed to embark on additional rounds of quantitative easing in an attempt to spur increased consumption.

In other words, the Fed's plan was very slow to work when its QE first entered the public lexicon during the Great Recession. That's because one thing a crash does is create a lot of cheap assets that others grab up at firesafe prices and build on or a rapid expansion. Before the Great Recovery period ended, QE was barely working at all:

Which brings us to the seeds of the Fed's own demise: the problem is that QE appears to be experiencing diminishing returns, as evidenced by a falling correlation between excess reserves and M1 in successive episodes of QE following the financial crisis. As QE leads to a direct increase in bank reserves, only a fraction is translated into money supply growth, and thus potentially consumption and investment. QE1 was highly effective and an important factor behind pulling the economy out of recession. QE2 had a marginally lower, but still high, follow through of ... $0.74 of each dollar of QE translated to increased money supply. We observe elevated inflation and personal consumption rates during the period of QE2 as evidence of its effectiveness. However, during Q3, the correlation fell to just $0.28 and resulted in very little inflation of GDP growth. Through this lens, the impact of QE on the real economy has diminished over time.

So, the coroner now announces that the Fed is dead on the basis that QE isn't doing anything to the underlying life signs that would normally cause GDP to rise after a reasonable lag time.

By "elevated inflation," ZH clearly doesn't mean a lot of inflation. I'm guessing they are noting that it was finally enough to make the needle wiggle.

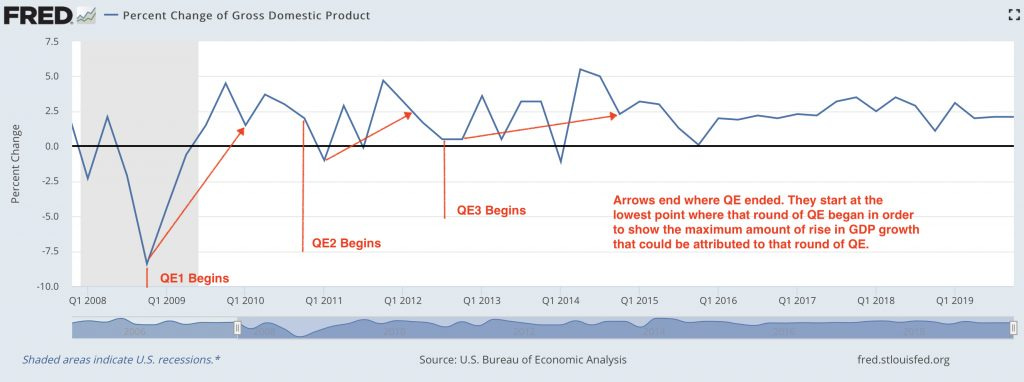

Notice the huge increase in the amount of QE needed ("Balance Sheet Change") each time to get a rise in money growth and to wiggle the needle and in GDP growth (not shown in this table, but shown in the graph to follow):

The following graph shows how each round of QE played out in terms of the subsequent GDP growth rate (with the arrow plotted to show the maximum amount of improvement in the GDP growth rate that could possibly be attributed to that round of QE based on the lowest GDP growth rate near the point where each round ended (near due to the expected lag time for the money to flow through to consumers and then show back up in business statistics that go into the GDP report):

At best, you can see that each round got less bang for the buck in terms of getting GDP growth to pick up. Yet, each amount of QE, as shown in the table, was much larger than the previous round in terms of how much money the Fed created. Once QE ended, we essentially flatlined if you average everything out at about 2.1% growth, even after the huge Trump Tax Cuts, which were promised to have their own effect at stimulating GDP growth.

ZH explains why this happens:

Diminishing marginal utility of consumption: QE (and monetary policy) is often referred to as "borrowing from the future". However, there is only a limited amount of future consumption that can be pulled into the current period via monetary policy. This could apply to consumption of durable goods: as rates have been relatively low for a long period of time, demand for credit no longer increases at the same rate with incrementally lower interest rates. At some point, consumption does not bring sufficient to utility no matter how long [low?] prices or interest rates are.

In other words, if you try to build your economy on increasing rounds of debt to bring consumption forward, eventually you reach the maximum amount of debt people can make use of, even with sloppier credit terms and rock-bottom interest. They simply don't want any more of your credit because they cannot afford to bring any more of their future income forward because the payment on all the debt they've already accumulated is eating them alive even at the lower interest rates.

What extremes will a dead Fed use to return on "The Night of the Living Fed?"

Once peak debt happens, the only way to get more stimulus out of credit in a consumer-based economy is to start giving the money away by letting the government take on all the debt as we are already doing, which is called MMT (Modern Monetary Theory).

So far, that isn't working, but enthusiasts will say it's just because this recession is so severe that three trillion dollars over three months is not enough of a kick. Well, true enough in one sense. We went there and did that, and consumption is still not back to what it was, but it could hardly be expected to be. So, the enthusiasts will just say, "Give it more time" and, I'm sure, "Give it more money." Time and money.

For right now, a trillion dollars a month hasn't done the job. And, if I'm right about the knock-on effects of the recent economic damage, it never will be enough because the worst damage is yet to come. So, this has to be QE4ever.

ZH also explains what should be obvious to everyone in the Fed as another reason the Fed's program works so poorly:

Wealth disparity: Wealth disparity exacerbates the impact of diminishing marginal utility of consumption.... QE tends to inflate the price of financial assets, making those who own the assets more wealthy. A large percentage of QE money ends up in the hands of the wealthy, whose consumption patterns are unlikely to change in response to a near term increase in wealth.

Obviously, when your plan is always to give more money to rich bankers who invest it in bonds and stocks to make rich corporate owners and richer bankers, then it doesn't do much to boost consumption because that tiny 1% of the population isn't going to change their consumption much because they have more money.

They're more about building up the amount of wealth they have. You can only use so many toys and so many bigger boats. So, the money created causes little inflation outside of financial assets, except in very high-end possessions like mansions and works of art and football teams that are purchased exclusively by the rich, somewhat for asset value and somewhat for enjoyment.

Thus, ZH gives this third reason for why each round of QE has accomplished less:

Wealth disparity: Wealth disparity exacerbates the impact of diminishing marginal utility of consumption. For reasons discussed in further detail below, QE tends to inflate the price of financial assets, making those who own the assets more wealthy. A large percentage of QE money ends up in the hands of the wealthy, whose consumption patterns are unlikely to change in response to a near term increase in wealth.

Now we are at a point where QE has brought some return of consumption maybe. Consumption is up from where it first plummeted, but it's hard to say any of that is due to QE, given the normal lag between Fed actions and economic recovery and particularly given that the government is simultaneously pumping trillions of economic stimulus into the economy and given that the economy was legally shutdown and now has been legally reopened.

I think we are seeing no results from the QE. ZH allows that there are slight results so far, but I attribute those to the factors just mentioned, as reopening is bound to have a huge impact and did, but it hasn't had enough to get us back to where we were.

Money supply that doesn't translate into consumption must result in higher financial asset prices until defaults result in wealth destruction. What does this mean for the recovery? The central bank is displaying reduced capacity to further generate real economic activity as a result of accommodative policy over the past twenty years.

According to ZH, the best thing we could hope for is a massive number of defaults that rips the bandage of the Fed's failed recovery, for if FedMed has died in terms of its effectiveness, what really dies is the Fed's faked-up economic recovery since 2008. The best outcome, in other words, would be what I was writing clear back then -- that everything that needed to default then and ever since should be allowed to default so that the rotting humus from all that dead material could be plowed back into the ground to make it fertile for new businesses.

Put another way, let the corrupt organizations die of their own corruption so they don't use the oxygen and food of those that didn't participate in their same level of greed. Let those who invested in them take 100% of the fall before anyone else does so that people start being a lot more careful about investing in corrupt, greedy banks and so that the banks that survive do so on warning that they can die, too, if they don't act more conservatively and responsibly than those that crashed. Let corporations that had too much debt that they could not maintain die to make room for new corporations and to avoid creating zombies that live past their time.

In other words, let Capitalism actually exist and function, instead of trying to protect capitalISTS by socializing all their losses!

The Fed's recovery program has reached its terminus. But that doesn't mean Feddie Krueger won't do desperate things if we all let him to return for more mayhem with measures far beyond what the Fed has done so far if we are stupid enough, lazy enough, and cowardly enough to let the Fed live on.

Of course, the Fed has the full support of corporate America, which long ago twiddled away all their surplus cash in order to fatten themselves with stock buybacks and which are now getting bailed out on the promise that they won't engage in buybacks again for a little while if they get a bunch of cheap or free Fed/government money.

(Who can even tell any more where the money comes from now that the Fed creates it, but the government backs it in case of default, but the Fed, in turn, will back all government shortfalls that were created by the backing of defaults. What a ludicrous system of pretend finance!)

The moneyed interests will do all they can to make sure the Fed and government protect them, and the general public doesn't seem to understand what is happening or why well enough to even try to put a stop to it. They have no tolerance or bravery for the level of pain involved in true correction anyway. They would rather let future generations bear the cost while pretending it won't be that bad for them.

Everyone has the cover of saying this all due to a true black-swan event (a specific virus that no one could have seen coming) to justify why the Fed and government should continue with rocket-fueled bailouts.

The Fed and government will go beyond the outer limits, so long as they can think of something new to try. So, expect the wildest and craziest death throes ever exhibited. It promises to be a highly dramatic death scene like the battle of dinosaurs.

Remember: this isn't just happening in the US. It's happening all over the world on just as great a scale. This is the destruction of corrupt, badly crippled, poorly reconstructed, economic systems with deep design flaws disintegrating because of the asteroid impact of a tiny virus-sized particle that blew up the world.

So, maybe to say "the Fed is dead" is a little less than accurate. Rather, everything it has tried to accomplish through all of its QE is dying and the Fed's ability to resurrect any of that is finished; the effectiveness of QE (FedMed) is dead; and everything like that all around the world is dying in an extinction-level event that will stink to the upper reaches of the atmosphere and be filled with all kinds of moaning and death drama.

Feddie Krueger isn't going down until he takes the entire world with him.

In my next Patron Post, I'll be talking a little about death of the dollar and a lot about Yield Curve Control.