The Great Yield Curve Control Conundrum

In one of my recent Patron Posts, I stated there was virtually no chance the Federal Reserve would be lowering interest rates below the zero bound. In spite of the massive economic damage we've seen from the coronavirus shutdown, that has so far remained true. The Fed has continued to say they don't believe they will ever go to Negative Interest Rate Policy (NIRP).

I fact, the following from the Fed notes sounds like there is not even the slightest interest in lowering interest rates any further:

Officials [on the FOMC] were in agreement with a need to give markets more information about what would cause the central bank to keep rates close to zero or move them higher.

Their talk at their last meeting was only about when to increase rates again:

In their discussion about this year, a “number†of Fed officials wanted to tie any rate hike to a modest overshoot of the Fed’s 2% inflation target. A “couple†of others favored tieing it to the unemployment rate. A “few†suggested setting a specific date. A couple of other Fed officials warned that committing to very low interest rates for a long time would pose significant risks to financial stability.

The Fed's position, then, is that even low interest rates pose problems they don't want. No one on the Federal Open Market Committee was leaning toward expressed any interest in ever taking rates lower.

The Fed knows the distortions caused by NIRP are not worth whatever limited benefits there might be because other nations have shown the benefits to be nothing compared to the distortions. As I noted in these Patron Posts about central bank digital currencies, the Fed is sometimes willing to let other central banks blaze new trails and learn from their mistakes.

NIRP was a mistake.

At their June meeting, Fed officials kept the benchmark federal funds rate in a range of 0% to 0.25% and put out a projection showing officials expect the rate to remain steady until 2023.

So, NIRP remains off the table, as I said it would, but the statement that ZIRP will remain in place until 2023 shows how longterm the Fed, contrary to the stock market that it nurtures, believes this downturn will last. That should lead us to ask what its next program will be, if it's not going to be NIRP.

(I think it's a given that the Fed will believe more programs are needed, as the present extensive efforts, coupled with massive government stimulus, clearly are not able to get the Dow or S&P to rise back up to their previous heights, and we all know the Fed has become the market's bitch.)

Yield curve control soon to come

Where central banks have gotten big results in the past, in contrast to NIRP, is in quantitative easing through bond buying. So, on that, they are going to continue full steam ahead:

Officials also agreed to keep asset purchase, which have included Treasurys and agency mortgage-backed securities, at least at the current pace of $120 billion per month.

As I've noted in other posts, that is 1.5x the rate of QE3, which had been the largest of all QE rounds. QE4ever has already dwarfed QE3 in size and now adds the new promise that it will continue indefinitely at this unprecedented high rate:

At their meeting, “a number†of Fed officials judged that there was a substantial chance of additional “waves of outbreaks†of the coronavirus. Another source of risk was that fiscal help for households, businesses, and state and local governments might prove insufficient.

At the June meeting, the Fed staff downgraded their projection for the economy from their prior forecast in April based on how the pandemic was evolving. The staff said their pessimistic forecast of a second wave of coronavirus outbreak later this year and subsequent economic damage was just as plausible as the more benign baseline forecast.... Fed officials said the lockdown will be disinflationary. Fed officials noted that the central bank will have to keep monetary policy highly easy for some time to achieve their 2% inflation target.

Indefinite QE, too, creates distortions, such as inversion of the yield curve, which banks don't like because their original business model required borrowing low short-term and loaning higher longterm. Inverted rates along the yield curve don't allow that. (By definition curve inversion means the further you go out in duration, the lower the interest rate goes.)

Now that the Fed is hoarding bonds at higher rates than ever, it could easily see yield-curve inversion happen on a worse scale than it did from its last long bout of easing because it is a lot closer to inversion than it was when it started the now comparatively small QE3. The Fed has a way to control that, however, which works very nicely with its wish to monetize the federal debt. It's called "Yield Curve Control" (YCC) or "Yield Curve Targets" (YCT). (The Fed prefers the term "target" to "control," as it sounds more free market and less autocratic.)

The essence of YCC is that the central bank, instead of committing to buy, say, $120 billion in bonds per month commits to holding the yields of certain bonds (say the US10YR) to a certain level. It, then, buys as many of those bonds as necessary to maintain that cap, assuring the Federal government a long, low interest rate.

In other words, the Fed sucks up every bond that starts to price above that level to make sure none do and, in essence, monetizes the US debt at a set rate for as long as the Fed continues that program or as long as it continues rolling that same debt over at that set rate.

The Fed did that during WWII to make it affordable for the US government to issue as much debt as necessary to fund the war.

The side effect the Fed probably doesn't want is that it also means the government becomes free to issue as much debt as it wants at that interest level. This effectively hands monetary policy and control of the size of the Fed's balance sheet over to the US treasury, as it becomes the treasury that determines how much new money will be created in the Federal

Reserve System by how much debt it issues with no concern for market constraints, such as pesky interest spikes.

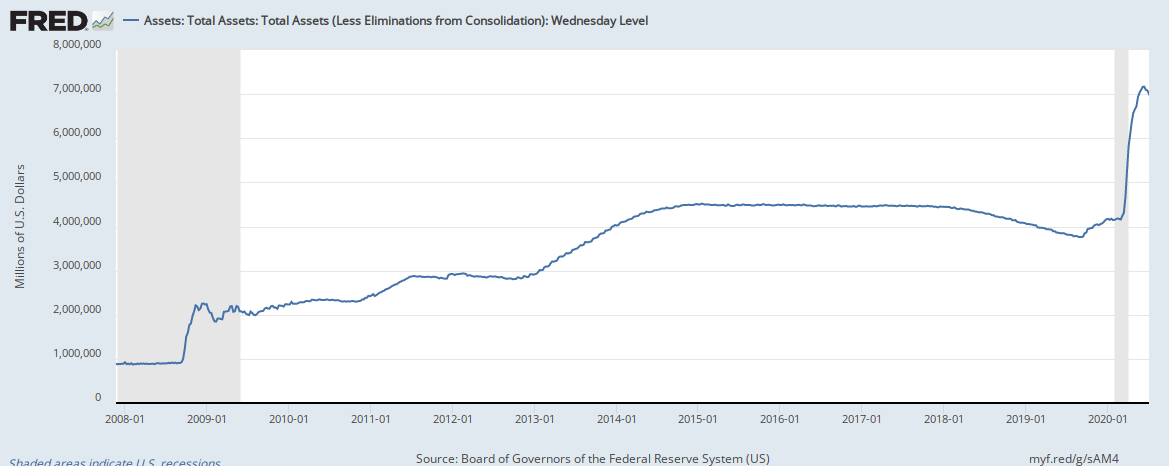

The Fed's balance sheet expansion already looks like a rocket ride into orbit compared to any other year:

{kind=link}

In three months, the Federal Reserve’s balance sheet rose from $4 trillion to $7 trillion. The central bank announced Wednesday that the money tsunami will go on flooding the financial system. The stock market will float in torrential liquidity, indefinitely.

Having just become what Bill Blain called "the de facto guarantors of the corporate bond market,†the Fed will likely soon become the de facto creditor for government debt. To a large extent it already was, but under YCC, the government can issue all the debit it wants, knowing the Fed will suck all of it up at a set rate. The government will no longer have to worry at all about what other domestic or foreign demand there is for government debt or about how a certain bond issuance, if too big, might drive up its interest.

It's likely coming soon to a theater near you, as Michael Lebowitz and Jack Scott have noted on Real Investment Advice:

The next iteration of monetary policy may well be “yield curve†control?

In the 1950s, each dollar of debt drove nearly 70 cents of economic growth. It has fallen ever since. Recently, each dollar of debt bought less than 30 cents of growth. That number has deteriorated further in the last few months....

Each dollar of debt drives less growth than the prior dollar of debt, thus requiring even more debt....

As the ratio of debt to GDP increases, even more debt is needed tomorrow just to maintain current economic activity. For a Fed overly concerned about short-term economic activity, this dilemma creates a self-reinforcing problem. The situation is akin to a Ponzi scheme that needs constant feeding....

Surging debt levels means the Fed will have to become even more creative and active in managing interest rates.

I believe the key reason the Fed has recently reduced its balance sheet while continuing to buy $120 billion in government bonds and MBS is partly to let the Repo stuff play off but also partly because it needs to get its YCC plan in place before it ignites the next stage in its rocket trajectory to the moon. For the moment, we've leveled off in orbit.

The Fed didn't have a YCC plan ready on the shelf because it wasn't expecting the Coronacrisis. If it did, we'd probably already be using it.

How YCC works and its risks that must be managed

YCC, this pair argues, gives the Fed "a bigger shovel" for digging the debt hole faster. With QE 1-3, the Fed set a predetermined amount of QE. As I've always maintained, QE4 will have to be QE4ever, meaning constantly upgradable in amount and endlessly extendable in time, and that is exactly what YCC offers.

You see, if the Fed simply said it was going to buy X amount of treasuries to save the economy, and then it had to keep adding more and more, it would look like its treasury purchases are not working. But if the Fed changes its goals from the old play book and says it is targeting X amount of interest and using bond purchases to achieve its interest target, then, when it has to add more and more treasuries to do that, it looks like the program is working splendidly because the Fed can continue to report after each FOMC meeting, "Our treasury purchase program is working to hold interest effectively at our stated target goals."

Yay! Endless stories of success. Thus, to move into the realm of endlessly expanding QE (QE4ever) that it has wanted to avoid ...

The Fed is now considering an enhancement to the way it manages QE. The “upgrade†is called yield curve control (YCC). YCC essentially allows the Fed to do unlimited amounts of QE with no time restraints. Embedded in YCC is the specific goal of targeting particular interest rates across the entire yield curve.

For example, assume the Fed set a 0.75% target yield on the 10-year U.S. Treasury note. They can then employ QE in any amount needed to buy 10-year notes when the rate exceeds that level. If successful, the rate would never exceed 0.75% as [bond] traders would learn not to fight the Fed....

YCC is a euphemism for price controls.... In this instance, we are talking about the most fundamental component of any economic system, the price of money. Historically, in every case, the implications of price controls have been unfortunate.

With YCC, the Fed controls the shape of the yield curve by "doing whatever it takes" to keep the curve in the shape the Fed wants so that banks can continue to borrow low in the short term and lend higher in the long term.

This is not a novel idea. The Fed did this to help the US fund WWII:

From 1942 to 1950, the Fed targeted rates to help manage funding costs for WWII. If you are interested in reading more on the U.S. experience with YCC, we suggest the following article from the Federal Reserve: How the Fed Managed the Treasury Yield Curve in the 1940s.

There is a downside, though, in that the Fed can become trapped in this mode, as it nearly did in the 40's. That creates an inflation problem, which can also eat up bank profits in a hurry:

It is worth pointing out that after WWII ended, inflation spiked to double digits, yet the Fed held interest rates at artificially low levels. While bondholders may not have lost money on the bonds per se, they did lose dearly in their purchasing power

The Fed becomes trapped because the government takes on so much debt that the government must have this continued low interest to survive its debt, and that means the Fed is stuck stimulating the economy full on, even if the economy starts to recover, which can lead to high inflation, putting the dollar at risk.

Those known risks are why the Fed has paused to seriously think this through before taking the step in order to see if it can be implemented in some way that will avoid the past pitfalls:

Federal Reserve Bank of New York President John Williams says that policymakers are “thinking very hard†about targeting specific yields on Treasury securities.

With YCC, the only limit the Fed sets for its bond buying is "whatever it takes" to keep giving the federal government the interest rate it needs to fund its debt. In a time when the debt is mushrooming, that means an ever-greater amount of bond purchases, not just to soak up the government debt, but to make sure that the debt others are also buying from the government stays within what the government can afford.

The bigger the debt, the less the government can afford it; so, as the program goes on, bond buying has to increase to push the interest down further. Reflecting on the history of YCC, the Fed has noted,

Fixing the level of Treasury yields endogenized the size of the System Open Market Account: the Fed had to buy whatever private investors did not want to hold at the fixed rates.

Playing on the yield curve like that proved to be a slippery slope:

Investors quickly came to appreciate that they faced a positively sloped yield curve in a market where yields were at or near their ceiling levels. An investor could move out the curve to pick up coupon income without taking on more risk and then ride the position down the curve, adding to total return. This strategy of “playing the pattern of rates†led investors to prefer bonds to bills. Their preferences, coupled with the Treasury’s decision to issue in all maturity sectors, forced the Open Market Account to buy unwanted bills and to sell the more attractive bonds. By late 1945 the Account held 75 percent of outstanding bills, but—in spite of heavy bond issuance by the Treasury—fewer bonds than it had held in late 1941.

Getting itself out of the mess it created by manipulating interest rates ultimately became a difficult juggling act for the Fed and may have helped plunge the nation into a post-war recession because of the inflation that ensued. Maybe the recession would have happened anyway as just a post-war employment phenomenon. Who can know?

Perhaps because it fears this slippery slope, the FOMC apparently is not ready to implement YCC yet:

Officials said more work was needed on another possible tool — yield curve control — that could put a cap on longer-term rates.

"The minutes from the early-June FOMC meeting suggest that the Fed is still a long way from rolling out explicit targets for longer-term Treasury yields,†wrote Andrew Hunter, senior U.S. economist at Capital Economics.

Yet, their minutes show they definitely are strategizing about that:

The second staff briefing reviewed the yield caps or targets (YCT) policies that the Federal Reserve followed during and after World War II and that the Bank of Japan and the Reserve Bank of Australia are currently employing. These three experiences illustrated different types of YCT policies:... The staff noted that these three experiences suggested that credible YCT policies can control government bond yields, pass through to private rates, and, in the absence of exit considerations, may not require large central bank purchases of government debt. But the staff also highlighted the potential for YCT policies to require the central bank to purchase very sizable amounts of government debt under certain circumstances—a potential that was realized in the U.S. experience in the 1940s—and the possibility that, under YCT policies, monetary policy goals might come in conflict with public debt management goals, which could pose risks to the independence of the central bank.

The problem is there are always exit considerations. We know the Fed is horrible at exist strategies. When the Fed tried to extract itself from these operations after the war, it got a lot of pressure from the government to continue so that the government could fund its next war with North Korea. It took a literal act of congress to create an exit for the Fed.

We also saw how poorly the Fed's exit from its previous three rounds of QE went -- abject failure. Just as I always said, the Fed had not exit plan that would work. It's now stuck in QE. So, it's trying to think through its exit strategy this time.

In spite of the Fed's exit concerns, it may soon find itself needing to commit to very longterm purchases of "very sizable amounts of government debt" because of the present circumstances where the government is giving away money left and right.

YCC also proved hugely beneficial to stocks when it was last tried because it potentially commits the Fed to massive and ever-growing bond purchases (QE4ever), giving the stock market a long program of money creation to support its bets. And we know that is enticement for the Fed since the termination of Glass-Steagall allowed bankers to play much more freely in the stock market.

Bloomberg notes how nicely this would work for stocks:

As central banks pump trillions into the world economy, investors are setting their sights on what could be the next big thing in global monetary policy: yield curve control....

They are hoping for it, begging for it, possibly waiting on hold for it to be announced.

Should yield curve control go global, it would cement markets’ perception of central banks as the buyers of last resort, boosting risk appetite, lowering volatility and intensifying a broader hunt for yield. While money managers caution that such an environment could fuel reckless investment [really? like they care!] already stoked by a flood of fiscal and monetary stimulus, they nonetheless see benefits rippling across credit, equities, gold and emerging markets....

"Broadly speaking it’s the green light to carry on with the QE trade -- buy everything regardless of valuation,†said James Athey, who manages $3.1 billion at Aberdeen Standard Investments in London.

This is what the Fed must do if it wants to come back to life (for one last hurrah). It must pull out all the stops with YCC, a.k.a. self-avowed QE without limits (QE4ever).

From the Fed's point of view, what's not to like about ramping up into an every-increasing spiral of debt creation with the greatest bond purchases in history at set interest rates for eternity? It's actually their only hope. That's where they are now -- blow the thing wide open in the greatest nuclear central-bank explosion or die for good. It's Feddie Krueger's last chance at a final death scene.

While it could really help out the zombie trade, there is no guarantee, of course, that it will have the desired effect on stocks. The zombie trade has become so absurd already, and it is something that didn't even exist in the forties. It may just blow up in a matter of months under such acceleration. If the Fed is evaluating YCC based on its unwanted problems in the 40s, it has no way of gauging the zombie factor.

This might be like putting a 5,000 horsepower engine in a rusted-out VW bug and then trying to drive it down the street, pedal to the metal. All you do is twist the driveshaft into pretzels and send the transmission into orbit while the bug barely lurches ahead.

To put that in market terms, it would likely result rapidly in that bizarre situation where companies that are profitless due to the falling economy trade as trillion-dollar chips in the Wall Street casino.

With such delightful incentives, there was one thing on which the FOMC was unanimous:

All participants agreed that it would be useful for the staff to conduct further analysis of the design and implementation of YCT policies as well as of their likely economic and financial effects.

The option is solidly on the table for further study and possible implementation down the road. In fact, it sounds like the only thing holding the Fed back is designing a program they believe they can get out of more easily than they did back in the forties.

The committee also noted that demand for Fed repurchase agreements (repos) peaked in March and have subsequently subsided, so long as the Fed maintains its monthly QE "of approximately $80 billion in Treasury securities and $40 billion in agency MBS."

That's proof the Repocalpse that began last fall and the Fed's repo operations to quell the storm were always something that had to be resolved by a return to full-on QE at an ongoing level even greater than QE3. (Hence, again, requiring QE4ever, so everything points in that direction on an expanding scale.)

The Fed likes to think it can find an exit, as it tried to in 2017 and 2018, but it can't. It's earlier attempted exit created the Repo Crisis. Getting back to QE ended it ... so long as QE continues ... forever. Now, it's looking for a way to carry out QE4ever, which is YCC, and still dreaming it can have an exit strategy that doesn't end as the worst crash in history.

The negative side effects Bloomberg noted as likely to come from YCC were deterioration of the dollar while boosting riskier emerging-market currencies, including the Russian ruble, and hyperinflation of the asset bubble risks. (My trillion-dollar chip scenario for shell corporations, which would obviously be an extremely unstable situation.)

The dead Fed can only resurrect itself via destruction of the dollar

The Fed is now trapped in a Gordian knot, whether it realizes it or not. If it tries to save itself, it will likely kill the dollar. If the dollar dies, that's the Fed's only reason for existence, so the Fed dies anyway.

If the Fed takes the YCC step, it may be locking in destruction of its own dollar; yet, the step ultimately appears locked in, whether the Fed wants to admit it or not. This is the corner it has painted itself into:

Regardless, the notion that central banks are approaching some sort of curve control is here to stay. A key lesson from the 2008 crisis was that policy makers need to intervene quickly, and investors now expect them to consider any weapon at their disposal....

“The markets became too big to fail,†said Mark Nash, the head of fixed income at Merian Global Investors in London. “Now they have no choice but to keep them working.â€

I'm sure all it will take for the Fed to overcome its exit-strategy concerns is for the market to careen over the next cliff. The Fed knows, if this happens, its next step must be massive.

At its last meeting, the Fed admitted it is losing power; or, as I've been putting it, the Fed is dead. If not absolutely, positively dead, then, at least, Freddie Krueger dead. But let's put it in the Fed's words:

“Several participants remarked that declines in the neutral rate of interest and in term premiums over the past decade and prevailing low levels of longer-term yields would likely act as constraints on the effectiveness of asset purchases in the current environment and noted that these constraints were not as acute when the Committee implemented such programs in the wake of the Global Financial Crisis.â€

Or, expressed in my terms, FOMC members realize the Fed is seeing much less bang for much bigger bucks, and its members are recognizing that is going to be a problem for QE effectiveness going forward.

They also said,

businesses and households might not be as forward looking as assumed in the model simulations, which could reduce the effectiveness of policies that are predicated on influencing expectations about policy several years into the future.

In other words, they are concerned that "forward guidance" is also getting a lot less responsivenesss. The Fed's mere words used to move mountains. Now businesses and households are less apt to care what the Fed says as it begins to look increasingly ineffective in an increasingly desperate situation.

The Fed even admitted that the current boost in the stock market had less to do with Fed operations than with belief in a V-shaped economic recovery as the US economy reopened for business:

Risk asset prices were buoyed by optimism about the potential for increased economic activity associated with reopenings as parts of the United States and other countries relaxed lockdown restrictions. That optimism was reinforced by high-frequency data suggesting a pickup in economic activity. Market participants also pointed to the suite of U.S. and global policy measures taken since mid-March as laying a foundation for the improvement in risk sentiment. Against this backdrop, staff analysis suggested that equity prices had been supported by expectations for a strong rebound in earnings next year, low risk-free rates and positive risk sentiment.

This does not mean the market's rise has nothing to do with Fed QE. QE is still totally essential as a "foundation" to sustain the market's rise. What the Fed is saying now (and what I have been saying in recent articles) is that FED QE is no longer SUFFICIENT to create a rise in the stock market.

That rise requires unwavering belief in a V-shaped recovery coming out of the Coronacrisis and on huge amounts of federal government stimulus. It takes all three of things to float the market now -- Fed QE, belief in the "V" and huge government stimulus.

The "V" isn't going to happen for the Fed, and the Fed knows that, even though the market does not. Powell even risked stating as much at his last presser.

In essence, we have seen the greatest central-bank quantitative easing in history all over the world (but especially at the Fed), an immediate return to zero interest rates, the greatest government stimulus and bailout packages in history during a time of extreme tax breaks, and most of the stock market still remains below the peak from which it crashed going into this recession.

Pull the plug on the "V" narrative, and the market will fall even with massive Fed QE. Pull the plug on all government stimulus, as could happen in the second half of summer, and the market will crash.

The days when the Fed could do it alone are gone! It cannot even get the market back to the heights it once achieved with all this government help. With YCC funding the governments stimulus through limitless QE, maybe it can get enough of a final team push to do a little more. Maybe.

The next question to ask is how long does the Fed anticipate continuing exponential QE since it doesn't want to admit it must be forever?

Simulations suggested that the Committee would have to maintain highly accommodative financial conditions for many years to quicken meaningfully the recovery from the current severe downturn.

While they haven't admitted to themselves the likelihood that these "highly accommodative financial" interventions will have to continue forever, they have admitted they will have to continue for a very long time in order to be meaningful -- many years, not just a few.

Thus, YCC is likely assured, and with it destruction of the dollar finally comes onto the radar screen as a real possibility. This is a possibility that didn't even exist during World War II when the Fed last engaged in YCC because the dollar had not yet become the global trade currency, a status the US government has come to depend on.

"Death of the dollar" doesn't mean end of the dollar

I'm not saying the dollar will go out of existence, though that's highly possible. I'm talking about the possible sudden death of the dollar's special status as the global trade currency, including the petrodollar that anchors that status. That will do a lot to end US hegemony in the world, so it will alter the balance of global power if it happens.

If that happens, it also means the US will become utterly dependent on the Fed for its financing because all of that global trade dependence on dollars is what has assured for decades the US government could find cheap funding for all of its national debt.

It may be the reverse is equally true -- that, as the US becomes dependent on the Fed for financing of stimulus during the Coronacrisis, it assures death of the dollar as a global trade currency.

As I said, the situation was much different during WWII. Back then, the Fed didn't have to worry that unlimited bond-buying to achieve a set interest rate for the government would cause hyperinflation because the government set price controls to make sure that didn't happen; and price controls were easier to justify under the resource tightness and literal trade barriers created by the war.

So, unless we change over to communism where the government determines how much money is in the system and sets the prices, this program could be difficult to manage. The potential to have inflation in a deflationary environment (stagflation) comes into play here, too. That can happen when too much money chases too few resources during a time of decreased demand.

There are many factors hitting the dollar now, and many contenders wanting to be the next global currency.

Unlike those who write about the end of the dollar endlessly, as if it may happen in any year, I've never written about it. There was no year in which I've considered death of the dollar even remotely possible. However, it is finally a real enough possibility, so I am taking it up. "Death of the Dollar" will be the subject of my next Patron Post to come out in another day or two as the second part to this one.